Thanks @Tradehull_Imran, After fixing the code as suggested, I am able to fetch LTP

1 Like

DEAR SIR

as per your guideline i downloaded the new tradehull as u given,

i rum my code ,but it showing the error ,

BANKNIFTY 27 NOV 50400 CALL BANKNIFTY 27 NOV 50400 PUT 50400

Exception at calling ltp as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: None, ‘error_type’: None, ‘error_message’: None}, ‘data’: {‘data’: {‘805’: ‘Too many requests. Further requests may result in the user being blocked.’}, ‘status’: ‘failed’}}

LTP data fetch failed, retrying…

Exception at calling ltp as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: None, ‘error_type’: None, ‘error_message’: None}, ‘data’: {‘data’: {‘805’: ‘Too many requests. Further requests may result in the user being blocked.’}, ‘status’: ‘failed’}}

LTP data fetch failed, retrying…

Exception at calling ltp as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: None, ‘error_type’: None, ‘error_message’: None}, ‘data’: {‘data’: {‘805’: ‘Too many requests. Further requests may result in the user being blocked.’}, ‘status’: ‘failed’}}

LTP data fetch failed, retrying…

Exception at calling ltp as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: None, ‘error_type’: None, ‘error_message’: None}, ‘data’: {‘data’: {‘805’: ‘Too many requests. Further requests may result in the user being blocked.’}, ‘status’: ‘failed’}}

LTP data fetch failed, retrying…

LTP CALL: 462.9

LTP PUT: 416.8

EMA CALL: 475

EMA PUT: 410

Placing PUT order with limit price

here is my code if any improvement ,please correct it

import pdb

import time

import datetime

import traceback

import talib

from Dhan_Tradehull_V2 import Tradehull

import pandas as pd

Initialize client details

client_code = “1103655452”

token_id = “eyJ0eXAiOiJKV1QiLCJhbGciOiJIUzUxMiJ9.eyJpc3MiOiJkaGFuIiwicGFydG5lcklkIjoiIiwiZXhwIjoxNzMyNTM3OTQxLCJ0b2tlbkNvbnN1bWVyVHlwZSI6IlNFTEYiLCJ3ZWJob29rVXJsIjoiIiwiZGhhbkNsaWVudElkIjoiMTEwMzY1NTQ1MiJ9.fr_y6xjBJ8e6_Ey4xSFb8vbVfS8Bg3DOu2GQJ7NuEpiV0aKYAvKj7Bt8FxylYI4dYMUp1wBgTXe3MlsB3NKvkQ” # Replace with your actual token

tsl = Tradehull(client_code, token_id) # tradehull_support_library

Fetch balance and calculate risk limit

available_balance = tsl.get_balance()

max_risk_for_the_day = (available_balance * 1) / 100 * -1

print(“Available balance:”, available_balance)

print(“Max risk for the day:”, max_risk_for_the_day)

Select ATM Strike Price options for NIFTY

ce_name, pe_name, strike = tsl.ATM_Strike_Selection(‘BANKNIFTY’, ‘27-11-2024’)

print(ce_name, pe_name, strike)

Initialize variables

traded_watchlist =

target_profit = 50 # Set your desired profit target

trailing_sl = 10 # Set your trailing stop-loss

Define the function for updating stop-loss

def update_stop_loss(current_price, last_sl):

“”"

Update stop loss dynamically based on the trailing stop-loss value.

“”"

new_sl = max(last_sl, current_price - trailing_sl)

return new_sl

def calculate_limit_price(symbol, ltp, order_type):

“”"

Calculate the limit price based on the order type and current price (ltp).

For a CALL, set a limit slightly below the LTP. For a PUT, slightly above.

“”"

price_offset = 0.01 # 1% offset for limit price

if order_type == ‘buy_call’:

return ltp * (1 - price_offset) # 1% below LTP for CALL option

Main trading loop

try:

while True:

# Restrict trading hours to 9:16 AM to 2:55 PM

if not (datetime.time(9, 16) <= datetime.datetime.now().time() <= datetime.time(22, 55)):

time.sleep(60) # Sleep for 1 minute before checking again

continue

# Fetch LTP for CALL and PUT options

ltp1 = tsl.get_ltp_data(ce_name)

ltp2 = tsl.get_ltp_data(pe_name)

# Check if data is valid before proceeding

if not ltp1 or not ltp2:

print("LTP data fetch failed, retrying...")

time.sleep(5)

continue # Skip to the next iteration if data is invalid

ltp1_value = list(ltp1.values())[0] if ltp1 else None

ltp2_value = list(ltp2.values())[0] if ltp2 else None

if ltp1_value is None or ltp2_value is None:

print("Received empty LTP data, retrying...")

time.sleep(5)

continue # Skip if no valid LTP values are found

# Fetch intraday data and calculate EMA for CALL and PUT options

chart1 = tsl.get_historical_data(tradingsymbol= ce_name, exchange='NFO', timeframe="1")

chart2 = tsl.get_historical_data(tradingsymbol= pe_name, exchange='NFO', timeframe="1")

chart1['ema'] = talib.EMA(chart1['close'], timeperiod=20)

chart2['ema'] = talib.EMA(chart2['close'], timeperiod=20)

# Get the last EMA values

last_candle1 = chart1['ema'].iloc[-1]

last_candle2 = chart2['ema'].iloc[-1]

# Convert to integers if necessary

last_candle_close1 = int(last_candle1 + 1)

last_candle_close2 = int(last_candle2 + 1)

print("LTP CALL:", ltp1_value)

print("LTP PUT:", ltp2_value)

print("EMA CALL:", last_candle_close1)

print("EMA PUT:", last_candle_close2)

# Check if CALL order condition is met and hasn't been placed yet

if last_candle_close1 <= ltp1_value and ce_name not in traded_watchlist:

print("Placing CALL order with limit price")

limit_price_call = calculate_limit_price(ce_name, ltp1_value, 'buy_call')

#entry_order_id1 = tsl.order_placement(ce_name, 'NFO', 25, limit_price_call, 0, 'LIMIT', 'BUY', 'MIS')

traded_watchlist.append(ce_name)

# Define initial target and stop-loss for CALL

stop_loss_call = ltp1_value - trailing_sl

last_sl_call = stop_loss_call # Set last_sl as initial stop-loss for CALL

target_call = ltp1_value + target_profit

order_active_call = True

# Monitor the CALL position

while order_active_call:

current_price_call = tsl.get_ltp_data(ce_name)

current_price_call_1 = list(current_price_call.values())[0]

last_sl_call = update_stop_loss(current_price_call_1, last_sl_call)

if current_price_call_1 <= last_sl_call:

print("Trailing stop-loss hit for CALL, exiting position")

#tsl.order_placement(ce_name, 'NFO', 25, limit_price_call, 0, 'LIMIT', 'SELL', 'MIS')

order_active_call = False

elif current_price_call_1 >= target_call:

print("Target hit for CALL, exiting position")

#tsl.order_placement(ce_name, 'NFO', 25, limit_price_call, 0, 'LIMIT', 'SELL', 'MIS')

order_active_call = False

# After exiting the trade, only remove from watchlist if EMA is above LTP

if not order_active_call:

# Recalculate the EMA for the next iteration check

chart1 = tsl.get_historical_data(tradingsymbol= ce_name, exchange='NFO', timeframe="1")

chart1['ema'] = talib.EMA(chart1['close'], timeperiod=20)

last_candle_close1 = int(chart1['ema'].iloc[-1] + 1)

ltp3 = tsl.get_ltp_data(ce_name)

ltp3_value = list(ltp3.values())[0]

# Check if EMA is now above LTP before allowing re-entry

if last_candle_close1 > ltp3_value:

traded_watchlist.remove(ce_name)

print(f"{ce_name} removed from watchlist; EMA is now above LTP.")

time.sleep(5)

# Repeat similar logic for PUT options

if last_candle_close2 <= ltp2_value and pe_name not in traded_watchlist:

print("Placing PUT order with limit price")

limit_price_put = calculate_limit_price(pe_name, ltp2_value, 'buy_put')

#entry_order_id2 = tsl.order_placement(pe_name, 'NFO', 25, limit_price_put, 0, 'LIMIT', 'BUY', 'MIS')

traded_watchlist.append(pe_name)

# Define initial target and stop-loss for PUT

stop_loss_put = ltp2_value - trailing_sl

last_sl_put = stop_loss_put # Set last_sl as initial stop-loss for PUT

target_put = ltp2_value + target_profit

order_active_put = True

# Monitor the PUT position

while order_active_put:

current_price_put = tsl.get_ltp_data(pe_name)

current_price_put_1 = list(current_price_put.values())[0]

last_sl_put = update_stop_loss(current_price_put_1, last_sl_put)

if current_price_put_1 <= last_sl_put:

print("Trailing stop-loss hit for PUT, exiting position")

#tsl.order_placement(pe_name, 'NFO', 25, limit_price_put, 0, 'LIMIT', 'SELL', 'MIS')

order_active_put = False

elif current_price_put_1 >= target_put:

print("Target hit for PUT, exiting position")

#tsl.order_placement(pe_name, 'NFO', 25, limit_price_put, 0, 'LIMIT', 'SELL', 'MIS')

order_active_put = False

# After exiting the trade, only remove from watchlist if EMA is above LTP

if not order_active_put:

chart2 = tsl.get_historical_data(tradingsymbol= pe_name, exchange='NFO', timeframe="1")

chart2['ema'] = talib.EMA(chart2['close'], timeperiod=20)

last_candle_close2 = int(chart2['ema'].iloc[-1] + 1)

ltp4 = tsl.get_ltp_data(pe_name)

ltp4_value = list(ltp4.values())[0]

# Check if EMA is now above LTP before allowing re-entry

if last_candle_close2 > ltp4_value:

traded_watchlist.remove(pe_name)

print(f"{pe_name} removed from watchlist; EMA is now above LTP.")

time.sleep(1)

# Wait before the next iteration

time.sleep(5)

except Exception as e:

print(“An error occurred:”, e)

print(traceback.format_exc())

pdb.set_trace()

Please help.

Hello @Tradehull_Imran sir,

Sorry very delay practice

last time it was working fine for

Dhan_Tradehull_V2 Algo || Learn Algo Trading

but I when I am trying with below files

I am getting

Hope already answer is somewhere here. I will try to find it out from my side also.

1 Like

@Tradehull_Imran sir

I think for this also I need to replace the Dhan_Tradehull_V2.py file as per below solution right ?

Hi @Tradehull_Imran,

Day before yesterday it was working fine.

When i was running today getting below error.

VWAP CODE:

index_chart = tsl.get_historical_data(tradingsymbol='BANKNIFTY 27 NOV 50400 PUT', exchange='NFO', timeframe="1")

print(index_chart)

index_chart.set_index(pd.DatetimeIndex(index_chart['timestamp']), inplace=True)

index_chart['vwap'] = pta.vwap(index_chart['high'], index_chart['low'], index_chart['close'], index_chart['volume'])

Copied latest Dhan_Tradehull_V2.py

Error:

Traceback (most recent call last):

File "C:/Dhan/8. Session8- 2nd Live Algo/8. Session 8 Dhan_Tradehull_V2/vwap strategy.py", line 43, in <module>

index_chart.set_index(pd.DatetimeIndex(index_chart['timestamp']), inplace=True)

AttributeError: 'NoneType' object has no attribute 'set_index'

None

C:\Dhan\8. Session8- 2nd Live Algo>pip show dhanhq

Name: dhanhq

Version: 2.0.0

Summary: The official Python client for communicating with the DhanHQ API

Home-page: https://dhanhq.co/

Author: Dhan

Author-email: dhan-oss@dhan.co

License: MIT LICENSE

Location: c:\python3.8\lib\site-packages

Requires: pandas, pyOpenSSL, requests, websockets

I am trying today

But still it shows error

So How and when I will get the data and error will remove

And How Does it works

C:\Algo Practice\Api Upgrade>py RSI.py

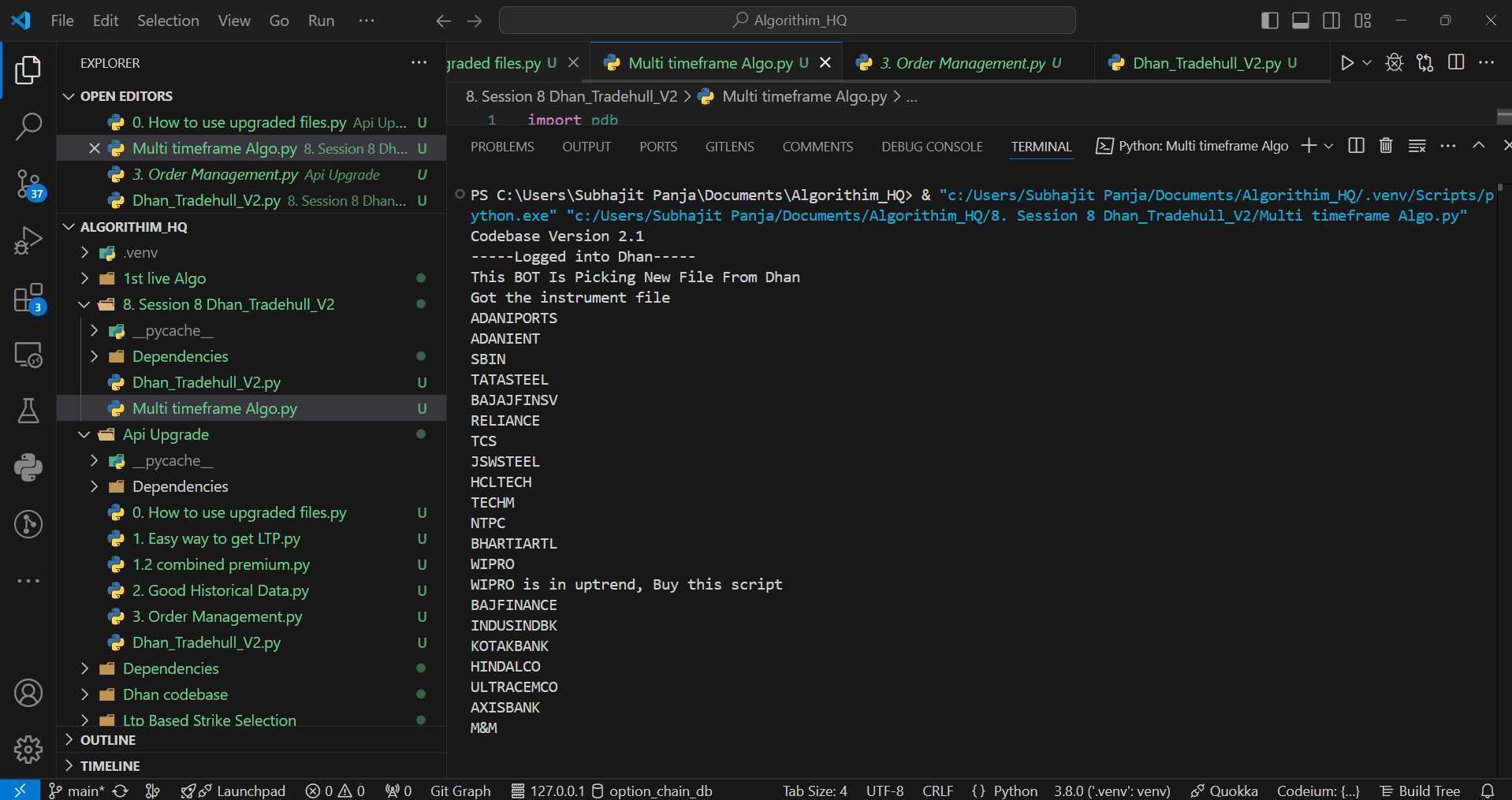

Codebase Version 2.1

-----Logged into Dhan-----

reading existing file all_instrument 2024-11-21.csv

Got the instrument file

available_balance 129364.75

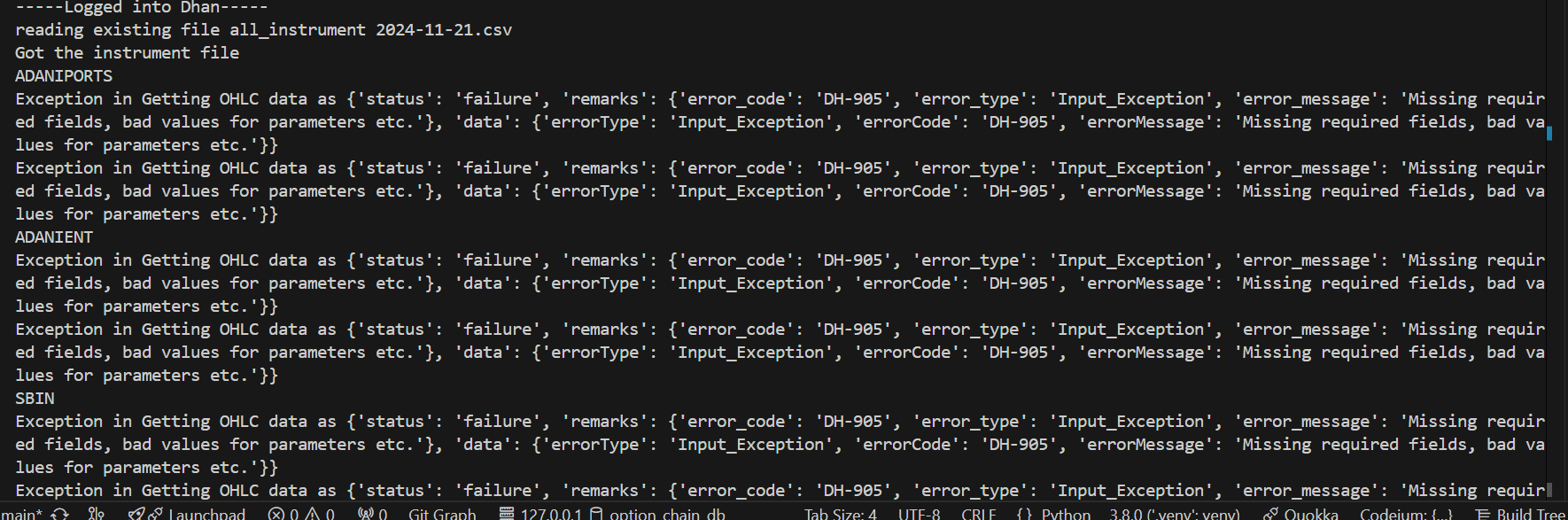

Exception in Getting OHLC data as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: ‘DH-905’, ‘error_type’: ‘Input_Exception’, ‘error_message’: ‘Missing required fields, bad values for parameters etc.’}, ‘data’: {‘errorType’: ‘Input_Exception’, ‘errorCode’: ‘DH-905’, ‘errorMessage’: ‘Missing required fields, bad values for parameters etc.’}}

Exception in Getting OHLC data as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: ‘DH-905’, ‘error_type’: ‘Input_Exception’, ‘error_message’: ‘Missing required fields, bad values for parameters etc.’}, ‘data’: {‘errorType’: ‘Input_Exception’, ‘errorCode’: ‘DH-905’, ‘errorMessage’: ‘Missing required fields, bad values for parameters etc.’}}

Traceback (most recent call last):

File “RSI.py”, line 46, in

chart_15[‘rsi’] = talib.RSI(chart_15[‘close’], timeperiod=14) #pandas

TypeError: ‘NoneType’ object is not subscriptable

The issue is of rate limit

Too many requests. Further requests may result in the user being blocked.

for solution check : https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718/860?u=tradehull_imran

Hi @Aijaz_Ahmad

This is related to order cancellation

I will check your question in live market tomorrow

Hye Sir @Tradehull_Imran

Suppose I enter a trade when the condition is met, e.g., Close > EMA, and my take profit is set to 10 points.

After booking the profit, the code enters a new trade again because the condition is still true.

However, I don’t want it to re-enter immediately. I want to trade only when the next signal comes. Please help

Hi @Deodas_kumar

Also modify your code to use less calls

New code

while True:

time.sleep(2)

try:

ltp_ce_pe = tsl.get_ltp_data([ce_name, pe_name])

ltp1 = ltp_ce_pe[ce_name]

ltp2 = ltp_ce_pe[pe_name]

except Exception as e:

print("Received empty LTP data, retrying...", e)

continue

New code is a replacement for

while True:

# Fetch LTP for CALL and PUT options

ltp1 = tsl.get_ltp_data(ce_name)

ltp2 = tsl.get_ltp_data(pe_name)

# Check if data is valid before proceeding

if not ltp1 or not ltp2:

print("LTP data fetch failed, retrying...")

time.sleep(5)

continue # Skip to the next iteration if data is invalid

ltp1_value = list(ltp1.values())[0] if ltp1 else None

ltp2_value = list(ltp2.values())[0] if ltp2 else None

if ltp1_value is None or ltp2_value is None:

print("Received empty LTP data, retrying...")

time.sleep(5)

continue # Skip if no valid LTP values are found

Hi @Kalpeshh_Patel

see : https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718/942?u=tradehull_imran

Hi @Subhajitpanja

yes its correct

use : https://drive.google.com/file/d/1h8J6VOLrHMAaF1NGP4_vJj2wtkNxfPDw/view

1 Like

Error says it cannot get data for index_chart, so its not able to plot vwap

use this file : https://drive.google.com/file/d/1h8J6VOLrHMAaF1NGP4_vJj2wtkNxfPDw/view

Hi @Zee2Zahid

How to manage re-entry and trade details, This concept I have not covered till now. will add the same in upcoming videos.

As per chart

If my one strategy requires following parameters

tsl = Tradehull(client_code,token_id)

chart_1 = tsl.get_historical_data(tradingsymbol = stock_name,exchange = ‘NSE’,timeframe=“5”)

chart_1[‘rsi’] = talib.RSI(chart_1[‘close’], timeperiod=14) #pandas

chart_15 = tsl.get_intraday_data(stock_name, ‘NSE’, 15) # 15 minute chart

chart_15 = tsl.get_historical_data(tradingsymbol = stock_name,exchange = ‘NSE’,timeframe=“15”) # this call has been updated to get_historical_data call,

buy_entry_orderid = tsl.order_placement(stock_name,‘NSE’, 1, 0, 0, ‘MARKET’, ‘BUY’, ‘MIS’)

live_pnl = tsl.get_live_pnl()

I_want_to_trade_no_more = tsl.kill_switch(‘ON’)

order_details = tsl.cancel_all_orders()

sl_orderid = tsl.order_placement(stock_name,‘NSE’, 1, 0, sl_price, ‘STOPMARKET’, ‘SELL’, ‘MIS’)

As per above parameter which I demand

Means I requested 10 DATA API

Is that right???

Yes it is correct

note:

chart_1[‘rsi’] = talib.RSI(chart_1[‘close’], timeperiod=14) …

is not a api call… its just a calculation.

Understand

But what 10 stocks in watchlist and one parameter of given as follows

watchlist = [‘MOTHERSON’, ‘OFSS’, ‘MANAPPURAM’, ‘BSOFT’, ‘CHAMBLFERT’, ‘DIXON’, ‘NATIONALUM’, ‘DLF’, ‘IDEA’, ‘ADANIPORTS’]

chart_15 = tsl.get_historical_data(tradingsymbol = stock_name,exchange = ‘NSE’,timeframe=“15”)

It means 10 DATA API requested

Is it right?

wanted to share this…

found accurate Nifty expiries for last 3 years,

Actually this is a difficult data to get because expiry dates may be influenced by NSE holidays.

07-Jan-2021, 14-Jan-2021, 21-Jan-2021, 28-Jan-2021, 04-Feb-2021, 11-Feb-2021, 18-Feb-2021, 25-Feb-2021, 04-Mar-2021, 10-Mar-2021, 18-Mar-2021, 25-Mar-2021, 01-Apr-2021, 08-Apr-2021, 15-Apr-2021, 22-Apr-2021, 29-Apr-2021, 06-May-2021, 12-May-2021, 20-May-2021, 27-May-2021, 03-Jun-2021, 10-Jun-2021, 17-Jun-2021, 24-Jun-2021, 01-Jul-2021, 08-Jul-2021, 15-Jul-2021, 22-Jul-2021, 29-Jul-2021, 05-Aug-2021, 12-Aug-2021, 18-Aug-2021, 26-Aug-2021, 02-Sep-2021, 09-Sep-2021, 16-Sep-2021, 23-Sep-2021, 30-Sep-2021, 07-Oct-2021, 14-Oct-2021, 21-Oct-2021, 28-Oct-2021, 03-Nov-2021, 11-Nov-2021, 18-Nov-2021, 25-Nov-2021, 02-Dec-2021, 09-Dec-2021, 16-Dec-2021, 23-Dec-2021, 30-Dec-2021, 06-Jan-2022, 13-Jan-2022, 20-Jan-2022, 27-Jan-2022, 03-Feb-2022, 10-Feb-2022, 17-Feb-2022, 24-Feb-2022, 03-Mar-2022, 10-Mar-2022, 17-Mar-2022, 24-Mar-2022, 31-Mar-2022, 07-Apr-2022, 13-Apr-2022, 21-Apr-2022, 28-Apr-2022, 05-May-2022, 12-May-2022, 19-May-2022, 26-May-2022, 02-Jun-2022, 09-Jun-2022, 16-Jun-2022, 23-Jun-2022, 30-Jun-2022, 07-Jul-2022, 14-Jul-2022, 21-Jul-2022, 28-Jul-2022, 04-Aug-2022, 11-Aug-2022, 18-Aug-2022, 25-Aug-2022, 01-Sep-2022, 08-Sep-2022, 15-Sep-2022, 22-Sep-2022, 29-Sep-2022, 06-Oct-2022, 13-Oct-2022, 20-Oct-2022, 27-Oct-2022, 03-Nov-2022, 10-Nov-2022, 17-Nov-2022, 24-Nov-2022, 01-Dec-2022, 08-Dec-2022, 15-Dec-2022, 22-Dec-2022, 29-Dec-2022, 05-Jan-2023, 12-Jan-2023, 19-Jan-2023, 25-Jan-2023, 02-Feb-2023, 09-Feb-2023, 16-Feb-2023, 23-Feb-2023, 02-Mar-2023, 09-Mar-2023, 16-Mar-2023, 23-Mar-2023, 29-Mar-2023, 06-Apr-2023, 13-Apr-2023, 20-Apr-2023, 27-Apr-2023, 04-May-2023, 11-May-2023, 18-May-2023, 25-May-2023, 01-Jun-2023, 08-Jun-2023, 15-Jun-2023, 22-Jun-2023, 28-Jun-2023, 29-Jun-2023, 06-Jul-2023, 13-Jul-2023, 20-Jul-2023, 27-Jul-2023, 03-Aug-2023, 10-Aug-2023, 17-Aug-2023, 24-Aug-2023, 31-Aug-2023, 07-Sep-2023, 14-Sep-2023, 21-Sep-2023, 28-Sep-2023, 05-Oct-2023, 12-Oct-2023, 19-Oct-2023, 26-Oct-2023, 02-Nov-2023, 09-Nov-2023, 16-Nov-2023, 23-Nov-2023, 30-Nov-2023, 07-Dec-2023, 14-Dec-2023, 21-Dec-2023, 28-Dec-2023, 04-Jan-2024, 11-Jan-2024, 18-Jan-2024, 25-Jan-2024, 01-Feb-2024, 08-Feb-2024, 15-Feb-2024, 22-Feb-2024, 29-Feb-2024, 07-Mar-2024, 14-Mar-2024, 21-Mar-2024, 28-Mar-2024, 04-Apr-2024, 10-Apr-2024, 18-Apr-2024, 25-Apr-2024, 02-May-2024, 09-May-2024, 16-May-2024, 23-May-2024, 30-May-2024, 06-Jun-2024, 13-Jun-2024, 20-Jun-2024, 27-Jun-2024, 04-Jul-2024, 11-Jul-2024, 18-Jul-2024, 25-Jul-2024, 01-Aug-2024, 08-Aug-2024, 14-Aug-2024, 22-Aug-2024, 29-Aug-2024, 05-Sep-2024, 12-Sep-2024, 19-Sep-2024, 26-Sep-2024, 03-Oct-2024, 10-Oct-2024, 17-Oct-2024, 24-Oct-2024, 31-Oct-2024, 07-Nov-2024, 14-Nov-2024, 21-Nov-2024, 28-Nov-2024, 05-Dec-2024, 12-Dec-2024, 19-Dec-2024, 26-Dec-2024,

1 Like

@Tradehull_Imran sir it’s working

1 Like