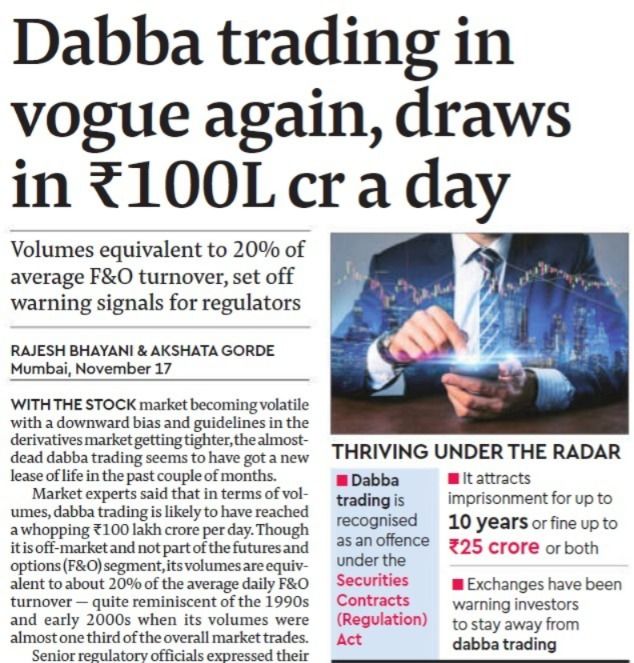

in the realm of Indian stock markets, the controversial practice of dabba trading has resurfaced, drawing an eye-popping ₹100 lakh crore in daily volumes. This underground activity, equivalent to a staggering 20% of the average daily turnover in the futures and options (F&O) segment, is once again under the spotlight, raising alarms among regulators and market experts.

What is Dabba Trading?

Dabba trading refers to off-market trades where investors bypass official exchanges like NSE and BSE. Instead, transactions are settled through a local operator or broker without actual execution on regulated exchanges. While this practice is alluring for its zero compliance costs, it operates in stark violation of the Securities Contracts (Regulation) Act, with heavy penalties and imprisonment of up to 10 years or fines as high as ₹25 crore for violators.

Why is Dabba Trading Making a Comeback?

- Volatility in Stock Markets:

- Recent volatility and a bearish market bias have driven many traders to seek cost-efficient ways to hedge risks or speculate. Dabba trading offers a low-cost, high-leverage alternative to official platforms.

- Tighter Regulations in F&O:

- The Securities and Exchange Board of India (SEBI) has imposed stricter margin requirements and position limits in F&O trading. These measures, aimed at controlling excessive risk-taking, have inadvertently pushed some traders to dabba operators.

- Ease of Operations:

- Dabba trading circumvents regulatory complexities. Without the need for margin deposits or KYC requirements, it offers faster and simpler access, appealing to smaller investors and speculators.

- Tax Evasion:

- Since dabba trades occur off the books, they allow participants to evade taxes such as the Securities Transaction Tax (STT), Commodity Transaction Tax (CTT), and GST, making it financially attractive despite the risks.

Impact on the Market

The resurgence of dabba trading poses significant risks to the Indian financial ecosystem:

- Regulatory Challenges: The off-market nature of dabba trading undermines SEBI’s efforts to maintain transparency and investor protection.

- Revenue Loss: Government and exchanges lose revenue from taxes and transaction fees.

- Increased Risk: Dabba trading lacks safeguards like margin calls or investor protection mechanisms, exposing participants to heightened financial and legal risks.

Could Reduction in Weekly Expiries Fuel Dabba Trading?

One of the recent changes in the Indian derivatives market has been the reduction in weekly expiries, a move aimed at stabilizing excessive speculative activity. While this decision may seem prudent, it could unintentionally lead to:

- Reduced Trading Opportunities:

- Weekly expiries are highly popular among retail traders for short-term speculative bets. Curtailing them could push these traders to dabba operators to sustain their activity.

- Lower Market Liquidity:

- With fewer trading opportunities on official platforms, liquidity could decline, making off-market options like dabba trading more attractive.

- Increased Speculation in Unregulated Spaces:

- If retail traders perceive official platforms as less flexible or lucrative, they may migrate to dabba trading to maintain high-frequency speculative activities.

While the reduction in weekly expiries aims to bring discipline to F&O markets, regulators must also address the unintended consequence of potentially driving participants to illegal avenues.

Way Forward

- Strengthen Enforcement:

- Regulators need to ramp up surveillance and crack down on dabba trading networks, leveraging technology to track unregulated activities.

- Education and Awareness:

- Investors must be educated about the legal, financial, and systemic risks of dabba trading. Exchanges and SEBI can run targeted campaigns to warn against the practice.

- Streamline Regulations:

- Simplifying compliance processes and reducing transaction costs for official trading platforms can make them more competitive with illegal alternatives.

- Monitor Changes in Market Structure:

- SEBI should assess the impact of changes like reducing weekly expiries on market participation, ensuring they do not inadvertently boost illegal trading practices.

Conclusion

The resurgence of dabba trading underscores the need for a balanced regulatory approach. While measures like tighter F&O guidelines and reduced weekly expiries aim to enhance market stability, they must not come at the cost of driving activity underground. Regulators, exchanges, and market participants must collaborate to curb dabba trading and safeguard the integrity of India’s financial markets.