@Tradehull_Imran

Hi @Tradehull_Imran sir,

kaise hai ap ap ke help se mai ek chota sa algo banaya hai iske liye thank you but sir is me ek error rha hai

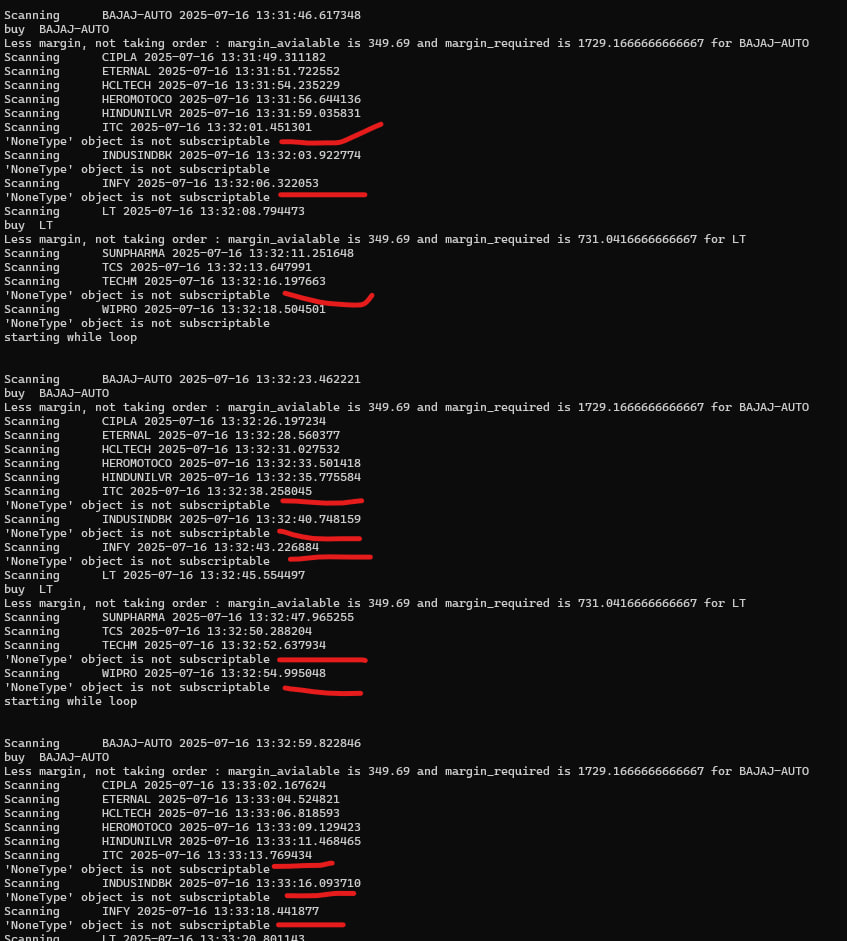

- ek bar tg or sl hit hone pr same stock ki scanning or reentry pr( ‘NoneType’ object is not subscriptable ) aisa error ata hai to mughe algo retart krna prta hai.

- mughe isme ema_21 add krna hai aur buy break candle agar ema ke upar closed ho aur second candle break krne pr buy ho. same iska apposit sell ke liye.

- agar previous week ka low ka SL hit or next to next day (2 or # 3days in the week) market reverse ho to 1h ka time pr previous week Low & ema ke upar closed ke second candle pr buy ho ( tg 1:2 & weekly call rahega.

please help & share code proper testing

Error:

Scanning CIPLA 2025-07-17 12:47:58.276160

'NoneType' object is not subscriptable

Scanning HCLTECH 2025-07-17 12:48:00.633788

Scanning HEROMOTOCO 2025-07-17 12:48:02.988629

Scanning ITC 2025-07-17 12:48:05.346589

Scanning INDUSINDBK 2025-07-17 12:48:08.742576

Scanning LT 2025-07-17 12:48:11.029972

code :

import pdb

import time

import datetime

import traceback

from Dhan_Tradehull_V2 import Tradehull

import pandas as pd

import xlwings as xw

from pprint import pprint

import talib

import pandas_ta as ta

import winsound

client_code = "xxxxxx"

token_id = "xxxxxxxxxxx"

tsl = Tradehull(client_code,token_id)

pre_market_watchlist = ['ADANIENT', 'ADANIPORTS', 'APOLLOHOSP', 'ASIANPAINT', 'AXISBANK', 'BAJAJ-AUTO', 'BAJFINANCE', 'BAJAJFINSV', 'BEL', 'BHARTIARTL', 'CIPLA', 'COALINDIA', 'DRREDDY', 'EICHERMOT', 'ETERNAL', 'GRASIM', 'HCLTECH', 'HDFCBANK', 'HDFCLIFE', 'HEROMOTOCO', 'HINDALCO', 'HINDUNILVR', 'ICICIBANK', 'ITC', 'INDUSINDBK', 'INFY', 'JSWSTEEL', 'JIOFIN', 'KOTAKBANK', 'LT', 'M&M', 'MARUTI', 'NTPC', 'NESTLEIND', 'ONGC', 'POWERGRID', 'RELIANCE', 'SBILIFE', 'SHRIRAMFIN', 'SBIN', 'SUNPHARMA', 'TCS', 'TATACONSUM', 'TATAMOTORS', 'TATASTEEL', 'TECHM', 'TITAN', 'TRENT', 'ULTRACEMCO', 'WIPRO']

watchlist = []

for name in pre_market_watchlist:

print("Pre market scanning ", name)

day_chart = tsl.get_historical_data(tradingsymbol = name,exchange = 'NSE',timeframe="DAY")

# indi = ta.supertrend(day_chart['high'], day_chart['low'], day_chart['close'], 10, 2) # appy suppertrand

# day_chart = pd.concat([day_chart, indi], axis=1, join='inner')

# if day_chart.iloc[-1]['SUPERTd_10_2.0'] == 1:

# watchlist.append(name)

day_chart['upperband'], day_chart['middleband'], day_chart['lowerband'] = talib.BBANDS(day_chart['close'], timeperiod=20, nbdevup=2, nbdevdn=2, matype=0)

last_dat_candle = day_chart.iloc[-1]

upper_breakout = last_dat_candle['high'] > last_dat_candle['upperband']

lower_breakout = last_dat_candle['low'] < last_dat_candle['lowerband']

if upper_breakout or lower_breakout:

watchlist.append(name)

print(f"\t selected {name} for trading")

print(watchlist)

# pdb.set_trace()

single_order = {'name' :None , 'date' :None , 'entry_time' :None , 'entry_price' :None , 'buy_sell' :None , 'qty' :None , 'sl' :None , 'exit_time' :None , 'exit_price' :None , 'pnl' :None , 'remark' :None , 'traded' :None , 'pyramiding' :None , 'Traling' :None ,}

orderbook = {}

wb = xw.Book('Live Trade Data.xlsx')

live_Trading = wb.sheets['Live_Trading']

completed_orders_sheet = wb.sheets['completed_orders']

reentry = "yes" #"yes/no"

completed_orders = []

bot_token = "7747163783:AAHV4vxVsAewDmzNDQFcSeCA3b9t8df9-sE"

receiver_chat_id = "5490108905"

live_Trading.range("A2:Z100").value = None

completed_orders_sheet.range("A2:Z100").value = None

for name in watchlist:

orderbook[name] = single_order.copy()

while True:

print("starting while loop \n\n")

current_time = datetime.datetime.now().time()

if current_time < datetime.time(9, 20):

print(f"wait for market to start", current_time)

time.sleep(1)

continue

if current_time > datetime.time(15, 15):

order_details = tsl.cancel_all_orders()

print(f"Market over closing all trades !! Bye Bye See you Tomorrow", current_time)

pdb.set_trace()

break

all_ltp = tsl.get_ltp_data(names = watchlist)

for name in watchlist:

orderbook_df = pd.DataFrame(orderbook).T

live_Trading.range('A1').value = orderbook_df

completed_orders_df = pd.DataFrame(completed_orders)

completed_orders_sheet.range('A1').value = completed_orders_df

current_time = datetime.datetime.now()

print(f"Scanning {name} {current_time}")

try:

chart = tsl.get_historical_data(tradingsymbol = name,exchange = 'NSE',timeframe="5")

chart['rsi'] = talib.RSI(chart['close'], timeperiod=14)

chart['ema'] = talib.EMA(chart['close'], timeperiod=21)

indi = ta.supertrend(chart['high'], chart['low'], chart['close'], 7, 3)

chart = pd.concat([chart, indi], axis=1, join='inner')

cc = chart.iloc[-2]

bc1 = cc['rsi'] > 60

bc2 = cc['SUPERTd_7_3.0'] == 1

bc3 = True # cc['ema'] > chart['ema'].iloc[-2]

bc4 = orderbook[name]['traded'] is None

# sc1 = cc['rsi'] < 40

# sc2 = orderbook[name]['traded'] is None

except Exception as e:

print(e)

continue

if bc1 and bc2 and bc3 and bc4:

print("buy ", name, "\t")

margin_avialable = tsl.get_balance()

margin_required = cc['close']/4.8

if margin_avialable < margin_required:

print(f"Less margin, not taking order : margin_avialable is {margin_avialable} and margin_required is {margin_required} for {name}")

continue

orderbook[name]['name'] = name

orderbook[name]['date'] = str(current_time.date())

orderbook[name]['entry_time'] = str(current_time.time())[:8]

orderbook[name]['buy_sell'] = "BUY"

orderbook[name]['qty'] = 1 #int(10000/close)

try:

entry_orderid = tsl.order_placement(tradingsymbol=name ,exchange='NSE', quantity=orderbook[name]['qty'], price=0, trigger_price=0, order_type='MARKET', transaction_type='BUY', trade_type='MIS')

orderbook[name]['entry_orderid'] = entry_orderid

orderbook[name]['entry_price'] = tsl.get_executed_price(orderid=orderbook[name]['entry_orderid'])

orderbook[name]['tg'] = round(orderbook[name]['entry_price']*1.002, 1) # 1.01

orderbook[name]['sl'] = round(orderbook[name]['entry_price']*0.998, 1) # 0.99

sl_orderid = tsl.order_placement(tradingsymbol=name ,exchange='NSE', quantity=orderbook[name]['qty'], price=0, trigger_price=orderbook[name]['sl'], order_type='STOPMARKET', transaction_type='SELL', trade_type='MIS')

orderbook[name]['sl_orderid'] = sl_orderid

orderbook[name]['traded'] = "yes"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"Entry_done {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

except Exception as e:

print(e)

pdb.set_trace(header = "error in entry order cheking")

if orderbook[name]['traded'] == "yes":

bought = orderbook[name]['buy_sell'] == "BUY"

if bought:

try:

ltp = all_ltp[name]

sl_hit = tsl.get_order_status(orderid=orderbook[name]['sl_orderid']) =="TRADED"

tg_hit = ltp > orderbook[name]['tg']

except Exception as e:

print(e)

pdb.set_trace(header = "error in sl order cheking")

if sl_hit:

try:

orderbook[name]['exit_time'] = str(current_time.time())[:8]

orderbook[name]['exit_price'] = tsl.get_executed_price(orderid=orderbook[name]['sl_orderid'])

orderbook[name]['pnl'] = round((orderbook[name]['exit_price'] - orderbook[name]['entry_price'])*orderbook[name]['qty'],1)

orderbook[name]['remark'] = "Bought_SL_hit"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"SL_HIT {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

if reentry == "yes":

completed_orders.append(orderbook[name])

orderbook[name] = None

except Exception as e:

print(e)

pdb.set_trace(header = "sl_hit")

if tg_hit:

try:

tsl.cancel_order(OrderID=orderbook[name]['sl_orderid'])

time.sleep(2)

square_off_buy_order = tsl.order_placement(tradingsymbol=orderbook[name]['name'] ,exchange='NSE', quantity=orderbook[name]['qty'], price=0, trigger_price=0, order_type='MARKET', transaction_type='SELL', trade_type='MIS')

orderbook[name]['exit_time'] = str(current_time.time())[:8]

orderbook[name]['exit_price'] = tsl.get_executed_price(orderid=square_off_buy_order)

orderbook[name]['pnl'] = round((orderbook[name]['exit_price'] - orderbook[name]['entry_price'])*orderbook[name]['qty'],1)

orderbook[name]['remark'] = "Bought_TG_hit"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"TG_HIT {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

if reentry == "yes":

completed_orders.append(orderbook[name])

orderbook[name] = None

winsound.Beep(1500, 10000)

except Exception as e:

print(e)

pdb.set_trace(header = "error in sl tg_hit")