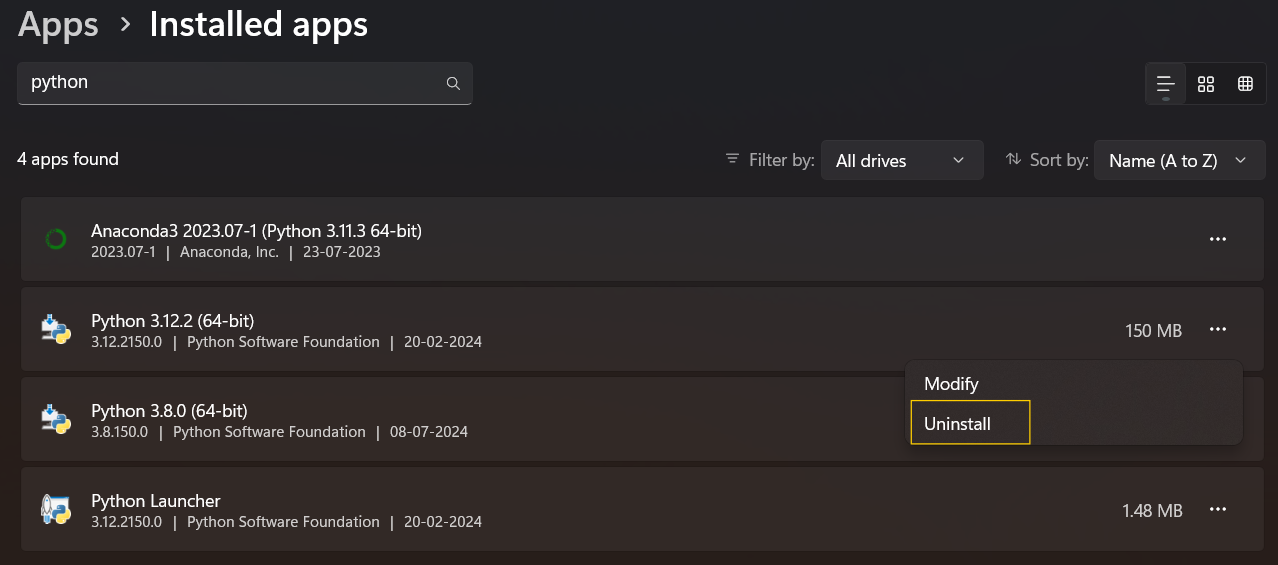

Hi @Kusum_Kapadia ,

Firstly do uninstall existing versions as below:

- Press

Win + Ito open Settings. - Go to Apps > Installed apps (or Apps & Features).

- Search for Python.

- Click Uninstall for each Python version.

- Follow the prompts to remove it.

Hi @Kusum_Kapadia ,

Firstly do uninstall existing versions as below:

Win + I to open Settings.Hi @amitbalagi ,

Do update codebase on your system

Guide to use the updated codebase:

Video reference : https://www.youtube.com/watch?v=P9iPYShakbA

Hi @Raju2 ,

In our latest codebase, the num_strikes parameter is not available for use.

You can retrieve the option chain using the following code:

option_chain = tsl.get_option_chain(Underlying=“NIFTY”, exchange=“INDEX”, expiry=0)

We will be adding num_strikes in further versions. You can use the below code if you wish to do it manually:

num_strikes = 10

strike_step = 50

CE_symbol_name, PE_symbol_name, atm_strike = tsl.ATM_Strike_Selection(Underlying='NIFTY', Expiry=0)

oc_df = tsl.get_option_chain(Underlying="NIFTY", exchange="INDEX", expiry=0)

df = oc_df[(oc_df['Strike Price'] >= str(atm_strike - num_strikes * strike_step)) & (oc_df['Strike Price'] <= atm_strike + num_strikes * strike_step)].sort_values(by='Strike Price').reset_index(drop=True)

Hi @rahulcse56 ,

Steps to be followed to get INDIAVIX Ltp:

pip show Dhan-TradeHull

get_ltp_data() function.exchange_index = {"BANKNIFTY": "NSE_IDX", "NIFTY":"NSE_IDX", "MIDCPNIFTY":"NSE_IDX", "FINNIFTY":"NSE_IDX", "SENSEX":"BSE_IDX", "BANKEX":"BSE_IDX", "INDIA VIX":"IDX_I"}

Note : This will be upgraded in further versions

Hi @Qaisar ,

Solution link :

https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718/2637?u=tradehull_imran

Dear sir

how to save in excel sheet of enter order price ,sl/ target price of algo.

please guide us.

I had already saw your post and updated dhan-tradehull. see below the pip show dhan-tradehull output for your reference.

PS C:\Users\amitb\Desktop\Python> pip show dhan-tradehull

Name: Dhan_Tradehull

Version: 3.0.2

Summary: A Dhan Codebase from TradeHull

Home-page: https://github.com/TradeHull/Dhan_Tradehull

Author: TradeHull

Author-email: contact.tradehull@gmail.com

License:

Location: c:\users\amitb\appdata\roaming\python\python310\site-packages

Requires: dhanhq, mibian, numpy, pandas, pytz, requests

Required-by:

PS C:\Users\amitb\Desktop\Python>

Then I ran the same file from 2 different locations, in one i got the same error as before while in other problem was resolved.

import sys

import winsound

import dhan_user_functions

from Dhan_Tradehull_V2 import Tradehull

from datetime import datetime,timedelta

import time

import math

import requests

import pandas as pd

import threading

import datetime as dt

import talib

import logging

# Set up logging

logging.basicConfig(level=logging.INFO, format='%(asctime)s - %(levelname)s - %(message)s')

logging.info(f"Now logging to Dhan Account.")

client_code = open("dhan_client_id.txt",'r').read() #'clientID'

token_id = open("dhan_access_token.txt",'r').read() #'accessToken'

tsl = Tradehull(client_code,token_id)

# tsl = Tradehull(client_code,token_id)

logging.info(f"Successfully logged in to Dhan Account.")

name = 'NIFTY'

chart = tsl.get_historical_data(name, exchange='INDEX', timeframe='5')

# chart = tsl.get_historical_data(tradingsymbol = 'NIFTY',exchange = 'INDEX',timeframe="5")

# chart = chart.set_index(chart['timestamp'])

print("chart is \n", chart)

then the output from 1st location is as below:

"C:\Program Files\Python310\python.exe" C:\Users\amitb\Desktop\Python\dump.py

Codebase Version 2.8 : Solved - Strike Selection Issue

-----Logged into Dhan-----

reading existing file all_instrument 2025-02-19.csv

2025-02-19 19:00:25,077 - INFO - Now logging to Dhan Account.

2025-02-19 19:00:25,078 - INFO - Dhan.py started system

2025-02-19 19:00:25,078 - INFO - STARTED THE PROGRAM

Got the instrument file

2025-02-19 19:00:25,210 - ERROR - Error at getting start date as single positional indexer is out-of-bounds

Traceback (most recent call last):

File "C:\Users\amitb\Desktop\Python\Dhan_Tradehull_V2.py", line 431, in get_start_date

security_id = instrument_df[((instrument_df['SEM_TRADING_SYMBOL']==tradingsymbol)|(instrument_df['SEM_CUSTOM_SYMBOL']==tradingsymbol))&(instrument_df['SEM_EXM_EXCH_ID']==instrument_exchange[exchange])].iloc[-1]['SEM_SMST_SECURITY_ID']

File "C:\Users\amitb\AppData\Roaming\Python\Python310\site-packages\pandas\core\indexing.py", line 1191, in __getitem__

return self._getitem_axis(maybe_callable, axis=axis)

File "C:\Users\amitb\AppData\Roaming\Python\Python310\site-packages\pandas\core\indexing.py", line 1752, in _getitem_axis

self._validate_integer(key, axis)

File "C:\Users\amitb\AppData\Roaming\Python\Python310\site-packages\pandas\core\indexing.py", line 1685, in _validate_integer

raise IndexError("single positional indexer is out-of-bounds")

IndexError: single positional indexer is out-of-bounds

2025-02-19 19:00:25,213 - INFO - Successfully logged in to Dhan Account.

2025-02-19 19:00:25,224 - ERROR - Exception in Getting OHLC data as Check the Tradingsymbol or Exchange

Traceback (most recent call last):

File "C:\Users\amitb\Desktop\Python\Dhan_Tradehull_V2.py", line 476, in get_historical_data

raise Exception("Check the Tradingsymbol or Exchange")

Exception: Check the Tradingsymbol or Exchange

Exception in Getting OHLC data as Check the Tradingsymbol or Exchange

chart is

None

Process finished with exit code 0

while from another location, the output is as below:

"C:\Program Files\Python310\python.exe" "C:\Users\amitb\Desktop\Python\2. API Traders Meetup & Workshop - Building Blocks\Session 1\dump.py"

Codebase Version 2.8 : Solved - Strike Selection Issue

2025-02-19 19:03:30,281 - INFO - Now logging to Dhan Account.

2025-02-19 19:03:30,283 - INFO - Dhan.py started system

2025-02-19 19:03:30,283 - INFO - STARTED THE PROGRAM

-----Logged into Dhan-----

reading existing file all_instrument 2025-02-19.csv

Got the instrument file

2025-02-19 19:03:32,017 - INFO - Successfully logged in to Dhan Account.

chart is

open high ... volume timestamp

0 22809.900391 22835.50 ... 0.0 2025-02-17 09:15:00+05:30

1 22806.050000 22873.75 ... 0.0 2025-02-17 09:20:00+05:30

2 22842.000000 22874.75 ... 0.0 2025-02-17 09:25:00+05:30

3 22830.350000 22839.45 ... 0.0 2025-02-17 09:30:00+05:30

4 22805.650000 22824.35 ... 0.0 2025-02-17 09:35:00+05:30

.. ... ... ... ... ...

221 22946.550000 22949.15 ... 0.0 2025-02-19 15:10:00+05:30

222 22940.050000 22940.20 ... 0.0 2025-02-19 15:15:00+05:30

223 22931.250000 22932.60 ... 0.0 2025-02-19 15:20:00+05:30

224 22926.450000 22933.25 ... 0.0 2025-02-19 15:25:00+05:30

225 22932.900000 22932.90 ... 0.0 2025-02-19 17:50:00+05:30

[226 rows x 6 columns]

Process finished with exit code 0

@Tradehull_Imran Sir there is no reply from the @Hardik and please help for the same and i have another concern can you tell me the limit of the api hit per sec because if i try to fetch the data of the 200 stocks i build my own screener and i used threading it giving me the error that limit reached error Exception in Getting OHLC data as {'status': 'failure', 'remarks': {'error_code': 'DH-904', 'error_type': 'Rate_Limit', 'error_message': 'Too many requests on server from single user breaching rate limits. Try throttling API calls.'}, 'data': {'errorType': 'Rate_Limit', 'errorCode': 'DH-904', 'errorMessage': 'Too many requests on server from single user breaching rate limits. Try throttling API calls.'}} Error fetching data for APOLLOHOSP: 'NoneType' object has no attribute 'empty'

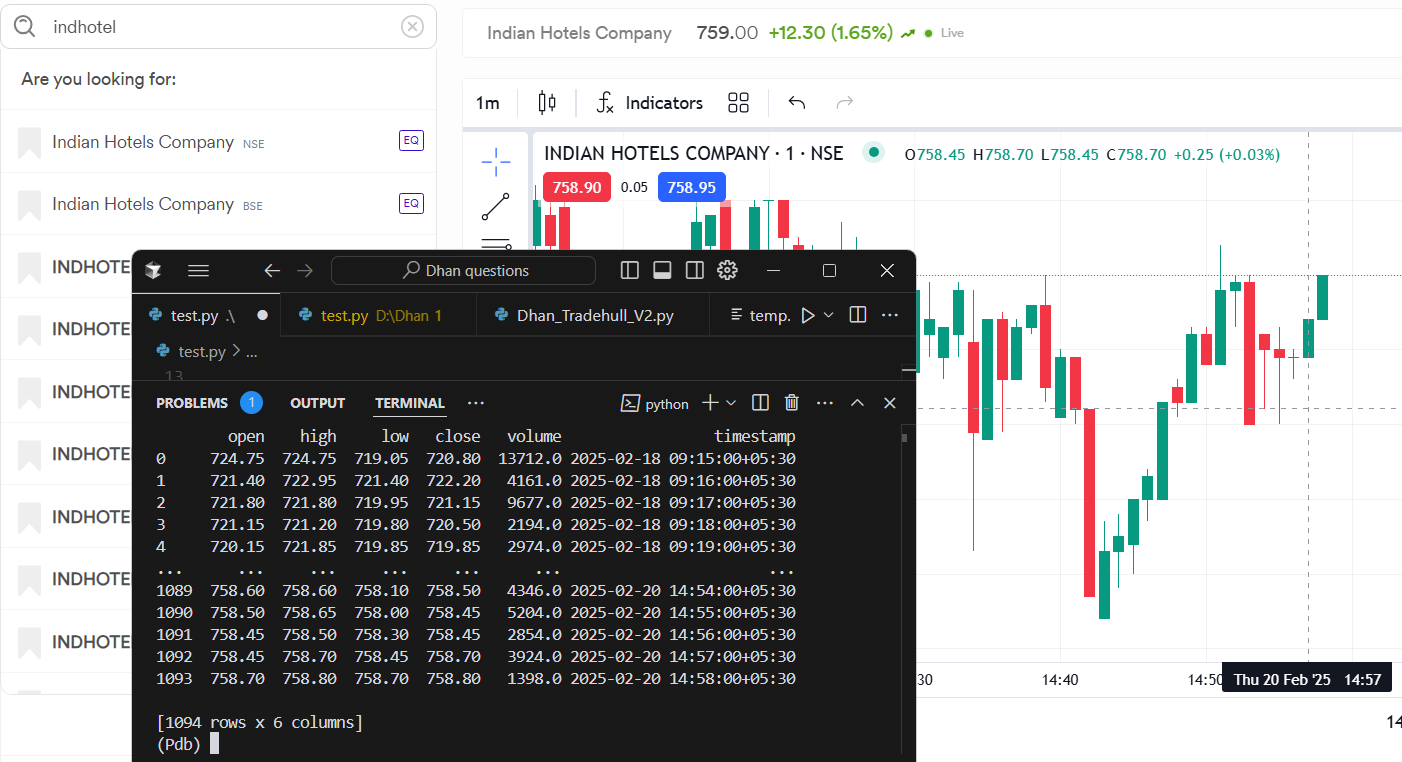

@Tradehull_Imran

ye dhan kya data de rha h ki chart ka data fetch kar rhe h api ke through

usme or aj ke char me jamin asman ka antar h esa nhi h ki ek hi char me h bhot chart me h GNFC , CONCOR , DELHIVERY , INDHOTEL or bhi bhot h @Hardik iska jawab do bhi ye to bhot bekar chiz h ye GFC ke chart ka bej rha hun or please jara actul chart ka difference ja ke dekho

| open | high | low | close | volume | timestamp | |

|---|---|---|---|---|---|---|

| 750 | 547.50 | 547.50 | 536.70 | 545.15 | 22229.0 | 2025-02-20 09:15:00+05:30 |

| 751 | 547.45 | 547.45 | 542.80 | 545.15 | 3286.0 | 2025-02-20 09:16:00+05:30 |

| 752 | 544.55 | 545.55 | 544.00 | 544.15 | 1838.0 | 2025-02-20 09:17:00+05:30 |

Hello @Dev_Goswami

Can you please share the request for this and also Security ID for which you are trying to fetch the data. If there were issues in data for companies highlighted by you, then even charts would have shown the same data as the source of both remains the same.

Also, do check if you have actually updated security ID list for today.

Currently, we only have daily timeframe data available for backtesting. But we are working on this to help you with minute timeframe of larger time period.

Arre, there’s no need for the Security ID now since data is being fetched using the symbol after the update. chart = tsl.get_historical_data(tradingsymbol="GNFC", exchange='NSE', timeframe="1") df_filtered = chart[chart["timestamp"] >= "2025-02-20 09:15:00+05:30"] df_filtered

| open | high | low | close | volume | timestamp | |

|---|---|---|---|---|---|---|

| 750 | 547.50 | 547.50 | 536.70 | 545.15 | 22229.0 | 2025-02-20 09:15:00+05:30 |

| 751 | 547.45 | 547.45 | 542.80 | 545.15 | 3286.0 | 2025-02-20 09:16:00+05:30 |

| 752 | 544.55 | 545.55 | 544.00 | 544.15 | 1838.0 | 2025-02-20 09:17:00+05:30 |

| now go and check the today GNFC chart and same issue with these company as well CONCOR , DELHIVERY , INDHOTEL @Tradehull_Imran |

Hello @Tradehull_Imran @Hardik

order_id = tsl.order_placement(tradingsymbol=‘NIFTY 20 FEB 26000 CALL’, exchange=‘NFO’, quantity=75, price=0, trigger_price=0, order_type=‘MARKET’, transaction_type=‘BUY’, trade_type=‘MIS’, disclosed_quantity=0, after_market_order=False, amo_time=‘OPEN’)

trade_type=‘MIS’ :- ABLE TO PLACE INTRDAYORDER

trade_type=‘CNC’ :- GETTING DH-906

trade_type=‘NRML’ :- Got exception in place_order as 'NRML

I can see we place Intraday options trade

*but do we have support for options delivery trades ???

example NIFTY 20 FEB 26000 CALL and trade_type CNC or NRML ???

Hi @Deodas_kumar ,

Refer the below code:

import xlwings as xw

wb = xw.Book('Live Trade Data.xlsx')

live_Trading = wb.sheets['Live_Trading'] # 'Live_Trading' is the excel sheet name.

orderbook = {}

# add other parameters to orderbook to send to excel sheet

orderbook['name'] = name

orderbook['date'] = str(current_time.date())

orderbook['entry_time'] = str(current_time.time())[:8]

orderbook['buy_sell'] = "BUY"

orderbook['qty'] = 1

# In the below code, we are converting to dataframe and sending to excel sheet

orderbook_df = pd.DataFrame(orderbook).T

live_Trading.range('A1').value = orderbook_df

refer the complete code as below:

import pdb

import time

import datetime

import traceback

from Dhan_Tradehull import Tradehull

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as ta

import xlwings as xw

import winsound

client_code = "1102790337"

token_id = "bhgvsaoieqhjvhg"

tsl = Tradehull(client_code,token_id)

# Uncomment below code to do pre market scanning

# pre_market_watchlist = ['ASIANPAINT', 'BAJAJ-AUTO', 'BERGEPAINT', 'BEL', 'BOSCHLTD', 'BRITANNIA', 'COALINDIA', 'COLPAL', 'DABUR', 'DIVISLAB', 'EICHERMOT', 'GODREJCP', 'HCLTECH', 'HDFCBANK', 'HAVELLS', 'HEROMOTOCO', 'HAL', 'HINDUNILVR', 'ITC', 'IRCTC', 'INFY', 'LTIM', 'MARICO', 'MARUTI', 'NESTLEIND', 'PIDILITIND', 'TCS', 'TECHM', 'WIPRO']

# watchlist = []

# for name in pre_market_watchlist:

# print("Pre market scanning ", name)

# day_chart = tsl.get_historical_data(tradingsymbol = name,exchange = 'NSE',timeframe="DAY")

# day_chart['upperband'], day_chart['middleband'], day_chart['lowerband'] = talib.BBANDS(day_chart['close'], timeperiod=20, nbdevup=2, nbdevdn=2, matype=0)

# last_day_candle = day_chart.iloc[-1]

# upper_breakout = last_day_candle['high'] > last_day_candle['upperband']

# lower_breakout = last_day_candle['low'] < last_day_candle['lowerband']

# if upper_breakout or lower_breakout:

# watchlist.append(name)

# print(f"\t selected {name} for trading")

# pdb.set_trace()

# print(watchlist)

# # pdb.set_trace()

watchlist = ['BEL', 'BOSCHLTD', 'COLPAL', 'HCLTECH', 'HDFCBANK', 'HAVELLS', 'HAL', 'ITC', 'IRCTC', 'INFY', 'LTIM', 'MARICO', 'MARUTI', 'NESTLEIND', 'PIDILITIND', 'TCS', 'TECHM', 'WIPRO']

single_order = {'name':None, 'date':None , 'entry_time': None, 'entry_price': None, 'buy_sell': None, 'qty': None, 'sl': None, 'exit_time': None, 'exit_price': None, 'pnl': None, 'remark': None, 'traded':None}

orderbook = {}

wb = xw.Book('Live Trade Data.xlsx')

live_Trading = wb.sheets['Live_Trading']

completed_orders_sheet = wb.sheets['completed_orders']

reentry = "yes" #"yes/no"

completed_orders = []

bot_token = "8059847390:AAECSnQK-yOaGJ-clJchb1cx8CDhx2VQq-M"

receiver_chat_id = "1918451082"

live_Trading.range("A2:Z100").value = None

completed_orders_sheet.range("A2:Z100").value = None

for name in watchlist:

orderbook[name] = single_order.copy()

while True:

print("starting while Loop \n\n")

current_time = datetime.datetime.now().time()

if current_time < datetime.time(13, 55):

print(f"Wait for market to start", current_time)

time.sleep(1)

continue

if current_time > datetime.time(15, 15):

order_details = tsl.cancel_all_orders()

print(f"Market over Closing all trades !! Bye Bye See you Tomorrow", current_time)

pdb.set_trace()

break

all_ltp = tsl.get_ltp_data(names = watchlist)

for name in watchlist:

orderbook_df = pd.DataFrame(orderbook).T

live_Trading.range('A1').value = orderbook_df

completed_orders_df = pd.DataFrame(completed_orders)

completed_orders_sheet.range('A1').value = completed_orders_df

current_time = datetime.datetime.now()

print(f"Scanning {name} {current_time}")

try:

chart = tsl.get_historical_data(tradingsymbol = name,exchange = 'NSE',timeframe="5")

chart['rsi'] = talib.RSI(chart['close'], timeperiod=14)

cc = chart.iloc[-2]

# buy entry conditions

bc1 = cc['rsi'] > 45

bc2 = orderbook[name]['traded'] is None

except Exception as e:

print(e)

continue

if bc1 and bc2:

print("buy ", name, "\t")

margin_avialable = tsl.get_balance()

margin_required = cc['close']/4.5

if margin_avialable < margin_required:

print(f"Less margin, not taking order : margin_avialable is {margin_avialable} and margin_required is {margin_required} for {name}")

continue

orderbook[name]['name'] = name

orderbook[name]['date'] = str(current_time.date())

orderbook[name]['entry_time'] = str(current_time.time())[:8]

orderbook[name]['buy_sell'] = "BUY"

orderbook[name]['qty'] = 1

try:

entry_orderid = tsl.order_placement(tradingsymbol=name ,exchange='NSE', quantity=orderbook[name]['qty'], price=0, trigger_price=0, order_type='MARKET', transaction_type='BUY', trade_type='MIS')

orderbook[name]['entry_orderid'] = entry_orderid

orderbook[name]['entry_price'] = tsl.get_executed_price(orderid=orderbook[name]['entry_orderid'])

orderbook[name]['tg'] = round(orderbook[name]['entry_price']*1.002, 1) # 1.01

orderbook[name]['sl'] = round(orderbook[name]['entry_price']*0.998, 1) # 99

sl_orderid = tsl.order_placement(tradingsymbol=name ,exchange='NSE', quantity=orderbook[name]['qty'], price=0, trigger_price=orderbook[name]['sl'], order_type='STOPMARKET', transaction_type ='SELL', trade_type='MIS')

orderbook[name]['sl_orderid'] = sl_orderid

orderbook[name]['traded'] = "yes"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"Entry_done {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

except Exception as e:

print(e)

pdb.set_trace(header= "error in entry order")

if orderbook[name]['traded'] == "yes":

bought = orderbook[name]['buy_sell'] == "BUY"

if bought:

try:

ltp = all_ltp[name]

sl_hit = tsl.get_order_status(orderid=orderbook[name]['sl_orderid']) == "TRADED"

tg_hit = ltp > orderbook[name]['tg']

except Exception as e:

print(e)

pdb.set_trace(header = "error in sl order cheking")

if sl_hit:

try:

orderbook[name]['exit_time'] = str(current_time.time())[:8]

orderbook[name]['exit_price'] = tsl.get_executed_price(orderid=orderbook[name]['sl_orderid'])

orderbook[name]['pnl'] = round((orderbook[name]['exit_price'] - orderbook[name]['entry_price'])*orderbook[name]['qty'],1)

orderbook[name]['remark'] = "Bought_SL_hit"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"SL_HIT {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

if reentry == "yes":

completed_orders.append(orderbook[name])

orderbook[name] = None

except Exception as e:

print(e)

pdb.set_trace(header = "error in sl_hit")

if tg_hit:

try:

tsl.cancel_order(OrderID=orderbook[name]['sl_orderid'])

time.sleep(2)

square_off_buy_order = tsl.order_placement(tradingsymbol=orderbook[name]['name'] ,exchange='NSE', quantity=orderbook[name]['qty'], price=0, trigger_price=0, order_type='MARKET', transaction_type='SELL', trade_type='MIS')

orderbook[name]['exit_time'] = str(current_time.time())[:8]

orderbook[name]['exit_price'] = tsl.get_executed_price(orderid=square_off_buy_order)

orderbook[name]['pnl'] = (orderbook[name]['exit_price'] - orderbook[name]['entry_price'])*orderbook[name]['qty']

orderbook[name]['remark'] = "Bought_TG_hit"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"TG_HIT {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

if reentry == "yes":

completed_orders.append(orderbook[name])

orderbook[name] = None

winsound.Beep(1500, 10000)

except Exception as e:

print(e)

pdb.set_trace(header = "error in tg_hit")

Hi @amitbalagi ,

Okay

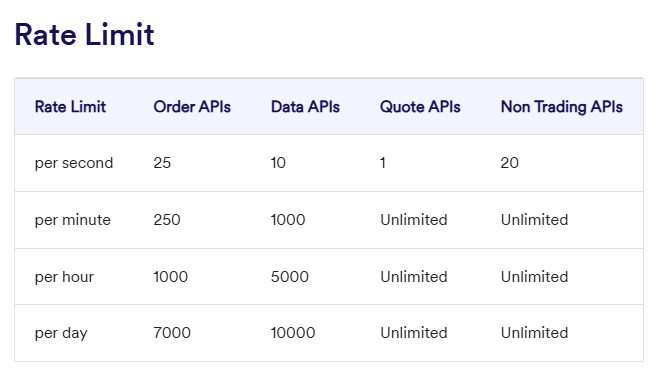

Hi @Dev_Goswami ,

It seems the data is matching accurately with the charts. Attaching the screenshot below do check.

Hi @Dev_Goswami ,

Here’s the screenshot of rate limits:

Do check this link:

Introduction - DhanHQ Ver 2.0 / API Document

Hi @Manish1 ,

Can you share screenshot of the terminal when you try to place for ‘CNC’ order.

Hi @anandc

Refer the below link for the code:

Hi @Subhajitpanja .

Refer the below link for the code:

Thank you @Tradehull_Imran sir

but I like to follow your video instructions only to write code.

I asked that one for a mate (here) who was seeking for it