Hello @Tradehull_Imran,

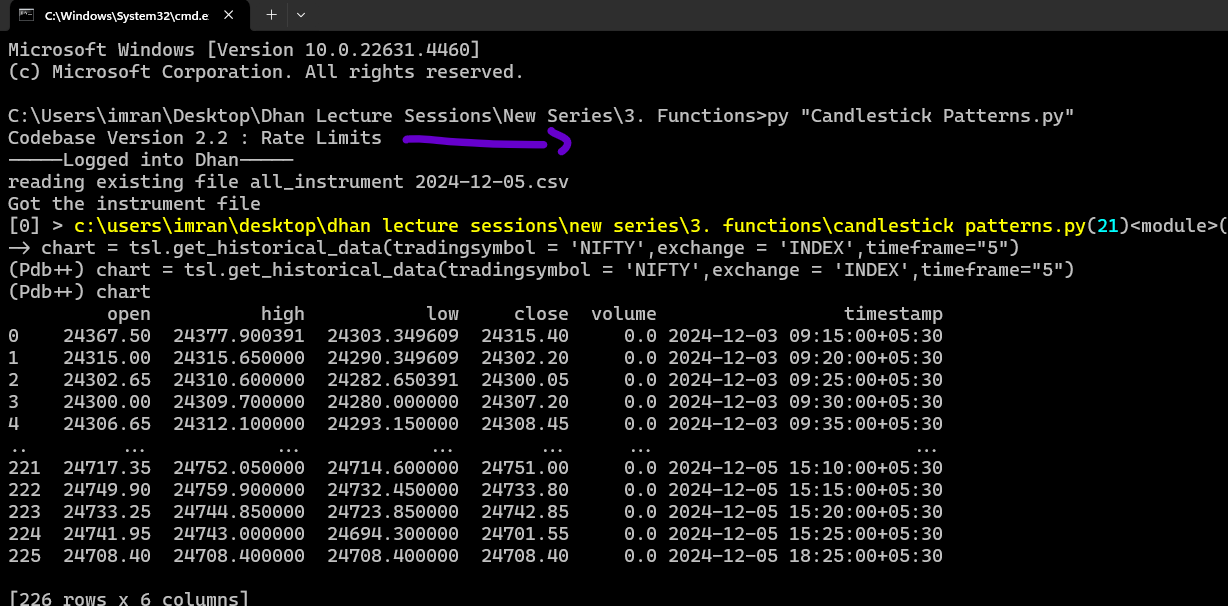

i have started session 3, and i am getting error as below cmd error code:

also the same is the issue with historical data call.

below is the error showing in cmd :

File "C:\Users\arpan\AppData\Local\Programs\Python\Python38\lib\site-packages\pandas\core\frame.py", line 817, in __init__

raise ValueError("DataFrame constructor not properly called!")

intraday_minute_data() missing 2 required positional arguments: 'from_date' and 'to_date'

Traceback (most recent call last):

File "C:\Users\arpan\Dhan Algo\Session 3\3. Session3 - Codebase\3. Session3 - Codebase\Dhan codebase\Dhan_Tradehull.py", line 252, in get_intraday_data

ohlc = self.Dhan.intraday_minute_data(str(security_id),exchangeSegment,instrument_type)

TypeError: intraday_minute_data() missing 2 required positional arguments: 'from_date' and 'to_date'

[0] > c:\users\arpan\dhan algo\session 3\3. session3 - codebase\3. session3 - codebase\dhan codebase\dhan_codebase usage.py(28)<module>()

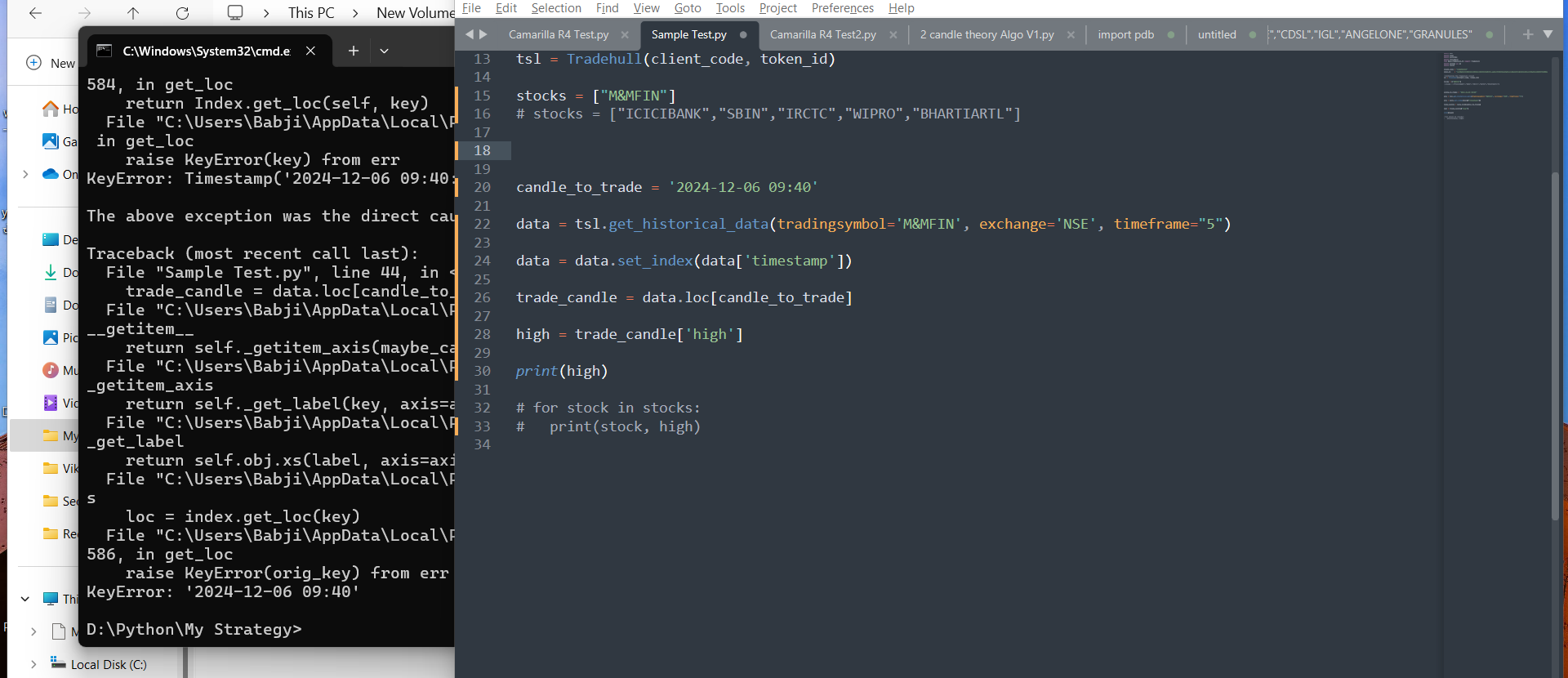

also sir, there is problem in loading dataframe.

df = pd.DataFrame(ohlc[‘data’]) is not loading. its showing error. please once run it on your pc as well sir and tell me where is the issue.

My 2 Algos where running from 9.20 to 1.30 Today, Usually I will run only one Algo from 9.20 and around 12.20 the Rate Limit Error Message , Will come..

But Toady after using 2 Algos , the message came around 1.30..

Hi @Kishore007

Then this file seems to be working fine

you can increase the sleep time

see

line 374, inside get_ltp_data function increase the time.sleep(2) to time.sleep(2.5)

line 274, inside get_historical_data function increase the time.sleep(1.5) to time.sleep(2.5)

Me too Me too

So far, we have learned Algo Trading, that we can implement and do forward testing, but we can wipe out our capital in that process. So, learning to backtest is key to success. Totally Agree with you @Tradehull_Imran “ Heart of Algo Trading : Backtesting”