Hello Everyone

@Tradehull_Imran

Sir, I am trying to get RSI of Index on 5 min time frame using the code but getting error

import pdb

from Dhan_Tradehull_V2 import Tradehull

import pandas as pd

import talib

import time

import datetime

Client details

client_code = “”

token_id = “”

Initialize Tradehull

tsl = Tradehull(client_code, token_id)

available_balance = tsl.get_balance()

leveraged_margin = available_balance5

max_trades = 2

per_trade_margin = (leveraged_margin/max_trades)

max_loss = (available_balance1)/100*-1

watchlist = [“NIFTY”,‘BANKNIFTY’,‘NIFTYIT’,‘NIFTYAUTO’,‘NIFTYFMCG’]

traded_wathclist =

for index_exchange in watchlist:

time.sleep(1)

chart_1 = tsl.get_historical_data(tradingsymbol = index_exchange,exchange = 'NSE',timeframe="1")

chart_5 = tsl.get_historical_data(tradingsymbol = index_exchange,exchange = 'NSE',timeframe="5") # this call has been updated to get_historical_data call,

chart_15 = tsl.get_historical_data(tradingsymbol = index_exchange,exchange = 'NSE',timeframe="15") # this call has been updated to get_historical_data call,

if (chart_1 is None) or (chart_5 is None) :

continue

if (chart_1.empty) or (chart_5.empty):

continue

if (chart_15.empty) or (chart_15.empty):

continue

if (chart_15 is None) or (chart_15 is None) :

continue

# Conditions that are on 1 minute timeframe

chart_5['rsi'] = talib.RSI(chart_5['close'], timeperiod=14) #pandas

cc_5 = chart_5.iloc[-1] #pandas completed candle of 5 min timeframe

print(stock_name, "RSI on 5 Min Time Frame is", cc_5['rsi'] )

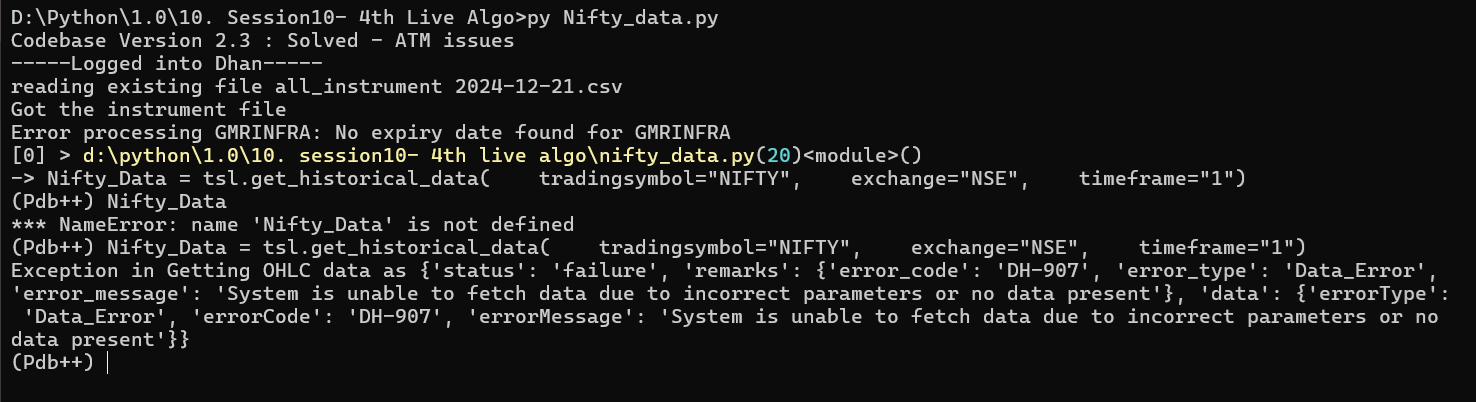

The error is

Exception in Getting OHLC data as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: ‘DH-907’, ‘error_type’: ‘Data_Error’, ‘error_message’: ‘System is unable to fetch data due to incorrect parameters or no data present’}, ‘data’: {‘errorType’: ‘Data_Error’, ‘errorCode’: ‘DH-907’, ‘errorMessage’: ‘System is unable to fetch data due to incorrect parameters or no data present’}}

Where I am doing wrong , please help