Hi @Tradehull_Imran ,

How to calculate Change in OI …?

Hi @Tradehull_Imran ,

How to calculate Change in OI …?

yes it is easy, share your code.

like if u want it should trail to ctc it can do that also if u want it trail continually like for every 5point it can trail sl up.

or can use this code and modify according to your needs

while True:

try:

current_market_price_dict = tsl.get_ltp_data(names=[trading_symbol])

current_market_price = current_market_price_dict[trading_symbol]

if current_market_price >= target_price:

# Target booking

tsl.modify_order(order_id=stoploss_orderid, order_type= "MARKET", quantity=qty, price=0, trigger_price=0)

log_queue.put(f"Target reached. Selling {trading_symbol} at market price. Sell Order ID: {stoploss_orderid}")

logging.info(f"Target reached. Selling {trading_symbol} at market price. Sell Order ID: {stoploss_orderid}")

break

elif current_market_price >= buy_price + sltrail:

# Calculate new stop-loss price

modified_sl = current_market_price - sltrail

sl_limit_price = modified_sl - 1

# Place a new stop-loss order

tsl.modify_order(order_id=stoploss_orderid, order_type= "STOPLIMIT", quantity=qty, price=sl_limit_price, trigger_price=modified_sl)

log_queue.put(f"New Stop Loss Order Placed. Order ID: {stoploss_orderid}, Stop Price: {modified_sl}")

logging.info(f"New Stop Loss Order Placed. Order ID: {stoploss_orderid}, Stop Price: {modified_sl}")

Hi @Vinod_Kumar1 ,

Send your code, will check if any speed optimization is possible in the code.

Hi @Abhishek_Pawde ,

do use this upgraded codebase file to get option chain for stocks:

Hi @Himansshu_Joshi

use below code

if ltp < sl_price:

modified_order = tsl.modify_order(order_id=sl_orderid,order_type="MARKET",quantity=25,price=0,trigger_price=0)

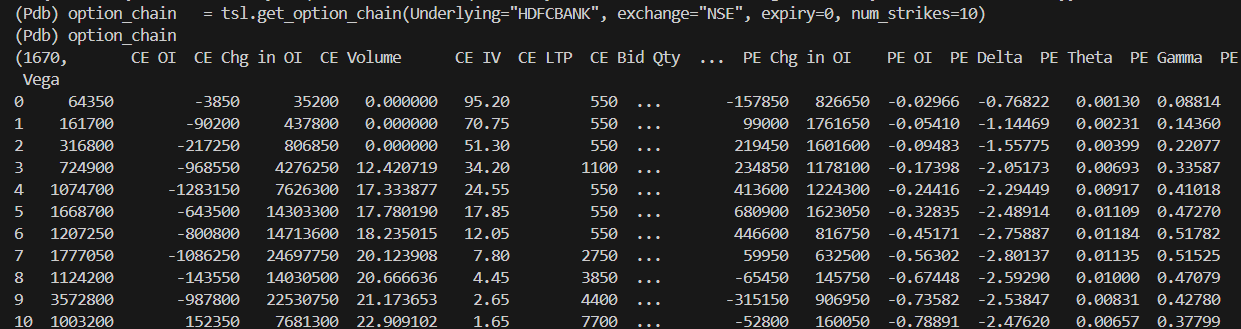

hi @Akshay_Bawane ,

you can fetch change in oi from the option chain directly. refer below code

option_chain = tsl.get_option_chain(Underlying="NIFTY", exchange="INDEX", expiry=0, num_strikes=10)

hello @Tradehull_Imran can i add indicator on ltp combined atm preimum live data while streaming i was trying but i failed mutlipe times

please suggest a code for trailing stop loss… or way to do it…

Do send the code and error faced as well

Hi @SF_F

we will be creating Trailing SL in detail in upcoming advance Algorithmic Trading Series.

for the Change in OI data from dhanhq… divide it by lot size.

Also for SENSEX the lot size will be 20 now.

thank you for your response in the meantime please confirm if below code works for trailing SL.

order_price = tsl.get_executed_price(orderid=buy_entry_orderid)

if order_status == "Traded":

print("Buy 1st order Successful, Order Price -", order_price)

if initial_SL == 0 #ensure always zero else initial SL will not trigger

#SL Cal.

sl_price = int(round((order_price-2),1))

sl_orderid = tsl.order_placement(atm_ce_sp,'NSE', 1, sl_price, sl_price, 'STOPMARKET', 'SELL', 'MIS')

sl_order_status = tsl.get_order_status(orderid=sl_orderid)

initial_SL = 1

print("Stoploss order pending-", sl_price)

continue

sl_order_status = tsl.get_order_status(orderid=sl_orderid)

sl_orderid_price = tsl.get_executed_price(orderid=sl_orderid)

if sl_order_status == "Pending":

#tlsl_status

tlsl_1Min = tsl.get_historical_data(tradingsymbol=atm_ce_sp,exchange='NSE',timeframe='1')

tlsl_ltp = int(tlsl_1Min['close'].iloc[-2])

usl_price = int(round(max(order_price,tlsl_ltp)-2,0))

if usl_ltp > sl_price:

cancel_details = tsl.cancel_orders(sl_orderid)

sl_orderid = tsl.order_placement(atm_ce_sp,'NSE', 1, usl_price, usl_price, 'STOPMARKET', 'SELL', 'MIS')

print("modify_TL_order-", tlsl_ltp, sl_orderid)

sl_order_status = tsl.get_order_status(orderid=sl_orderid)

if order_status == "Traded":

print("Modified_Stoploss Hit-", sl_price, sl_orderid)

sl_orderid_price = tsl.get_executed_price(orderid=sl_orderid)

order_detail = tsl.get_orderbook('')

Good afternnon sir, I was trying to Multitime frame file from Session 8, I am getting this error:

CODE:

import pdb

from Dhan_Tradehull_V2 import Tradehull

import pandas as pd

import talib

import time

import datetime

client_code = “1101092420”

token_id = “-----------”

tsl = Tradehull(client_code,token_id)

available_balance = tsl.get_balance()

leveraged_margin = available_balance5

max_trades = 1

per_trade_margin = (leveraged_margin/max_trades)

max_loss = (available_balance1)/100*-1

watchlist = [‘MOTHERSON’, ‘OFSS’, ‘MANAPPURAM’, ‘BSOFT’, ‘CHAMBLFERT’, ‘DIXON’, ‘NATIONALUM’, ‘DLF’, ‘IDEA’, ‘ADANIPORTS’, ‘SAIL’, ‘HINDCOPPER’, ‘INDIGO’, ‘RECLTD’, ‘PNB’, ‘HINDALCO’, ‘RBLBANK’, ‘GNFC’, ‘ALKEM’, ‘CONCOR’, ‘PFC’, ‘GODREJPROP’, ‘MARUTI’, ‘ADANIENT’, ‘ONGC’, ‘CANBK’, ‘OBEROIRLTY’, ‘BANDHANBNK’, ‘SBIN’, ‘HINDPETRO’, ‘CANFINHOME’, ‘TATAMOTORS’, ‘LALPATHLAB’, ‘MCX’, ‘TATACHEM’, ‘BHARTIARTL’, ‘INDIAMART’, ‘LUPIN’, ‘INDUSTOWER’, ‘VEDL’, ‘SHRIRAMFIN’, ‘POLYCAB’, ‘WIPRO’, ‘UBL’, ‘SRF’, ‘BHARATFORG’, ‘GRASIM’, ‘IEX’, ‘BATAINDIA’, ‘AARTIIND’, ‘TATASTEEL’, ‘UPL’, ‘HDFCBANK’, ‘LTF’, ‘TVSMOTOR’, ‘GMRINFRA’, ‘IOC’, ‘ABCAPITAL’, ‘ACC’, ‘IDFCFIRSTB’, ‘ABFRL’, ‘ZYDUSLIFE’, ‘GLENMARK’, ‘TATAPOWER’, ‘PEL’, ‘IDFC’, ‘LAURUSLABS’, ‘BANKBARODA’, ‘KOTAKBANK’, ‘CUB’, ‘GAIL’, ‘DABUR’, ‘TECHM’, ‘CHOLAFIN’, ‘BEL’, ‘SYNGENE’, ‘FEDERALBNK’, ‘NAVINFLUOR’, ‘AXISBANK’, ‘LT’, ‘ICICIGI’, ‘EXIDEIND’, ‘TATACOMM’, ‘RELIANCE’, ‘ICICIPRULI’, ‘IPCALAB’, ‘AUBANK’, ‘INDIACEM’, ‘GRANULES’, ‘HDFCAMC’, ‘COFORGE’, ‘LICHSGFIN’, ‘BAJAJFINSV’, ‘INFY’, ‘BRITANNIA’, ‘M&MFIN’, ‘BAJFINANCE’, ‘PIIND’, ‘DEEPAKNTR’, ‘SHREECEM’, ‘INDUSINDBK’, ‘DRREDDY’, ‘TCS’, ‘BPCL’, ‘PETRONET’, ‘NAUKRI’, ‘JSWSTEEL’, ‘MUTHOOTFIN’, ‘CUMMINSIND’, ‘CROMPTON’, ‘M&M’, ‘GODREJCP’, ‘IGL’, ‘BAJAJ-AUTO’, ‘HEROMOTOCO’, ‘AMBUJACEM’, ‘BIOCON’, ‘ULTRACEMCO’, ‘VOLTAS’, ‘BALRAMCHIN’, ‘SUNPHARMA’, ‘ASIANPAINT’, ‘COALINDIA’, ‘SUNTV’, ‘EICHERMOT’, ‘ESCORTS’, ‘HAL’, ‘ASTRAL’, ‘NMDC’, ‘ICICIBANK’, ‘TORNTPHARM’, ‘JUBLFOOD’, ‘METROPOLIS’, ‘RAMCOCEM’, ‘INDHOTEL’, ‘HINDUNILVR’, ‘TRENT’, ‘TITAN’, ‘JKCEMENT’, ‘ASHOKLEY’, ‘SBICARD’, ‘BERGEPAINT’, ‘JINDALSTEL’, ‘MFSL’, ‘BHEL’, ‘NESTLEIND’, ‘HDFCLIFE’, ‘COROMANDEL’, ‘DIVISLAB’, ‘ITC’, ‘TATACONSUM’, ‘APOLLOTYRE’, ‘AUROPHARMA’, ‘HCLTECH’, ‘LTTS’, ‘BALKRISIND’, ‘DALBHARAT’, ‘APOLLOHOSP’, ‘ABBOTINDIA’, ‘ATUL’, ‘UNITDSPR’, ‘PVRINOX’, ‘SIEMENS’, ‘SBILIFE’, ‘IRCTC’, ‘GUJGASLTD’, ‘BOSCHLTD’, ‘NTPC’, ‘POWERGRID’, ‘MARICO’, ‘HAVELLS’, ‘MPHASIS’, ‘COLPAL’, ‘CIPLA’, ‘MGL’, ‘ABB’, ‘PIDILITIND’, ‘MRF’, ‘LTIM’, ‘PAGEIND’, ‘PERSISTENT’]

traded_wathclist =

while True:

live_pnl = tsl.get_live_pnl()

current_time = datetime.datetime.now().time()

if current_time < datetime.time(9, 30):

print("wait for market to start", current_time)

continue

if (current_time > datetime.time(23, 15)) or (live_pnl < max_loss):

I_want_to_trade_no_more = tsl.kill_switch('ON')

order_details = tsl.cancel_all_orders()

print("Market is over, Bye Bye see you tomorrow", current_time)

break

for stock_name in watchlist:

time.sleep(0.2)

print(stock_name)

# Conditions that are on 1 minute timeframe

# chart_1 = tsl.get_intraday_data(stock_name, 'NSE', 1) # 1 minute chart # this call has been updated to get_historical_data call,

chart_1 = tsl.get_historical_data(tradingsymbol = stock_name,exchange = 'NSE',timeframe="1")

chart_1['rsi'] = talib.RSI(chart_1['close'], timeperiod=14) #pandas

cc_1 = chart_1.iloc[-2] #pandas completed candle of 1 min timeframe

uptrend = cc_1['rsi'] > 60

downtrend = cc_1['rsi'] < 40

# Conditions that are on 5 minute timeframe

# chart_5 = tsl.get_intraday_data(stock_name, 'NSE', 5) # 5 minute chart

chart_5 = tsl.get_historical_data(tradingsymbol = stock_name,exchange = 'NSE',timeframe="5") # this call has been updated to get_historical_data call,

chart_5['upperband'], chart_5['middleband'], chart_5['lowerband'] = talib.BBANDS(chart_5['close'], timeperiod=5, nbdevup=2, nbdevdn=2, matype=0)

cc_5 = chart_5.iloc[-1] # pandas

ub_breakout = cc_5['high'] > cc_5['upperband']

lb_breakout = cc_5['low'] < cc_5['lowerband']

no_repeat_order = stock_name not in traded_wathclist

max_order_limit = len(traded_wathclist) <= max_trades

if uptrend and ub_breakout and no_repeat_order and max_order_limit:

print(stock_name, "is in uptrend, Buy this script")

sl_price = round((cc_1['close']*0.98),1)

qty = int(per_trade_margin/cc_1['close'])

buy_entry_orderid = tsl.order_placement(stock_name,'NSE', 1, 0, 0, 'MARKET', 'BUY', 'MIS')

sl_orderid = tsl.order_placement(stock_name,'NSE', 1, 0, sl_price, 'STOPMARKET', 'SELL', 'MIS')

traded_wathclist.append(stock_name)

if downtrend and lb_breakout and no_repeat_order and max_order_limit:

print(stock_name, "is in downtrend, Sell this script")

sl_price = round((cc_1['close']*1.02),1)

qty = int(per_trade_margin/cc_1['close'])

buy_entry_orderid = tsl.order_placement(stock_name,'NSE', 1, 0, 0, 'MARKET', 'SELL', 'MIS')

sl_orderid = tsl.order_placement(stock_name,'NSE', 1, 0, sl_price, 'STOPMARKET', 'BUY', 'MIS')

traded_wathclist.append(stock_name)

ERROR:

C:\Users\RP\Desktop\DHAN Algorhythemic Trading\8. Session8- 2nd Live Algo\2nd live Algo>py “Multi timeframe Algo.py”

Codebase Version 2.3 : Solved - ATM issues

-----Logged into Dhan-----

reading existing file all_instrument 2025-01-30.csv

Got the instrument file

Exception for instrument name HINDALCO INDUSTRIES as Check the Tradingsymbol

Exception for instrument name NIFTY BANK as Check the Tradingsymbol

got exception in pnl as ‘Hindalco Industries’

MOTHERSON

OFSS

MANAPPURAM

BSOFT

CHAMBLFERT

DIXON

NATIONALUM

DLF

IDEA

ADANIPORTS

SAIL

HINDCOPPER

INDIGO

RECLTD

PNB

HINDALCO

RBLBANK

GNFC

ALKEM

CONCOR

PFC

PFC is in uptrend, Buy this script

GODREJPROP

MARUTI

ADANIENT

ONGC

CANBK

OBEROIRLTY

BANDHANBNK

BANDHANBNK is in downtrend, Sell this script

SBIN

HINDPETRO

CANFINHOME

TATAMOTORS

LALPATHLAB

MCX

TATACHEM

BHARTIARTL

INDIAMART

LUPIN

INDUSTOWER

VEDL

SHRIRAMFIN

POLYCAB

WIPRO

UBL

SRF

BHARATFORG

GRASIM

IEX

BATAINDIA

AARTIIND

TATASTEEL

UPL

HDFCBANK

LTF

TVSMOTOR

GMRINFRA

Exception in Getting OHLC data as Check the Tradingsymbol or Exchange

Traceback (most recent call last):

File “Multi timeframe Algo.py”, line 57, in

chart_1[‘rsi’] = talib.RSI(chart_1[‘close’], timeperiod=14) #pandas

TypeError: ‘NoneType’ object is not subscriptable

Hi @SF_F

Check below code reference

import pdb

import time

import datetime

import traceback

from Dhan_Tradehull import Tradehull

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as ta

import xlwings as xw

import winsound

import sqn_lib

client_code = "1102790337"

token_id = "eyJ0eXAiOiJKV1QiLCJhbGciOiJIUzUxMiJ9.eyJpc3MiOiJkaGFuIiwicGFydG5lcklkIjoiIiwiZXhwIjoxNzM2ODYwMTMxLCJ0b2tlbkNvbnN1bWVyVHlwZSI6IlNFTEYiLCJ3ZWJob29rVXJsIjoiIiwiZGhhbkNsaWVudElkIjoiMTEwMjc5MDMzNyJ9.Leop6waGeVfmBOtczNEcjRWmC8pUGWQf54YPINGDi_PZjk1IvW-DDdaYXsgM_s8McOT44q4MjEQxGXU0lduK0A"

tsl = Tradehull(client_code,token_id)

opening_balance = 1005000 # tsl.get_balance()

base_capital = 1000000

market_money = opening_balance - base_capital

# beacuse I am loosing money, so I have 0 market money, and I can take risk on the current opening balance and not on the base capital

if (market_money < 0):

market_money = 0

base_capital = opening_balance

market_money_risk = (market_money*1)/100

base_capital_risk = (base_capital*0.5)/100

max_risk_for_today = base_capital_risk + market_money_risk

max_order_for_today = 2

risk_per_trade = (max_risk_for_today/max_order_for_today)

atr_multipler = 3

risk_reward = 3

watchlist = ['NIFTY', 'ADANIPORTS', 'ADANIENT', 'SBIN']

single_order = {'name':None, 'date':None , 'entry_time': None, 'entry_price': None, 'buy_sell': None, 'qty': None, 'sl': None, 'exit_time': None, 'exit_price': None, 'pnl': None, 'remark': None, 'traded':None}

orderbook = {}

wb = xw.Book('Live Trade Data.xlsx')

live_Trading = wb.sheets['Live_Trading']

completed_orders_sheet = wb.sheets['completed_orders']

reentry = "yes" #"yes/no"

completed_orders = []

bot_token = "8059847390:AAECSnQK-yOaGJ-clJchb1cx8CDhx2VQq-M"

receiver_chat_id = "1918451082"

live_Trading.range("A2:Z100").value = None

completed_orders_sheet.range("A2:Z100").value = None

for name in watchlist:

orderbook[name] = single_order.copy()

while True:

print("starting while Loop \n\n")

current_time = datetime.datetime.now().time()

if current_time < datetime.time(10, 15):

print(f"Wait for market to start", current_time)

time.sleep(1)

continue

live_pnl = tsl.get_live_pnl()

max_loss_hit = live_pnl < (max_risk_for_today*-1)

market_over = current_time > datetime.time(15, 15)

if max_loss_hit or market_over:

order_details = tsl.cancel_all_orders()

print(f"Market over Closing all trades !! Bye Bye See you Tomorrow", current_time)

pdb.set_trace()

break

all_ltp = tsl.get_ltp_data(names = watchlist)

for name in watchlist:

orderbook_df = pd.DataFrame(orderbook).T

live_Trading.range('A1').value = orderbook_df

completed_orders_df = pd.DataFrame(completed_orders)

completed_orders_sheet.range('A1').value = completed_orders_df

current_time = datetime.datetime.now()

print(f"Scanning {name} {current_time}")

try:

if name == "NIFTY":

exchange = "INDEX"

else:

exchange = "NSE"

chart = tsl.get_historical_data(tradingsymbol = name,exchange = exchange,timeframe="5")

chart['rsi'] = talib.RSI(chart['close'], timeperiod=14)

sqn_lib.sqn(df=chart, period=21)

chart['market_type'] = chart['sqn'].apply(sqn_lib.market_type)

chart['atr'] = talib.ATR(chart['high'], chart['low'], chart['close'], timeperiod=14)

cc = chart.iloc[-2]

no_of_orders_placed = orderbook_df[orderbook_df['qty'] > 0].shape[0] + completed_orders_df[completed_orders_df['qty'] > 0].shape[0]

# buy entry conditions

bc1 = cc['rsi'] > 1

bc2 = orderbook[name]['traded'] is None

bc3 = True # cc['market_type'] != "neutral"

bc4 = no_of_orders_placed < 5

except Exception as e:

print(e)

continue

if bc1 and bc2 and bc3:

print("buy ", name, "\t")

pdb.set_trace()

# margin_avialable = tsl.get_balance()

# margin_required = cc['close']/4.5

# if margin_avialable < margin_required:

# print(f"Less margin, not taking order : margin_avialable is {margin_avialable} and margin_required is {margin_required} for {name}")

# continue

ce_name, pe_name, ce_otm_strike, pe_otm_strike = tsl.OTM_Strike_Selection(Underlying='NIFTY', Expiry=0, OTM_count=2)

lot_size = tsl.get_lot_size(tradingsymbol = ce_name)

options_chart = tsl.get_historical_data(tradingsymbol = ce_name,exchange = 'NFO',timeframe="5")

options_chart['atr'] = talib.ATR(options_chart['high'], options_chart['low'], options_chart['close'], timeperiod=14)

rc_options = options_chart.iloc[-1]

orderbook[name]['name'] = name

orderbook[name]['options_name'] = ce_name

orderbook[name]['date'] = str(current_time.date())

orderbook[name]['entry_time'] = str(current_time.time())[:8]

orderbook[name]['max_holding_time'] = datetime.datetime.now() + datetime.timedelta(hours=2)

orderbook[name]['buy_sell'] = "BUY"

sl_points = rc_options['atr']*atr_multipler

orderbook[name]['qty'] = 25 # int(int((risk_per_trade*0.7)/sl_points)/lot_size)*lot_size

try:

entry_orderid = tsl.order_placement(tradingsymbol=orderbook[name]['options_name'] ,exchange='NFO', quantity=orderbook[name]['qty'], price=0, trigger_price=0, order_type='MARKET', transaction_type='BUY', trade_type='MIS')

orderbook[name]['entry_orderid'] = entry_orderid

orderbook[name]['entry_price'] = tsl.get_executed_price(orderid=orderbook[name]['entry_orderid'])

orderbook[name]['sl'] = round(orderbook[name]['entry_price'] - sl_points, 1) # 99

orderbook[name]['tsl'] = orderbook[name]['sl']

price = orderbook[name]['sl'] - 0.05

sl_orderid = tsl.order_placement(tradingsymbol=orderbook[name]['options_name'] ,exchange='NFO', quantity=orderbook[name]['qty'], price=price, trigger_price=orderbook[name]['sl'], order_type='STOPLIMIT', transaction_type ='SELL', trade_type='MIS')

orderbook[name]['sl_orderid'] = sl_orderid

orderbook[name]['traded'] = "yes"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"Entry_done {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

except Exception as e:

print(e)

pdb.set_trace(header= "error in entry order")

if orderbook[name]['traded'] == "yes":

bought = orderbook[name]['buy_sell'] == "BUY"

if bought:

try:

ltp = all_ltp[name]

sl_hit = tsl.get_order_status(orderid=orderbook[name]['sl_orderid']) == "TRADED"

holding_time_exceeded = datetime.datetime.now() > orderbook[name]['max_holding_time']

current_pnl = round((ltp - orderbook[name]['entry_price'])*orderbook[name]['qty'],1)

except Exception as e:

print(e)

pdb.set_trace(header = "error in sl order cheking")

if sl_hit:

try:

orderbook[name]['exit_time'] = str(current_time.time())[:8]

orderbook[name]['exit_price'] = tsl.get_executed_price(orderid=orderbook[name]['sl_orderid'])

orderbook[name]['pnl'] = round((orderbook[name]['exit_price'] - orderbook[name]['entry_price'])*orderbook[name]['qty'],1)

orderbook[name]['remark'] = "Bought_SL_hit"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"SL_HIT {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

if reentry == "yes":

completed_orders.append(orderbook[name])

orderbook[name] = None

except Exception as e:

print(e)

pdb.set_trace(header = "error in sl_hit")

if holding_time_exceeded and (current_pnl < 0):

try:

tsl.cancel_order(OrderID=orderbook[name]['sl_orderid'])

time.sleep(2)

square_off_buy_order = tsl.order_placement(tradingsymbol=orderbook[name]['name'] ,exchange='NSE', quantity=orderbook[name]['qty'], price=0, trigger_price=0, order_type='MARKET', transaction_type='SELL', trade_type='MIS')

orderbook[name]['exit_time'] = str(current_time.time())[:8]

orderbook[name]['exit_price'] = tsl.get_executed_price(orderid=square_off_buy_order)

orderbook[name]['pnl'] = (orderbook[name]['exit_price'] - orderbook[name]['entry_price'])*orderbook[name]['qty']

orderbook[name]['remark'] = "holding_time_exceeded_and_I_am_still_facing_loss"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"holding_time_exceeded_and_I_am_still_facing_loss {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

if reentry == "yes":

completed_orders.append(orderbook[name])

orderbook[name] = None

winsound.Beep(1500, 10000)

except Exception as e:

print(e)

pdb.set_trace(header = "error in tg_hit") # Testing changes. sadhasd ajsdas dbna sdb abs da sd asd abs d asd

options_name = orderbook[name]['options_name']

options_chart = tsl.get_historical_data(tradingsymbol = options_name,exchange = 'NFO',timeframe="5")

options_chart['atr'] = talib.ATR(options_chart['high'], options_chart['low'], options_chart['close'], timeperiod=14)

rc_options = options_chart.iloc[-1]

sl_points = rc_options['atr']*atr_multipler

options_ltp = tsl.get_ltp_data(names = options_name)[options_name]

tsl_level = options_ltp - sl_points

if tsl_level > orderbook[name]['tsl']:

trigger_price = round(tsl_level, 1)

price = trigger_price - 0.05

tsl.modify_order(order_id=orderbook[name]['sl_orderid'],order_type="STOPLIMIT",quantity=25,price=price,trigger_price=trigger_price)

orderbook[name]['tsl'] = tsl_level

# order_ids = tsl.place_slice_order(tradingsymbol="NIFTY 19 DEC 24400 CALL", exchange="NFO",quantity=10000, transaction_type="BUY",order_type="LIMIT",trade_type="MIS",price=0.05)

Use below code to manage exceptions

for stock_name in watchlist:

print(stock_name)

chart_1 = tsl.get_historical_data(tradingsymbol = stock_name,exchange = 'NSE',timeframe="1")

if chart_1 is None:

continue

chart_1['rsi'] = talib.RSI(chart_1['close'], timeperiod=14) #pandas

also remove GMRINFRA from watchlist

and use latest codebase file : Dhan_Tradehull_V2.py - Google Drive

Thank you so much for your kind & quick help ![]()

M&MFIN LTP SHOWN 2106.98 INSTEND OF CURRENT PRICE, PLEASE HELP. @Tradehull_Imran

Very Good Morning Sir.

Thank You very much for your correction.

I will let you know after trying this sir.

VBR Prasad

Sir I have suggested modification in the code. But Still I am getting the Error:

Modified Code:

for stock_name in watchlist:

time.sleep(0.2)

print(stock_name)

# Conditions that are on 1 minute timeframe

# chart_1 = tsl.get_intraday_data(stock_name, 'NSE', 1) # 1 minute chart # this call has been updated to get_historical_data call,

chart_1 = tsl.get_historical_data(tradingsymbol = stock_name,exchange = 'NSE',timeframe="1")

if chart_1 is none:

continue

chart_1['rsi'] = talib.RSI(chart_1['close'], timeperiod=14) #pandas

cc_1 = chart_1.iloc[-2] #pandas completed candle of 1 min timeframe

uptrend = cc_1['rsi'] > 60

downtrend = cc_1['rsi'] < 40

ERROR:

Codebase Version 2.3 : Solved - ATM issues

-----Logged into Dhan-----

This BOT Is Picking New File From Dhan

Got the instrument file

MOTHERSON

Traceback (most recent call last):

File “Multi timeframe Algo.py”, line 55, in

if chart_1 is none:

NameError: name ‘none’ is not defined

Please Suggest Sir.