Hi @Tradehull_Imran,

I’m trying to implement the 2 candle strategy as per your video. However, I keep running into couple of errors. This is inspite of adhering to the rate limit and calling get_ltp with a gap of 60 secs between two calls.

Error list…

- Exception at calling ltp as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: None, ‘error_type’: None, ‘error_message’: None}, ‘data’: {‘data’: {‘805’: ‘Too many requests. Further requests may result in the user being blocked.’}, ‘status’: ‘failed’}}

exception got in ce_pe_option_df ‘NIFTY’

- UnboundLocalError: cannot access local variable ‘strike’ where it is not associated with a value

- Message: 'Got exception in ce_pe_option_df ’

Arguments: (KeyError(‘NIFTY’),)

I’m pasting the detailed code file and error file below. Kindly help

Code file

import pdb

import time

import datetime

import traceback

import pandas as pd

from pprint import pprint

import talib

# import pandas_ta as pta

import pandas_ta as ta

import warnings,sys

warnings.filterwarnings("ignore")

path = r'C:/Users/krish/OneDrive/Documents/Krishna/2 Areas/Finance/Stock Market/Trading/Trading Courses/Development/AlgoTrading/Dhan/DhanAlgoTrading'

# path = r'../DhanAlgoTrading'

sys.path.insert(0, path)

import credentials as cred

from Dhan_Tradehull_V2 import Tradehull

# ---------------Basic setup for dhan login & Defining Constants------------------------

client_code = cred.CLIENT_ID

token_id = cred.ACCESS_TOKEN

tsl = Tradehull(client_code,token_id)

available_balance = tsl.get_balance()

# leveraged_margin = available_balance*5

max_trades = 5

per_trade_margin = (available_balance/max_trades/5)

max_loss = -available_balance/100

EXPIRY ='26-12-2024'

LOT_SIZE = 3

VOLUME = 10000

# ---------------------------------------------------------------------------------------

traded = "no"

trade_info = {"options_name":None, "qty":None, "sl":None, "CE_PE":None}

while True:

live_pnl = tsl.get_live_pnl()

current_time = datetime.datetime.now().time()

month = datetime.datetime.now().strftime("%b").upper()

if current_time < datetime.time(9, 30):

print("Market yet to open", current_time)

continue

if (current_time > datetime.time(15, 15)) or (live_pnl < max_loss):

order_details = tsl.cancel_all_orders()

print("Market is closed!", current_time)

break

index_chart = tsl.get_historical_data(tradingsymbol=f'NIFTY {month} FUT', exchange='NFO', timeframe="1")

time.sleep(60)

index_ltp = tsl.get_ltp_data(names = [f'NIFTY {month} FUT'])[f'NIFTY {month} FUT']

# if (index_chart.empty):

# time.sleep(60)

# continue

if index_chart is None or index_ltp is None:

print("Data unavailable. Retrying...")

time.sleep(60)

continue

# rsi ------------------------ apply indicators

index_chart['rsi'] = talib.RSI(index_chart['close'], timeperiod=14)

# vwap

index_chart.set_index(pd.DatetimeIndex(index_chart['timestamp']), inplace=True)

index_chart['vwap'] = ta.vwap(index_chart['high'] , index_chart['low'], index_chart['close'] , index_chart['volume'])

# Supertrend

supertrend = ta.supertrend(index_chart['high'], index_chart['low'], index_chart['close'], 10, 2)

index_chart = pd.concat([index_chart, supertrend], axis=1, join='inner')

# vwma

index_chart['pv'] = index_chart['close'] * index_chart['volume']

index_chart['vwma'] = index_chart['pv'].rolling(20).mean() / index_chart['volume'].rolling(20).mean()

first_candle = index_chart.iloc[-3]

second_candle = index_chart.iloc[-2]

running_candle = index_chart.iloc[-1]

# print(index_chart)

# ---------------------------- BUY ENTRY CONDITIONS ----------------------------

buy_condition_1 = first_candle['close'] > first_candle['vwap'] # First Candle close is above VWAP

buy_condition_2 = first_candle['close'] > first_candle['SUPERT_10_2.0'] # First Candle close is above Supertrend

buy_condition_3 = first_candle['close'] > first_candle['vwma'] # First Candle close is above VWMA

buy_condition_4 = first_candle['rsi'] < 80 # First candle RSI < 80

buy_condition_5 = second_candle['volume'] > VOLUME # Second candle Volume should be greater than 50,000 for Nifty and above 125,000 for Bank Nifty

buy_condition_6 = traded == "no"

buy_condition_7 = index_ltp > first_candle['low']

print(f"BUY \t {current_time} \t {buy_condition_1} \t {buy_condition_2} \t {buy_condition_3} \t {buy_condition_4} \t {buy_condition_5} \t {buy_condition_6} \t {buy_condition_7} \t first_candle {str(first_candle['timestamp'].time())}")

# ---------------------------- SELL ENTRY CONDITIONS ----------------------------

sell_condition_1 = first_candle['close'] < first_candle['vwap'] # First Candle close is below VWAP

sell_condition_2 = first_candle['close'] < first_candle['SUPERT_10_2.0'] # First Candle close is below Supertrend

sell_condition_3 = first_candle['close'] < first_candle['vwma'] # First Candle close is below VWMA

sell_condition_4 = first_candle['rsi'] > 20 # First candle RSI < 80

sell_condition_5 = second_candle['volume'] > VOLUME # Second candle Volume should be greater than 50,000 for Nifty and above 125,000 for Bank Nifty

sell_condition_6 = traded == "no"

sell_condition_7 = index_ltp < first_candle['high']

print(f"SELL \t {current_time} \t {sell_condition_1} \t {sell_condition_2} \t {sell_condition_3} \t {sell_condition_4} \t {sell_condition_5} \t {buy_condition_7} \t {sell_condition_7} \t first_candle {str(first_candle['timestamp'].time())} \n")

# pdb.set_trace()

if buy_condition_1 and buy_condition_2 and buy_condition_3 and buy_condition_4 and buy_condition_5 and buy_condition_6 and buy_condition_7:

print("Buy Signal Formed")

ce_name, pe_name, strike = tsl.ATM_Strike_Selection(Underlying ='NIFTY',Expiry =EXPIRY)

total_lots = tsl.get_lot_size(ce_name)*LOT_SIZE

# call_buy_orderid = tsl.order_placement(ce_name,'NFO', total_lots, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info['options_name'] = ce_name

trade_info['qty'] = total_lots

trade_info['buy_price'] = tsl.get_ltp_data(names = [ce_name])[ce_name] #call_buy_orderid['price']

trade_info['create_time'] = datetime.datetime.now()

trade_info['sl'] = first_candle['low']

trade_info['CE_PE'] = "CE"

if sell_condition_1 and sell_condition_2 and sell_condition_3 and sell_condition_4 and sell_condition_5 and sell_condition_6 and sell_condition_7:

print("Sell Signal Formed")

ce_name, pe_name, strike = tsl.ATM_Strike_Selection(Underlying ='NIFTY',Expiry =EXPIRY)

total_lots = tsl.get_lot_size(pe_name)*LOT_SIZE

# put_buy_orderid = tsl.order_placement(pe_name,'NFO', total_lots, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info['options_name'] = pe_name

trade_info['qty'] = total_lots

trade_info['buy_price'] = tsl.get_ltp_data(names = [pe_name])[pe_name]

trade_info['create_time'] = datetime.datetime.now()

trade_info['sl'] = first_candle['high']

trade_info['CE_PE'] = "PE"

# ---------------------------- check for exit SL/TG-----------------------------

if traded == "yes":

long_position = trade_info['CE_PE'] == "CE"

short_position = trade_info['CE_PE'] == "PE"

if long_position:

stop_loss_hit = index_ltp < trade_info['sl']

target_hit = index_ltp < running_candle['SUPERT_10_2.0']

if stop_loss_hit or target_hit:

# call_exit_orderid = tsl.order_placement(trade_info['options_name'],'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

if stop_loss_hit:

trade_info['exit_reason'] = 'SL Hit'

else:

trade_info['exit_reason'] = 'Target Hit'

trade_info['sell_price'] = tsl.get_ltp_data(names = [ce_name])[ce_name]

trade_info['exit_time'] = datetime.datetime.now()

print("Order Exited", trade_info)

traded = "no"

# pdb.set_trace()

if short_position:

stop_loss_hit = index_ltp > trade_info['sl']

target_hit = index_ltp > running_candle['SUPERT_10_2.0']

if stop_loss_hit or target_hit:

# put_exit_orderid = tsl.order_placement(trade_info['options_name'],'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

if stop_loss_hit:

trade_info['exit_reason'] = 'SL Hit'

else:

trade_info['exit_reason'] = 'Target Hit'

trade_info['sell_price'] = tsl.get_ltp_data(names = [pe_name])[pe_name]

trade_info['exit_time'] = datetime.datetime.now()

print("Order Exited", trade_info)

traded = "no"

# pdb.set_trace()

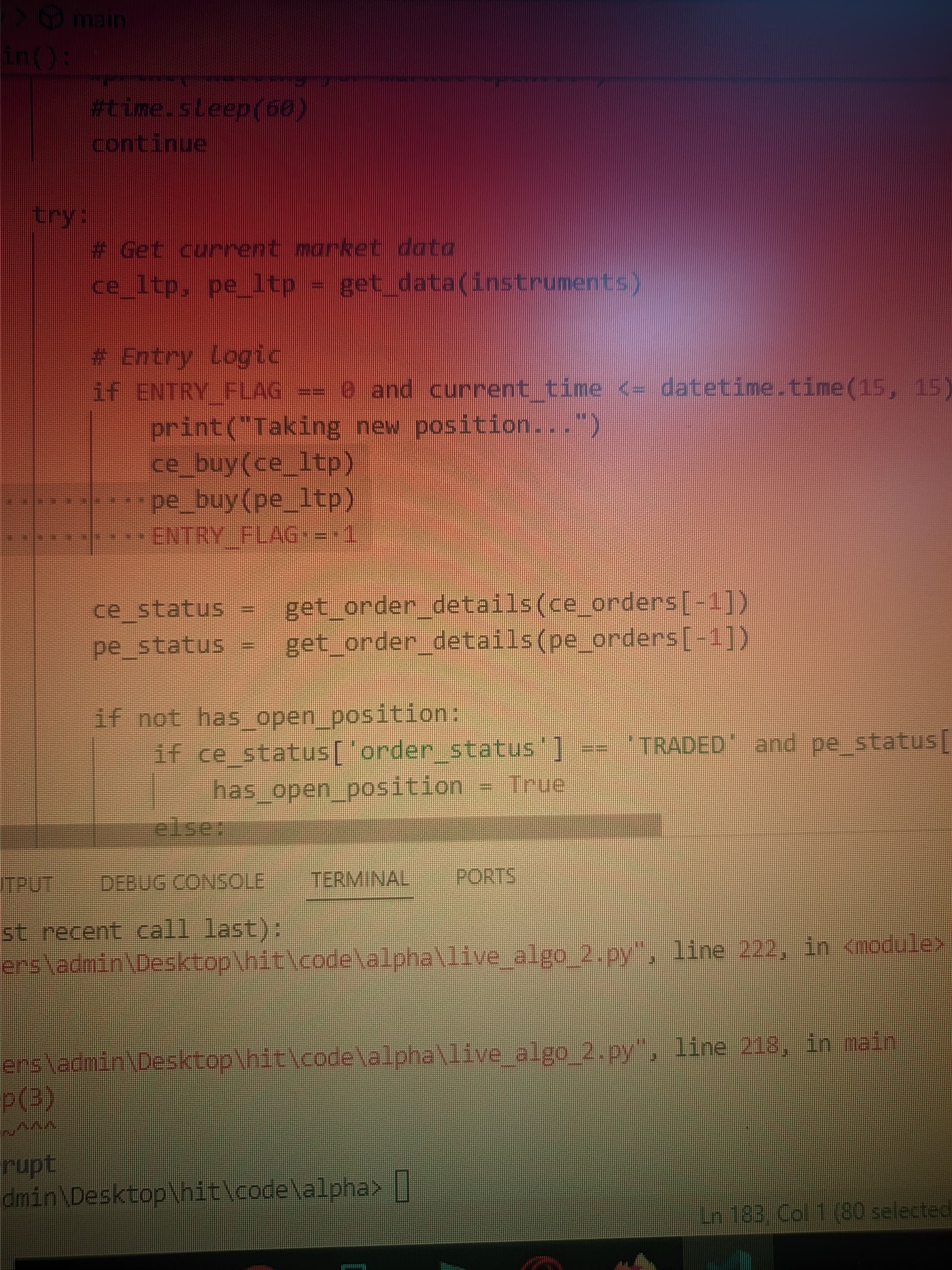

Error details

Sell Signal Formed

Exception at calling ltp as {'status': 'failure', 'remarks': {'error_code': None, 'error_type': None, 'error_message': None}, 'data': {'data': {'805': 'Too many requests. Further requests may result in the user being blocked.'}, 'status': 'failed'}}

exception got in ce_pe_option_df 'NIFTY'

Traceback (most recent call last):

File "C:\Users/krish/OneDrive/Documents/Krishna/2 Areas/Finance/Stock Market/Trading/Trading Courses/Development/AlgoTrading/Dhan/DhanAlgoTrading\Dhan_Tradehull_V2.py", line 489, in ATM_Strike_Selection

ltp = ltp_data[Underlying]

~~~~~~~~^^^^^^^^^^^^

KeyError: 'NIFTY'

--- Logging error ---

Traceback (most recent call last):

File "C:\Users/krish/OneDrive/Documents/Krishna/2 Areas/Finance/Stock Market/Trading/Trading Courses/Development/AlgoTrading/Dhan/DhanAlgoTrading\Dhan_Tradehull_V2.py", line 489, in ATM_Strike_Selection

ltp = ltp_data[Underlying]

~~~~~~~~^^^^^^^^^^^^

KeyError: 'NIFTY'

During handling of the above exception, another exception occurred:

Traceback (most recent call last):

File "c:\Users\krish\anaconda3\Lib\logging\__init__.py", line 1110, in emit

msg = self.format(record)

^^^^^^^^^^^^^^^^^^^

File "c:\Users\krish\anaconda3\Lib\logging\__init__.py", line 953, in format

return fmt.format(record)

^^^^^^^^^^^^^^^^^^

File "c:\Users\krish\anaconda3\Lib\logging\__init__.py", line 687, in format

record.message = record.getMessage()

^^^^^^^^^^^^^^^^^^^

File "c:\Users\krish\anaconda3\Lib\logging\__init__.py", line 377, in getMessage

msg = msg % self.args

~~~~^~~~~~~~~~~

TypeError: not all arguments converted during string formatting

Call stack:

File "<frozen runpy>", line 198, in _run_module_as_main

File "<frozen runpy>", line 88, in _run_code

File "c:\Users\krish\anaconda3\Lib\site-packages\ipykernel_launcher.py", line 17, in <module>

app.launch_new_instance()

File "c:\Users\krish\anaconda3\Lib\site-packages\traitlets\config\application.py", line 992, in launch_instance

app.start()

File "c:\Users\krish\anaconda3\Lib\site-packages\ipykernel\kernelapp.py", line 701, in start

self.io_loop.start()

File "c:\Users\krish\anaconda3\Lib\site-packages\tornado\platform\asyncio.py", line 195, in start

self.asyncio_loop.run_forever()

File "c:\Users\krish\anaconda3\Lib\asyncio\windows_events.py", line 321, in run_forever

super().run_forever()

File "c:\Users\krish\anaconda3\Lib\asyncio\base_events.py", line 607, in run_forever

self._run_once()

File "c:\Users\krish\anaconda3\Lib\asyncio\base_events.py", line 1922, in _run_once

handle._run()

File "c:\Users\krish\anaconda3\Lib\asyncio\events.py", line 80, in _run

self._context.run(self._callback, *self._args)

File "c:\Users\krish\anaconda3\Lib\site-packages\ipykernel\kernelbase.py", line 534, in dispatch_queue

await self.process_one()

File "c:\Users\krish\anaconda3\Lib\site-packages\ipykernel\kernelbase.py", line 523, in process_one

await dispatch(*args)

File "c:\Users\krish\anaconda3\Lib\site-packages\ipykernel\kernelbase.py", line 429, in dispatch_shell

await result

File "c:\Users\krish\anaconda3\Lib\site-packages\ipykernel\kernelbase.py", line 767, in execute_request

reply_content = await reply_content

File "c:\Users\krish\anaconda3\Lib\site-packages\ipykernel\ipkernel.py", line 429, in do_execute

res = shell.run_cell(

File "C:\Users\krish\AppData\Local\Temp\ipykernel_30488\1990712033.py", line 29, in wrapper

result = old_func(*args, **kwargs)

File "c:\Users\krish\anaconda3\Lib\site-packages\ipykernel\zmqshell.py", line 549, in run_cell

return super().run_cell(*args, **kwargs)

File "c:\Users\krish\anaconda3\Lib\site-packages\IPython\core\interactiveshell.py", line 3051, in run_cell

result = self._run_cell(

File "c:\Users\krish\anaconda3\Lib\site-packages\IPython\core\interactiveshell.py", line 3106, in _run_cell

result = runner(coro)

File "c:\Users\krish\anaconda3\Lib\site-packages\IPython\core\async_helpers.py", line 129, in _pseudo_sync_runner

coro.send(None)

File "c:\Users\krish\anaconda3\Lib\site-packages\IPython\core\interactiveshell.py", line 3311, in run_cell_async

has_raised = await self.run_ast_nodes(code_ast.body, cell_name,

File "c:\Users\krish\anaconda3\Lib\site-packages\IPython\core\interactiveshell.py", line 3493, in run_ast_nodes

if await self.run_code(code, result, async_=asy):

File "c:\Users\krish\anaconda3\Lib\site-packages\IPython\core\interactiveshell.py", line 3553, in run_code

exec(code_obj, self.user_global_ns, self.user_ns)

File "<ipython-input-1-fd9addb455cf>", line 125, in <module>

ce_name, pe_name, strike = tsl.ATM_Strike_Selection(Underlying ='NIFTY',Expiry =EXPIRY)

File "C:\Users/krish/OneDrive/Documents/Krishna/2 Areas/Finance/Stock Market/Trading/Trading Courses/Development/AlgoTrading/Dhan/DhanAlgoTrading\Dhan_Tradehull_V2.py", line 542, in ATM_Strike_Selection

self.logger.exception("Got exception in ce_pe_option_df ", e)

Message: 'Got exception in ce_pe_option_df '

Arguments: (KeyError('NIFTY'),)