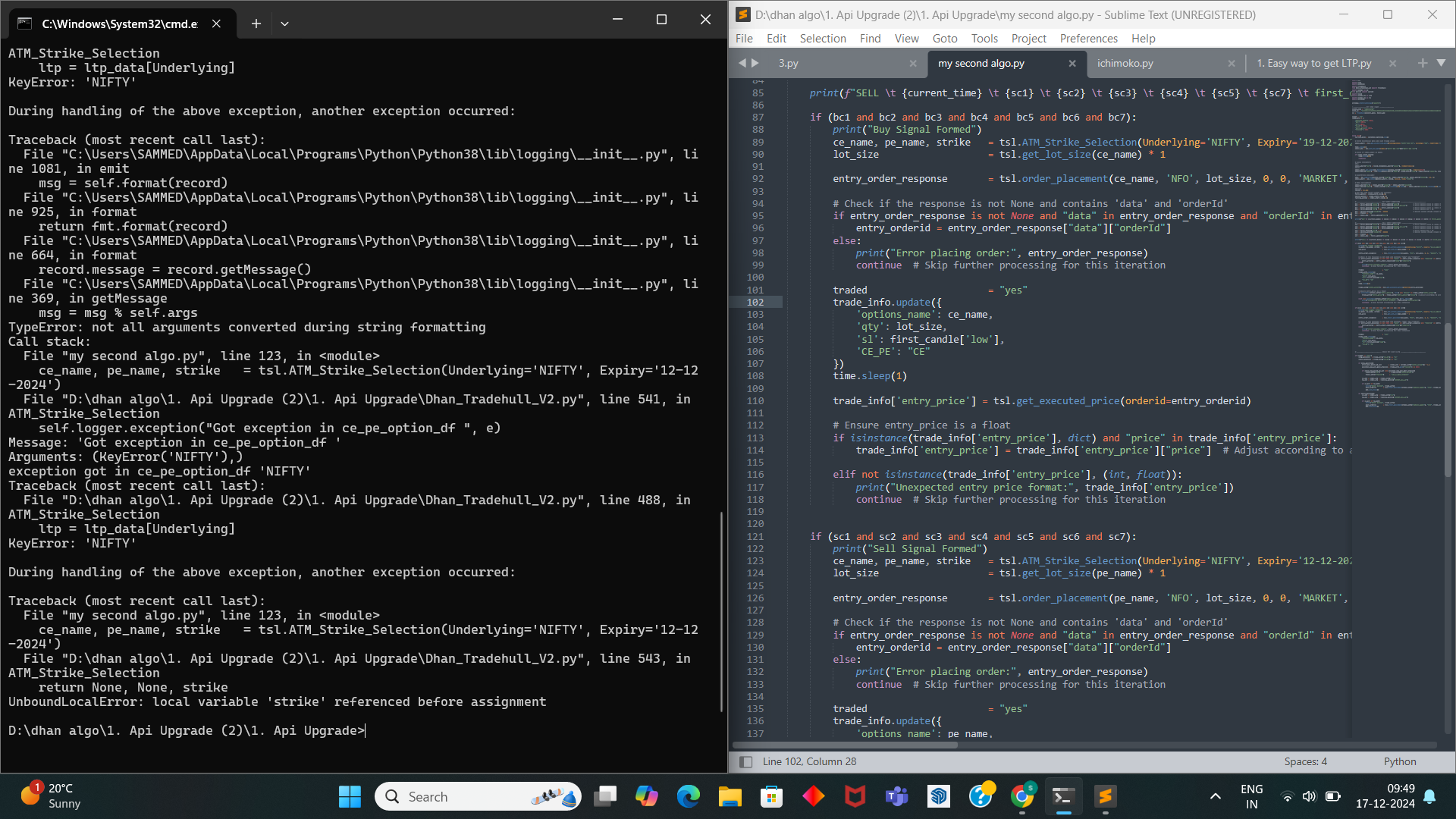

Hello Sir @Tradehull_Imran & aijaz

please help me in this, check live modification if its working at ur side or not.

even its placing new order continually but not modifying order (the same order)

i have tried all 3 its not working can any one help me in this please

1.

stoploss_orderid = tsl.Dhan.modify_order(stoploss_orderid, "STOPLIMIT", QTY, price, trigger, "MIS")

2.

stoploss_orderid = tsl.modify_order(stoploss_orderid, "STOPLIMIT", QTY, price, trigger, "MIS")

3.

stoploss_orderid = tsl.modify_order(stoploss_orderid, "STOPLIMIT", QTY, price, trigger)

error:

2024-12-16 12:22:12,164 - INFO - Buy Order Placed. Order ID: 12241216236708

2024-12-16 12:22:12,504 - INFO - Order Status: PENDING

2024-12-16 12:25:26,122 - INFO - Order Status: TRADED

2024-12-16 12:25:27,322 - INFO - Stop Loss Order Placed. Order ID: 102241216485008

2024-12-16 12:25:28,311 - INFO - Buy Price: 148.5, Current Price: 147.9, Target: 168.5, Stop Loss: 138.8

2024-12-16 12:35:00,014 - ERROR - Error in fetching order details or status: Traceback (most recent call last):

File “C:\Users\DELL\AppData\Local\Temp\ipykernel_11976\3384396219.py”, line 157, in

stoploss_orderid = tsl.Dhan.modify_order(stoploss_orderid, “STOPLIMIT”, QTY, new_sl_price - 1, new_sl_price, “MIS”)

TypeError: modify_order() missing 2 required positional arguments: ‘disclosed_quantity’ and ‘validity’

2024-12-16 12:35:00,265 - INFO - Order Status: TRADED

2024-12-16 12:35:01,564 - INFO - Stop Loss Order Placed. Order ID: 12241216245508

2024-12-16 12:35:02,502 - ERROR - Error in fetching order details or status: Traceback (most recent call last):

File “C:\Users\DELL\AppData\Local\Temp\ipykernel_11976\3384396219.py”, line 157, in

stoploss_orderid = tsl.Dhan.modify_order(stoploss_orderid, “STOPLIMIT”, QTY, new_sl_price - 1, new_sl_price, “MIS”)

TypeError: modify_order() missing 2 required positional arguments: ‘disclosed_quantity’ and ‘validity’

2024-12-16 12:35:02,761 - INFO - Order Status: TRADED

2024-12-16 12:35:03,969 - INFO - Stop Loss Order Placed. Order ID: 42241216501508

2024-12-16 12:35:04,907 - ERROR - Error in fetching order details or status: Traceback (most recent call last):

File “C:\Users\DELL\AppData\Local\Temp\ipykernel_11976\3384396219.py”, line 157, in

stoploss_orderid = tsl.Dhan.modify_order(stoploss_orderid, “STOPLIMIT”, QTY, new_sl_price - 1, new_sl_price, “MIS”)

TypeError: modify_order() missing 2 required positional arguments: ‘disclosed_quantity’ and ‘validity’

@Aijaz_Ahmad