Hey everyone,

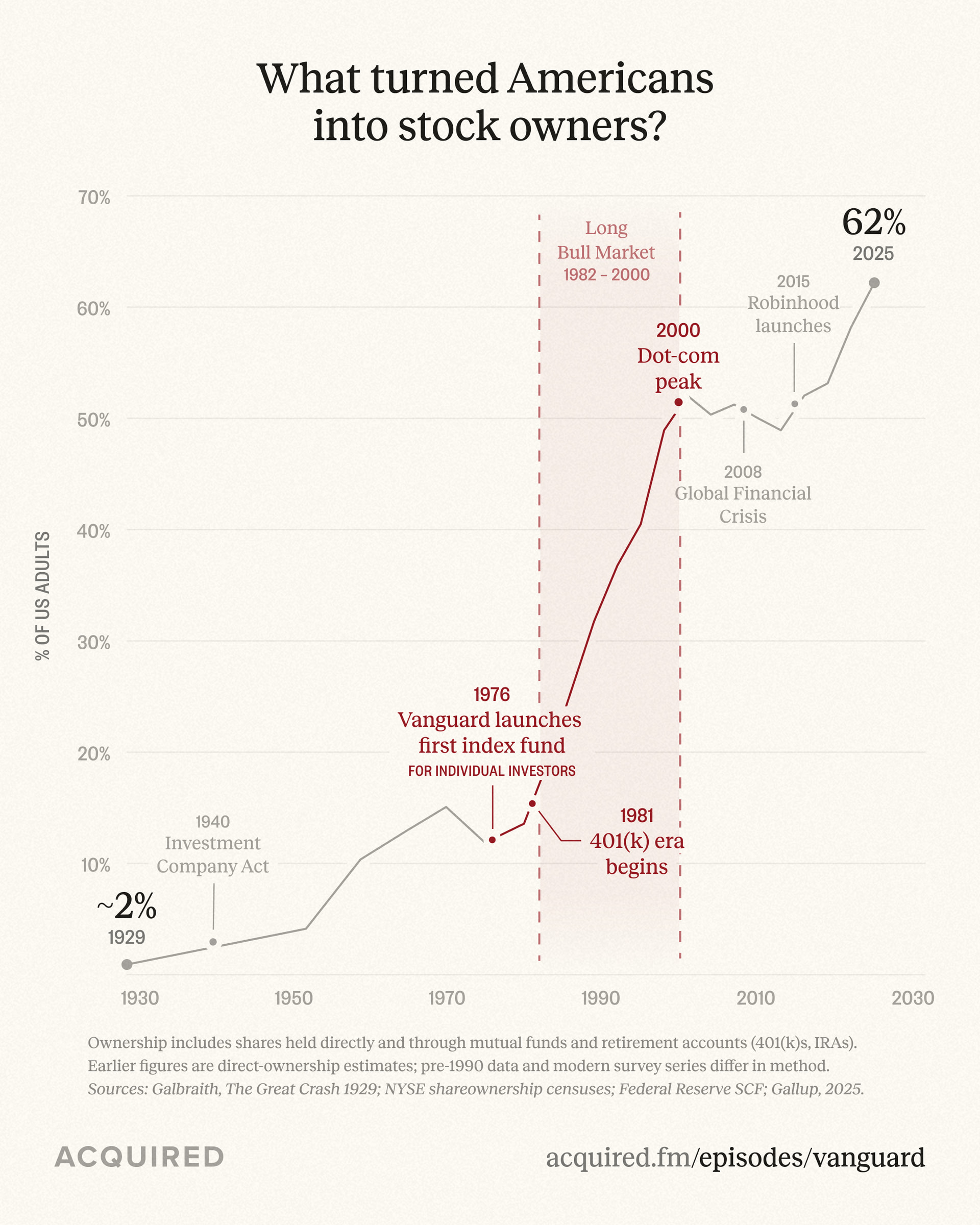

Came across a brilliant chart from the Acquired podcast’s Vanguard episode and could not stop thinking about it. It tracks the share of US adults who own stock, from roughly 2% in 1929 to 62% in 2025, and the story behind each jump is far more interesting than “the market went up.”

The big takeaway: Americans did not become owners because they suddenly got richer or smarter. Ownership exploded every time someone removed a barrier, cost, access, or friction. Here is the breakdown of each trigger, and then where we Indians fit into the same picture.

The triggers, one by one

1929, ~2% own stock. Before the Great Crash, the market was a rich person’s club. As Galbraith documents in The Great Crash 1929, only a tiny sliver of households held shares directly. The crash hurt that group, but the bigger damage was psychological, it scared off a whole generation.

1940, Investment Company Act. This is not a spike, it is the foundation. After the Depression, Congress built guardrails: disclosure rules, limits on leverage and conflicts of interest, a real legal structure for mutual funds. Pooled investing finally became safe enough for ordinary people to trust. Nothing big happens for decades, but nothing later happens without this.

1970, ~15% (the first plateau). Post-war prosperity slowly pulled more people in, but it was still mostly direct stock-picking by the comfortable. Then the brutal 1973 to 1974 bear market and stagflation knocked confidence flat.

1976, Vanguard launches the first index fund for individual investors. Jack Bogle’s radical pitch: stop trying to beat the market, just own all of it, cheaply. Wall Street openly mocked it as “Bogle’s Folly” and even called indexing “un-American” (why settle for average?). The launch was a flop, it raised around 11 million dollars against a 150 million dollar target. It also quietly collapsed the cost of investing for normal people, which is the whole reason it mattered.

1981, the 401(k) era begins. Arguably the single biggest driver on the entire chart. The shift from company-managed pensions to payroll-deduction retirement accounts meant millions of regular workers were funneled into mutual funds automatically, without ever calling a broker. Investing went from a decision you had to make to a default that happened to you.

1982 to 2000, the Long Bull Market. Now the flywheel spins. Monthly 401(k) money flowing in, plus cheap index funds, plus a market running from roughly 110 to 1,500 on the S&P. Ownership roughly doubled, from around 25% to 51%.

2000, Dot-com peak (~51%), then 2008 GFC. Internet mania pulled retail in, the bust and then the financial crisis pushed participation back down. Confidence is fragile.

2015, Robinhood launches. The last barrier to fall: friction. Zero commissions, mobile-first, tap-to-trade. It set up the huge retail wave of 2020 and 2021.

2025, 62%. An all-time high.

The throughline, every leap came from structure changing, not sentiment: cheaper (index funds), automatic (401k), frictionless (mobile).

Now look at India on the same curve

Here is what makes this fun. We are running the exact same playbook, just a few decades behind and much faster.

Demat investing only started here in 1996. It then took about 25 years to cross 11 crore accounts (around 2022). After that it went vertical, crossing 20 crore demat accounts by late 2025 / early 2026 (CDSL and NSDL data). Our own versions of the US triggers all landed at once:

| US trigger | India’s equivalent |

|---|---|

| Index funds collapse cost | Discount brokers and zero / low brokerage |

| 401(k) makes investing automatic | The SIP habit, monthly auto-debit into funds |

| Robinhood removes friction | UPI plus Aadhaar e-KYC, account open in minutes |

| Long bull market compounds it | The post-2020 domestic equity run |

And the SIP engine is genuinely staggering. Per AMFI, monthly SIP inflows hit a record ₹32,087 crore in March 2026, and equity mutual funds have now logged an unbroken inflow streak since March 2021, over five straight years, through every dip and geopolitical scare. Industry AUM sits near ₹81.6 lakh crore, up from about ₹10 lakh crore a decade ago. Roughly 75% of new demat accounts in 2025 belonged to under-30s, and most of the growth is coming from tier-2 and tier-3 cities, not the metros.

But here is the honest, important nuance: the US chart measures 62% of adults. India’s 20 crore demat accounts sit in a population of 140 crore plus, only about 1 in 4 of those accounts is even active, and one person often holds several. So our true share of investing adults is still in single digits to low teens depending on how you count. In other words, on the US curve, India is somewhere around the late 1970s to early 1980s, right at the base of the climb, just before the structure kicked in and sent it vertical.

That is the exciting part. If the pattern holds, we are early.

It Took America a Century to Turn Workers Into Investors. India is Doing it in a Decade.

The part that ties both charts together

Here is what struck me most. That entire American climb, from 2% to 62%, is the story of ordinary people coming to own American companies. For most of our investing lives, watching that chart meant watching from the outside, reading about Apple and Microsoft and Amazon compounding for decades while our money stayed in one market.

That is the thing that has quietly changed. Today an Indian investor does not have to choose between the two curves, you can sit on both at once. One portfolio riding the Indian demat and SIP boom we just walked through, and another holding the same global names that powered the chart above. You can do exactly that from within Dhan, which means the old “India or the US” debate quietly turns into a much healthier “how much of each.”

And owning both is not about chasing returns in dollars. It is real diversification, across two economies, two currencies, and two different growth engines. When the rupee softens, your unhedged US holdings actually cushion you a little, the kind of spread that used to be the privilege of large institutions and is now sitting in a retail portfolio. A lot of what we build here has come straight out of these community conversations, and being able to hold an Indian and a US book side by side is one of those quietly big shifts that is easy to miss while it is happening.

So I am curious about your own setup: do you already hold both an Indian and a US slice in your portfolio, or are you still fully on one side of the line?