Hi everyone,

Yesterday an article came in the business standard making a point a lot of us have felt in our portfolios: through the West Asia tension, foreign investors have been heavy sellers while domestic institutions and retail have quietly held the market up. The article puts it plainly, FPIs net sellers, DIIs channelling money in, and retail snapping up ₹19,664 crore in April, their biggest single month since October 2024.

It’s a good read, and the flow data backs every word of it. What the data adds is the precision the headline can’t, just how cleanly domestic money matched the foreign exit.

The offset was almost rupee for rupee

Lay the March and April flows side by side:

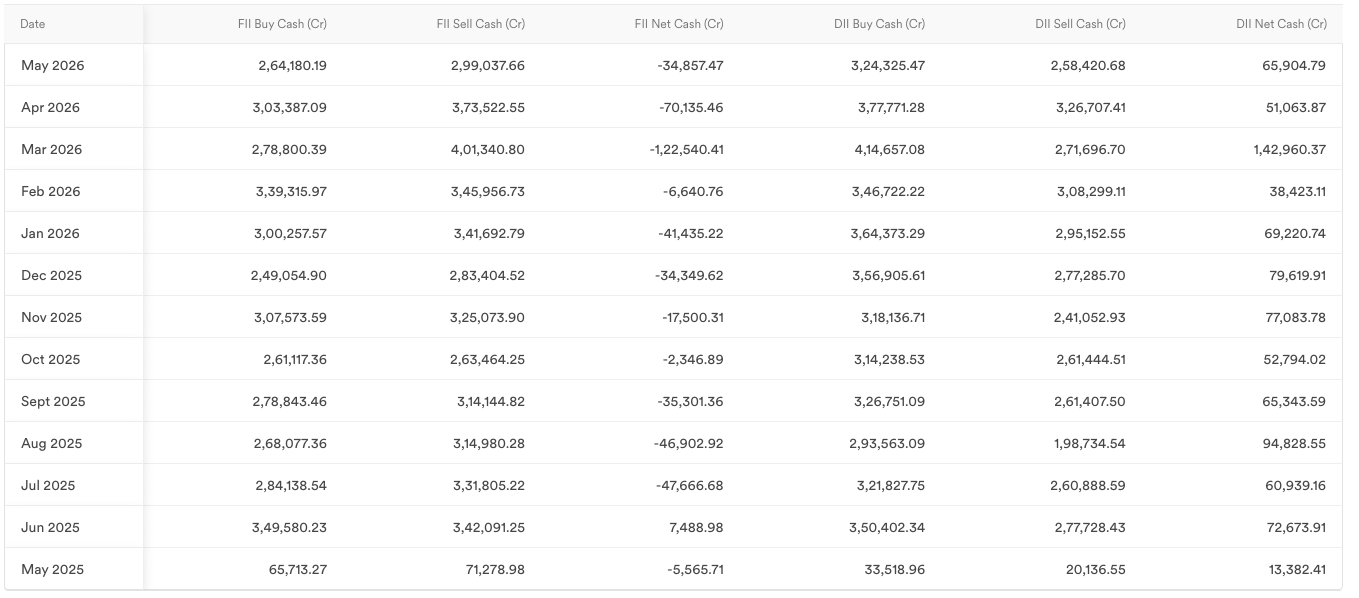

| Month | FII net (₹ cr) | DII net (₹ cr) |

|---|---|---|

| Mar 2026 | -1,22,540 | +1,42,960 |

| Apr 2026 | -70,135 | +51,064 |

| Two-month total | -1,92,675 | +1,94,024 |

Here’s the data from ScanX insights as well:

Foreigners took out roughly ₹1.93 lakh crore. Domestic institutions put in roughly ₹1.94 lakh crore. The gap between the two is about ₹1,350 crore, which on a base this size is essentially a rounding error. When the article says DIIs steadied the market, this is what that sentence looks like in numbers: not a vague cushion, but an almost exact, month-on-month absorption of everything the foreigners sold.

Retail wasn’t just present. It leaned in.

The ₹19,664 crore of direct retail buying in April being the biggest since October 2024 isn’t a small footnote. It tells you the dip-buying reflex the article describes, the SIP-bred habit of treating falls as opportunities, has graduated from autopilot into active conviction. People didn’t just keep their SIPs running through the scare. They added on top, deliberately, while the headlines were at their worst.

Why the precision matters

A near-perfect FII-DII offset is a structurally calmer market than the raw “₹2 lakh crore sold” headline suggests. It means foreign exits were being met by a domestic bid deep enough to clear them without forcing a disorderly fall. That’s exactly why the broader market could begin its smallcap and midcap recovery even while FPIs were still leaving, the selling had a buyer waiting on the other side every single month. The article gets the direction right. The flow data shows the mechanism. (Worth reading next to the rupee thread, since a softer currency is half the reason the FPIs were heading out in the first place.)

And the freshest reading? The pressure is easing.

Bringing it right up to now: the most recent prints suggest the foreign selling is losing steam. May’s monthly FPI outflow has shrunk to roughly ₹35,000 crore, well below March and April, while DIIs kept buying. The latest daily and weekly numbers tell the same story, FIIs still nibbling on the sell side (around -₹1,043 cr on the day, -₹2,629 cr on the week) against steady DII buying (+₹3,821 cr daily, +₹9,039 cr weekly). The tug of war the article describes is still on. It’s just gotten a good deal quieter.

When the selling was at its scariest in March, were you a buyer or a watcher?