Disclaimer: This is an illustrative example for FY 2025-26 / AY 2026-27 under the new tax regime. The purpose is to explain why stock market income should not be treated as one single income block. Actual tax depends on the exact breakup of income, applicable sections, date of transfer, set-off rules, deductions, rebate eligibility and return filing status.

Rahul is a full-time investor and trader.

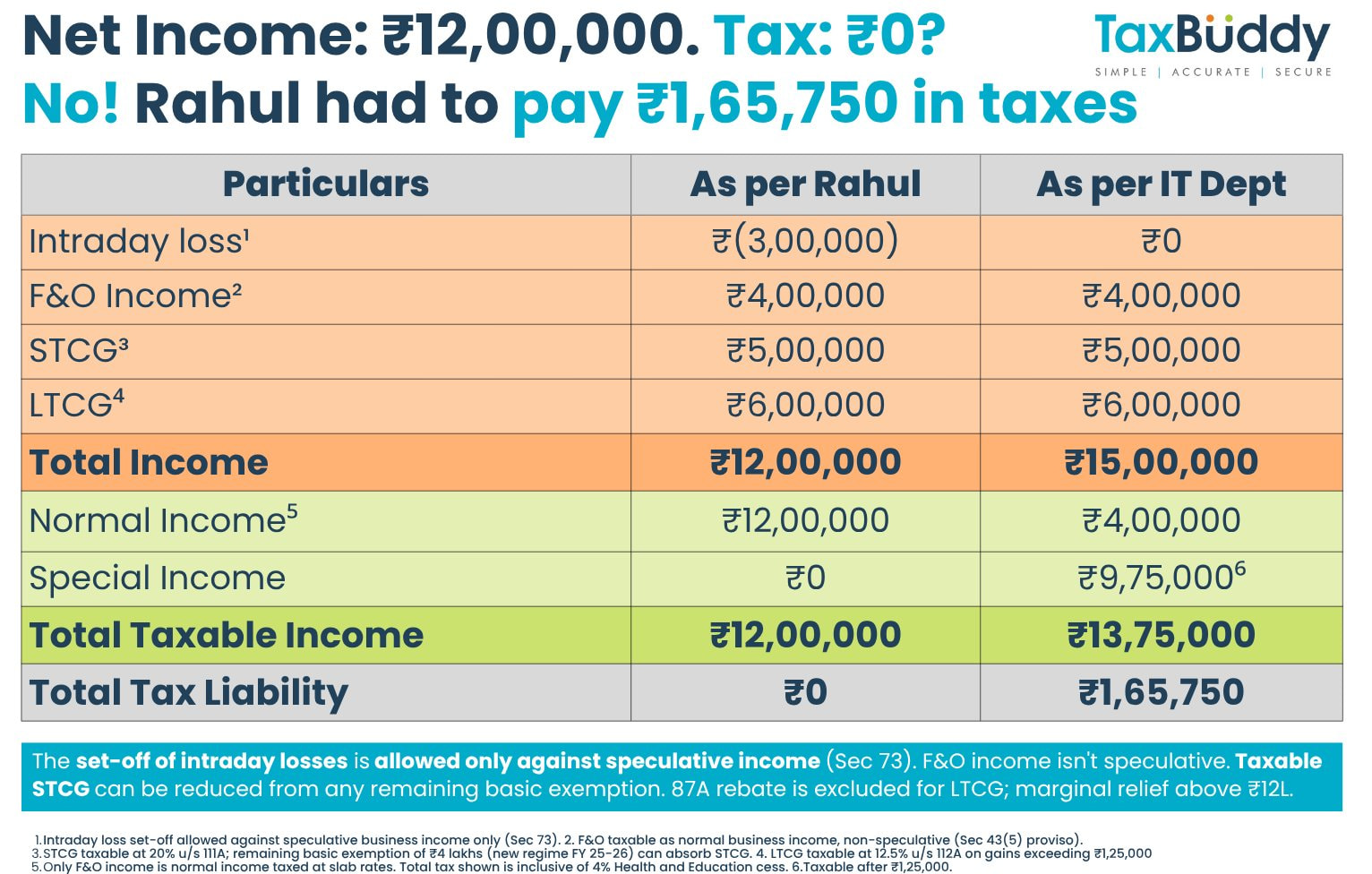

During the year, he made profits from the stock market.

He assumed:

“My income is within ₹12 lakh. So my tax should be zero under the new regime.”

But when his tax was calculated, he faced a tax shock of ₹1,65,750.

This happened because stock market income is not taxed under one simple rule.

F&O, intraday, STCG and LTCG can all have different tax treatment.

The mistake Rahul made

Rahul looked at his stock market income as one combined number.

That is where the confusion started.

The new tax regime gives rebate relief for eligible income up to the prescribed limit.

But that does not mean every type of stock market income automatically becomes tax-free.

Some income is taxed at slab rates.

Some income is taxed at special rates.

Some losses can be adjusted widely.

Some losses can be adjusted only against specific income.

So before assuming “no tax,” every trader and investor needs to classify the income correctly.

Two income heads are involved

Stock market income can mainly fall under two heads:

1. Profits and Gains from Business or Profession

This may include:

→ Intraday equity trading

→ F&O trading

2. Capital Gains

This may include:

→ Short-term capital gains under Section 111A

→ Long-term capital gains under Section 112A

These categories are not interchangeable.

The tax rate, loss adjustment rule, carry-forward period and rebate treatment can differ.

Intraday trading is speculative business income

Intraday equity trading is generally treated as speculative business income.

That means it is taxed as business income at slab rates.

But the loss treatment is restricted.

An intraday trading loss can generally be set off only against speculative business profit.

If the loss remains unadjusted, it can be carried forward for 4 years, provided the return is filed within the due date under Section 139(1).

So intraday loss should not be casually mixed with F&O loss or capital gains loss.

F&O trading is non-speculative business income

Eligible F&O trading is treated as non-speculative business income.

It is reported under:

Profits and Gains from Business or Profession

It is not capital gains.

It is not STCG.

It is not LTCG.

F&O profit is taxed at slab rates.

F&O loss can generally be set off against eligible income other than salary income.

Unadjusted F&O loss can be carried forward for 8 years, provided the return is filed within the due date.

This is why F&O traders should not skip reporting losses in the ITR.

Missing the due date or filing the wrong form can affect loss carry-forward benefits.

STCG under Section 111A is taxed separately

Short-term capital gains from listed equity shares or equity mutual funds, where STT conditions are satisfied, are taxed under Section 111A.

For transfers on or after 23 July 2024, the tax rate is 20%.

So if Rahul has STCG of ₹5 lakh under Section 111A, the tax will be:

₹5,00,000 × 20% = ₹1,00,000

This is why many investors get surprised.

They assume the new regime rebate will remove the tax impact.

But special-rate capital gains need separate checking.

LTCG under Section 112A has its own threshold

Long-term capital gains from listed equity shares or equity mutual funds, where Section 112A applies, are taxed only above the threshold limit.

For FY 2025-26, gains above ₹1.25 lakh are taxable.

For transfers on or after 23 July 2024, the tax rate is 12.5%.

So if Rahul has LTCG of ₹6 lakh:

Taxable LTCG = ₹6,00,000 - ₹1,25,000

Taxable amount = ₹4,75,000

Tax at 12.5% = ₹59,375

This tax does not disappear simply because Rahul assumed his overall income was within the rebate zone.

How Rahul’s tax shock happened

Rahul’s tax was calculated based on different buckets of income.

F&O profit taxed at slab rates: ₹0

STCG under Section 111A: ₹1,00,000

LTCG under Section 112A: ₹59,375

Subtotal tax: ₹1,59,375

Health and Education Cess at 4%: ₹6,375

Total tax payable: ₹1,65,750

The tax shock happened because Rahul treated all stock market income as one simple income figure.

But the law does not treat every stock market profit in the same way.

The Section 87A rebate confusion

The biggest misunderstanding is this:

“Income up to ₹12 lakh means no tax in every case.”

That is not always correct.

Section 87A rebate under the new regime has limits and conditions.

More importantly, certain special-rate incomes need separate treatment.

Tax on LTCG under Section 112A is not covered in the same way as normal slab income for rebate purposes.

So an investor with capital gains should not assume automatic zero tax only by looking at the total income number.

Why this matters for AY 2026-27

For AY 2026-27, trading income reporting has become more structured in the ITR forms.

F&O traders now need to report specific details such as:

→ F&O turnover

→ Income from F&O trading credited to the Profit & Loss account

These details are reported under Schedule Part A-Trading Account in the applicable ITR form.

For most individual F&O traders, the correct form is generally ITR-3.

This is especially important where there is F&O income, intraday trading, losses, books of account, turnover reporting or business expenses.

Documents Rahul should keep ready

Before filing the ITR, a trader or investor should keep:

→ Broker P&L statement

→ Capital gains statement

→ Tax P&L statement

→ F&O turnover calculation

→ Intraday turnover calculation

→ Bank statement

→ Brokerage and charges breakup

→ Expense proofs, wherever claimed

→ Books of account, wherever applicable

These documents help in reporting income correctly and avoiding mistakes in classification.

Key takeaway

→ Stock market income is not taxed with one single formula.

→ F&O is business income.

→ Intraday is speculative business income.

→ STCG under Section 111A has a special rate.

→ LTCG under Section 112A has a threshold and a special rate.

→ Loss adjustment rules are also different.

So before assuming that ₹12 lakh income means zero tax, check what the income is made of.

Because in stock market taxation, the real problem is often not the profit.

It is the wrong classification of that profit.