Hi @rahulcse56 ,

The open source backtesting video will be released by this weekend.

Hi @rahulcse56 ,

The open source backtesting video will be released by this weekend.

Thanks @Tradehull_Imran ,

but, if possible can we get the strikes dynamic like, ITM, OTM as like this one,

because dynamix strikes will be much helpful and less tiresome.

atm, OC = tsl.get_option_chain(Underlying=“NIFTY”, exchange=“INDEX”, expiry=0, num_strikes=5)

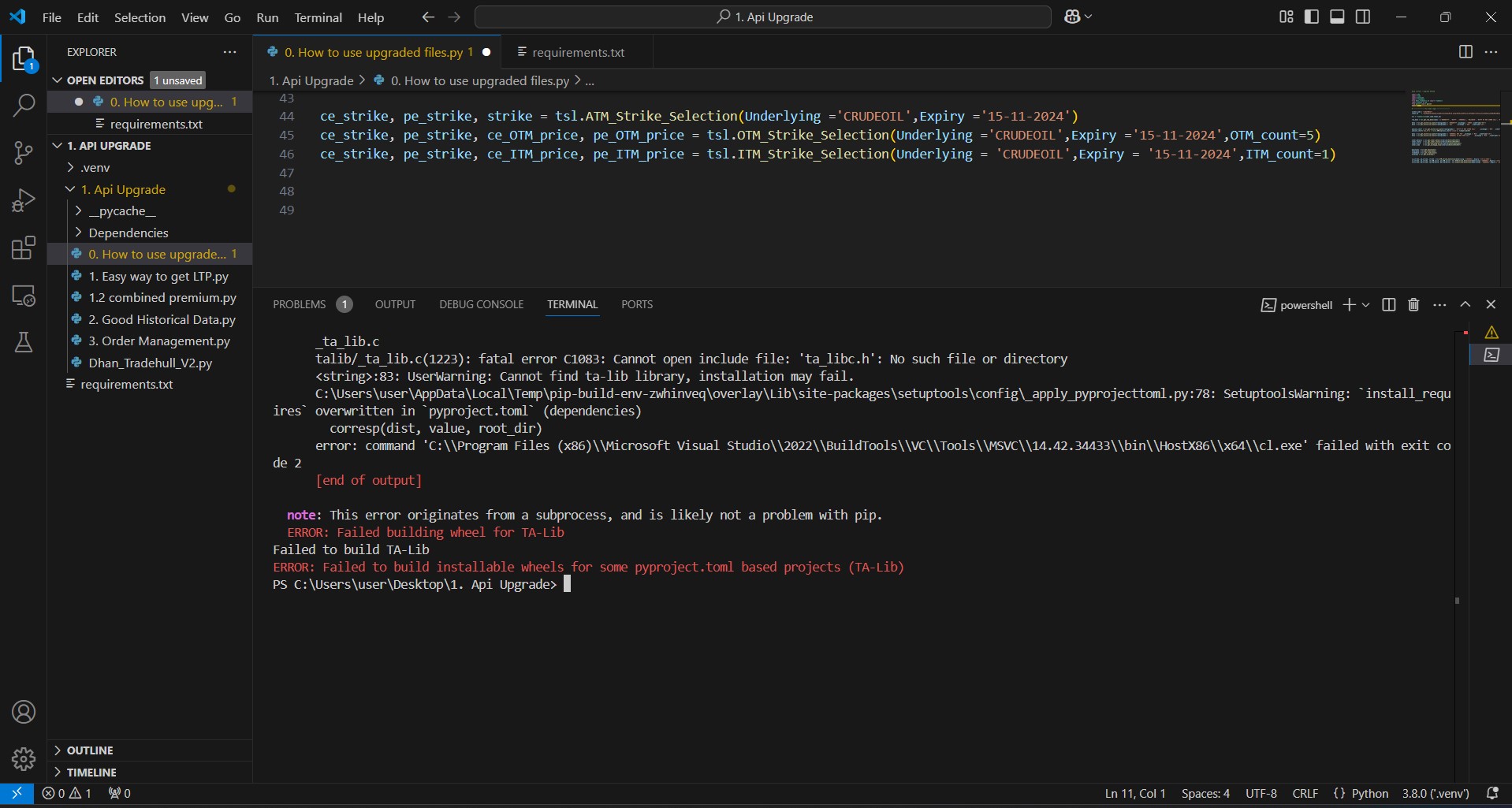

@Tradehull_Imran , I got this error while installing TA-lib, kindly help.

watchlist = [“COALINDIA”]

for stock_name in watchlist:

chart_5 = tsl.get_historical_data(stock_name, “NSE”, “5”)

if chart_5 is not None:

chart_5[“rsi”] = talib.RSI(chart_5[‘close’], timeperiod=14) #rsi

chart_5[‘average_volume’] = chart_5[‘volume’].rolling(window=20).mean() #average volume

chart_5.set_index(pd.DatetimeIndex(chart_5[‘timestamp’]), inplace=True) #vwap

chart_5[‘vwap’] = pta.vwap(chart_5[‘high’],chart_5[‘low’],chart_5[‘close’],chart_5[‘volume’])

indi = ta.supertrend(chart_5[‘high’],chart_5[‘low’],chart_5[‘close’],10,2) #supertrend

chart_5 = pd.concat([chart_5, indi],axis=1, join=‘inner’)

scanned_candle = chart_5.iloc[-2] #

breakout_candle = chart_5.iloc[-1] #.between_time("09:20","09:25")

first_candle = chart_5.between_time("9:15","09:15").iloc[-1]

sc1 = scanned_candle['rsi'] < 35 and scanned_candle['close'] < scanned_candle['SUPERT_10_2.0'] and scanned_candle['close'] < scanned_candle['vwap'] and scanned_candle['close'] < scanned_candle['open']

sc2 = breakout_candle['rsi'] < scanned_candle['rsi'] and breakout_candle['close'] < scanned_candle['low'] and breakout_candle['open'] > breakout_candle['close']

sc3 = breakout_candle['open'] > breakout_candle['close']

if sc1 and sc2 and sc3:

ltp = tsl.get_ltp_data(names=[stock_name])[stock_name]

print(f"sell this script {stock_name} at {scanned_candle['close']}")

ce_name, pe_name, strike = tsl.ATM_Strike_Selection(stock_name, Expiry=0)

ce_ltp = tsl.get_ltp_data(names=[ce_name])[ce_name]

# pdb.set_trace()

This error is solved now, it was mismatch of the wheel file version.

@Tradehull_Imran Sir, the tradingsymbol I executed does not match the tradingsymbol present in the get_positions() DataFrame. What is the solution? Please guide me.

excel_file = “Nifty1.xlsx”

try:

df = pd.read_excel(excel_file, sheet_name=‘trade_info’, engine=‘openpyxl’)

if df.empty:

time.sleep(1)

else:

for index, row in df.iterrows():

Strike = row['Strike Symbol']

entry = row['Entry Price']

target = row['target']

sl = row['SL Price']

# Get live market data for the current strike

data = tsl.get_ltp_data(Strike)

ltp = data.get(Strike, None)

lot_size = tsl.get_lot_size(Strike)

if ltp and ltp < sl:

active_positions = tsl.get_positions()

print(active_positions)

# If no active positions, directly check holdings

if active_positions is None or (isinstance(active_positions, pd.DataFrame) and active_positions.empty):

print(f"[{Strike}] No active positions found.")

else:

# Proceed with active position logic

active_Strike = active_positions[active_positions['tradingSymbol'] == Strike]

# Check if a SELL order already exists

if 'positionType' in active_positions.columns:

sell_order_exists = not active_Strike[active_Strike['positionType'] == "CLOSE"].empty

if sell_order_exists:

print(f"[{Strike}] Sell order already exists. Skipping.")

buy_Strike = active_Strike[active_Strike['positionType'] == "LONG"]

if not buy_Strike.empty:

quantity = buy_Strike.iloc[0].get('buyQty', 1) # Use 'buyQty'

print(f"[{Strike}] Buy position found with quantity: {quantity}. Placing sell order.")

orderid = tsl.order_placement(Strike, 'NFO', quantity, 0, 0, 'MARKET', 'SELL', 'MIS')

else:

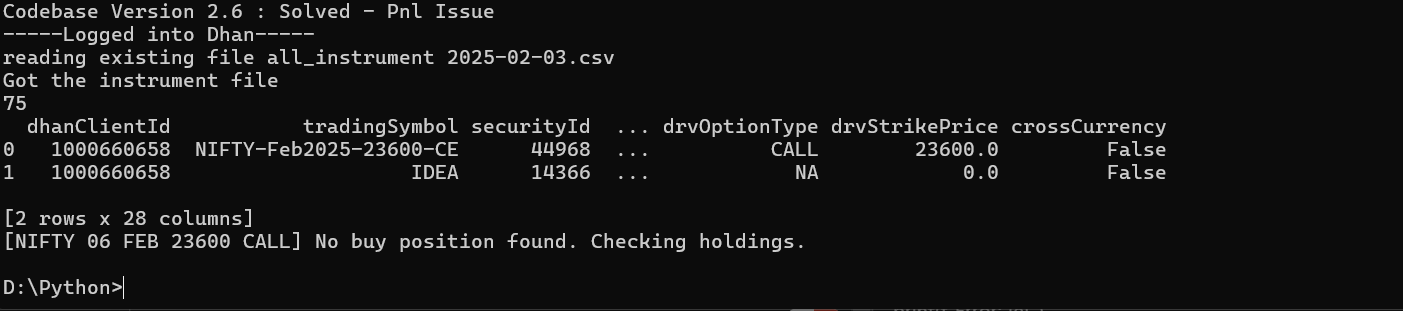

print(f"[{Strike}] No buy position found. Checking holdings.")

except Exception as e:

print(f"Error: {e}")

@Tradehull_Imran Is there a way to find out GAP UP/DOWN? Thanks

Sir, currently i have made it fast using threads, will seek help if needed any in future

@Tradehull_Imran one more, Is there an option to pick the expiry date of the index? I want my algo to trade only on the expiry day ![]()

@Tradehull_Imran Sir,

this solved my issues of fetching NIFTY data… thanks…

@Tradehull_Imran sir,

I am using -

data = tsl.get_historical_data(tradingsymbol=ce_strike, exchange=‘NSE’, timeframe=“5”)

to fetch the current expiry atm ce’s 5 min data. but getting error. Pls correct it.

Thanks.

Hi @anandc ,

The code seems to be working fine, can you mention for which ce_strike are you getting error?

@Tradehull_Imran sir,

CE STRIKE= NIFTY 06 FEB 23550 CALL

PE STRIKE= NIFTY 06 FEB 23550 PUT

data = tsl.get_historical_data(tradingsymbol=ce_strike, exchange=‘NSE’, timeframe=“5”)

Error-

Exception in Getting OHLC data as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: ‘DH-907’, ‘error_type’: ‘Data_Error’, ‘error_message’: ‘System is unable to fetch data due to incorrect parameters or no data present’}, ‘data’: {‘errorType’: ‘Data_Error’, ‘errorCode’: ‘DH-907’, ‘errorMessage’: ‘System is unable to fetch data due to incorrect parameters or no data present’}}

I tried by removing the “CALL” or “PUT” from the CE_STRIKE variable…? Still unable to fetch the data

Hi @Akshay_Bawane ,

Couldn’t understand your query, do elaborate your questions.

For my understanding, you can dynamically pass the strike names to get the oi as below:

atm, OC = tsl.get_option_chain(Underlying=“NIFTY”, exchange=“INDEX”, expiry=0, num_strikes=5)

ce_quote = tsl.get_quote([atm])

ce_oi = ce_quote[ce_otm]['oi']

Hi @Kanha_Meher ,

It appears that the code is attempting to retrieve the tradingsymbol from the positions DataFrame using the strike value. However, due to differences in naming conventions, the match is not successful.

Hi @anandc ,

Do change the exchange from “NSE” to “NFO”

data = tsl.get_historical_data(tradingsymbol=ce_strike, exchange='NFO', timeframe='5')

Refer the below code:

data = tsl.get_quote(names=['NIFTY'])

open_price = data['NIFTY']['ohlc']['open']

close_price = data['NIFTY']['ohlc']['close']

gap_up = open_price - close_price

refer the below code to get the list of expiries:

expiry_list = tsl.get_expiry_list("NIFTY", "NSE")

Hi @Abhishek_Pawde ,

We have fixed this issue, do use the upgraded codebase:

https://drive.google.com/file/d/1h8J6VOLrHMAaF1NGP4_vJj2wtkNxfPDw/view@Tradehull_Imran Sir,

Now working perfectly as expected… Thanks a lot sir…