import pdb

import time

import datetime

import traceback

from Dhan_Tradehull_V2 import Tradehull

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as pta

import pandas_ta as ta

import warnings

warnings.filterwarnings("ignore")

# ---------------for dhan login ----------------

client_code = "11047"

token_id = "eyJ0eXAiOiJK"

tsl = Tradehull(client_code,token_id)

traded = "no"

trade_info = {"options_name":None, "qty":None, "sl":None, "CE_PE":None}

reward_risk_ratio = 3

while True:

current_time = datetime.datetime.now()

index_chart = tsl.get_historical_data(tradingsymbol='NIFTY JAN FUT', exchange='NFO', timeframe="5")

time.sleep(5)

index_ltp = tsl.get_ltp_data(names = ['NIFTY JAN FUT'])['NIFTY JAN FUT']

# if (index_chart.empty):

# time.sleep(60)

# continue

# rsi ------------------------ apply indicators

index_chart['rsi'] = talib.RSI(index_chart['close'], timeperiod=14)

# vwap

index_chart.set_index(pd.DatetimeIndex(index_chart['timestamp']), inplace=True)

index_chart['vwap'] = pta.vwap(index_chart['high'] , index_chart['low'], index_chart['close'] , index_chart['volume'])

# Supertrend

indi = ta.supertrend(index_chart['high'], index_chart['low'], index_chart['close'], 10, 2)

index_chart = pd.concat([index_chart, indi], axis=1, join='inner')

# vwma

index_chart['pv'] = index_chart['close'] * index_chart['volume']

index_chart['vwma'] = index_chart['pv'].rolling(20).mean() / index_chart['volume'].rolling(20).mean()

# volume

volume = 50000

first_candle = index_chart.iloc[-3]

second_candle = index_chart.iloc[-2]

running_candle = index_chart.iloc[-1]

# ---------------------------- BUY ENTRY CONDITIONS ----------------------------

bc1 = first_candle['close'] > first_candle['vwap'] # First Candle close is above VWAP

bc2 = first_candle['close'] > first_candle['SUPERT_10_2.0'] # First Candle close is above Supertrend

bc3 = first_candle['close'] > first_candle['vwma'] # First Candle close is above VWMA

bc4 = first_candle['rsi'] < 80 # First candle RSI < 80

bc5 = second_candle['volume'] > 50000 # Second candle Volume should be greater than 50,000 for Nifty and above 125,000 for Bank Nifty

bc6 = traded == "no"

bc7 = index_ltp > first_candle['low']

print(f"BUY \t {current_time} \t {bc1} \t {bc2} \t {bc3} \t {bc4} \t {bc5} \t {bc6} \t {bc7} \t first_candle {str(first_candle['timestamp'].time())}")

# ---------------------------- SELL ENTRY CONDITIONS ----------------------------

sc1 = first_candle['close'] < first_candle['vwap'] # First Candle close is below VWAP

sc2 = first_candle['close'] < first_candle['SUPERT_10_2.0'] # First Candle close is below Supertrend

sc3 = first_candle['close'] < first_candle['vwma'] # First Candle close is below VWMA

sc4 = first_candle['rsi'] > 20 # First candle RSI < 80

sc5 = second_candle['volume'] > 50000 # Second candle Volume should be greater than 50,000 for Nifty and above 125,000 for Bank Nifty

sc6 = traded == "no"

sc7 = index_ltp < first_candle['high']

print(f"SELL \t {current_time} \t {sc1} \t {sc2} \t {sc3} \t {sc4} \t {sc5} \t {sc6} \t {sc7} \t first_candle {str(first_candle['timestamp'].time())} \n")

if bc1 and bc2 and bc3 and bc4 and bc5 and bc6 and bc7:

print("Buy Signal Formed")

ce_name, pe_name, ce_strike, pe_strike = tsl.OTM_Strike_Selection('NIFTY','23-1-2025',2)

ce_ltp = tsl.get_ltp_data(names = [ce_name])[ce_name]

lot_size = tsl.get_lot_size(ce_name)*1

entry_orderid = tsl.order_placement(ce_name,'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info['options_name'] = ce_name

trade_info['qty'] = lot_size

sl_percentage = 15 / 100 # 15%

target_percentage = 30 / 100 # 30%

trade_info['sl'] = ce_ltp * (1 - sl_percentage)

trade_info['target'] = ce_ltp * (1 + target_percentage)

trade_info['CE_PE'] = "CE"

if sc1 and sc2 and sc3 and sc4 and sc5 and sc6 and sc7:

print("Sell Signal Formed")

ce_name, pe_name, ce_strike, pe_strike = tsl.OTM_Strike_Selection('NIFTY','23-1-2025',2)

pe_ltp = tsl.get_ltp_data(names = [pe_name])[pe_name]

lot_size = tsl.get_lot_size(pe_name)*1

entry_orderid = tsl.order_placement(pe_name,'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info['options_name'] = pe_name

trade_info['qty'] = lot_size

sl_percentage = 15 / 100 # 15%

target_percentage = 30 / 100 # 30%

trade_info['sl'] = ce_ltp * (1 - sl_percentage)

trade_info['target'] = ce_ltp * (1 + target_percentage)

trade_info['CE_PE'] = "PE"

# ---------------------------- check for exit SL/TG

if traded == "yes":

long_position = trade_info['CE_PE'] == "CE"

short_position = trade_info['CE_PE'] == "PE"

if long_position:

options_ltp = tsl.get_ltp_data(names = [trade_info['options_name']])[trade_info['options_name']]

sl_hit = options_ltp < trade_info['sl']

trailing_tg_hit = index_ltp < running_candle['SUPERT_10_2.0'] # this is a trailing target, by supertrend

tg_hit = options_ltp > trade_info['target']

if sl_hit or trailing_tg_hit or tg_hit:

print("Order Exited", trade_info)

exit_orderid = tsl.order_placement(trade_info['options_name'],'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

pdb.set_trace()

if short_position:

options_ltp = tsl.get_ltp_data(names = [trade_info['options_name']])[trade_info['options_name']]

sl_hit = options_ltp > trade_info['sl']

trailing_tg_hit = index_ltp > running_candle['SUPERT_10_2.0'] # this is a trailing target, by supertrend

tg_hit = options_ltp < trade_info['target']

if sl_hit or trailing_tg_hit or tg_hit:

print("Order Exited", trade_info)

exit_orderid = tsl.order_placement(trade_info['options_name'],'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

pdb.set_trace()

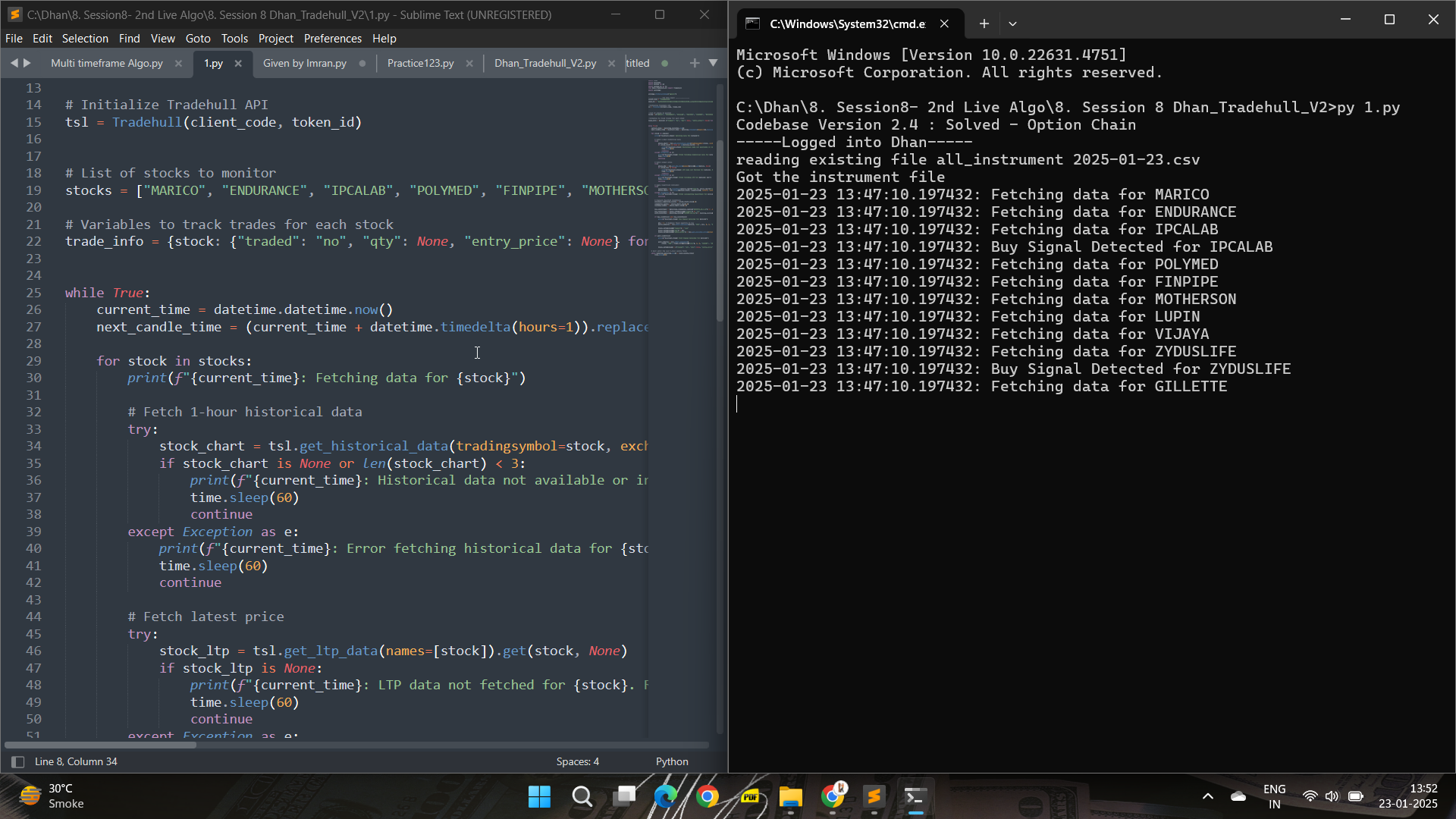

Sir, in this code it shows this error

" Exception at calling ltp as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: None, ‘error_type’: None, ‘error_message’: None}, ‘data’: {‘data’: {‘805’: ‘Too many requests. Further requests may result in the user being blocked.’}, ‘status’: ‘failed’}}

Traceback (most recent call last):

File “d:/Python/My Strategy/two candle theory.py”, line 134, in

options_ltp = tsl.get_ltp_data(names = [trade_info[‘options_name’]])[trade_info[‘options_name’]]

KeyError: ‘NIFTY 23 JAN 23200 CALL’

"

And then the code is stops, Please give me fix sir, why it is not tracking, Target and SL?

Thanks.