On October 1, 2024, SEBI issued a circular introducing measures to strengthen the equity derivatives framework. These measures aim to enhance investor protection and ensure market stability, addressing the growing retail participation and speculative trading activities in the segment. The circular outlines six key measures, which will be implemented in phases from November 20, 2024, to April 1, 2025, depending on the specific provision.

Here’s a summary of the three measures that will take effect from November 20, 2024:

1. Rationalisation of Weekly Index Derivatives (Effective November 20, 2024)

SEBI has limited weekly index derivatives to a single benchmark index per exchange. For example, NSE will offer weekly derivatives on Nifty 50, while BSE will offer weeklies on Sensex.

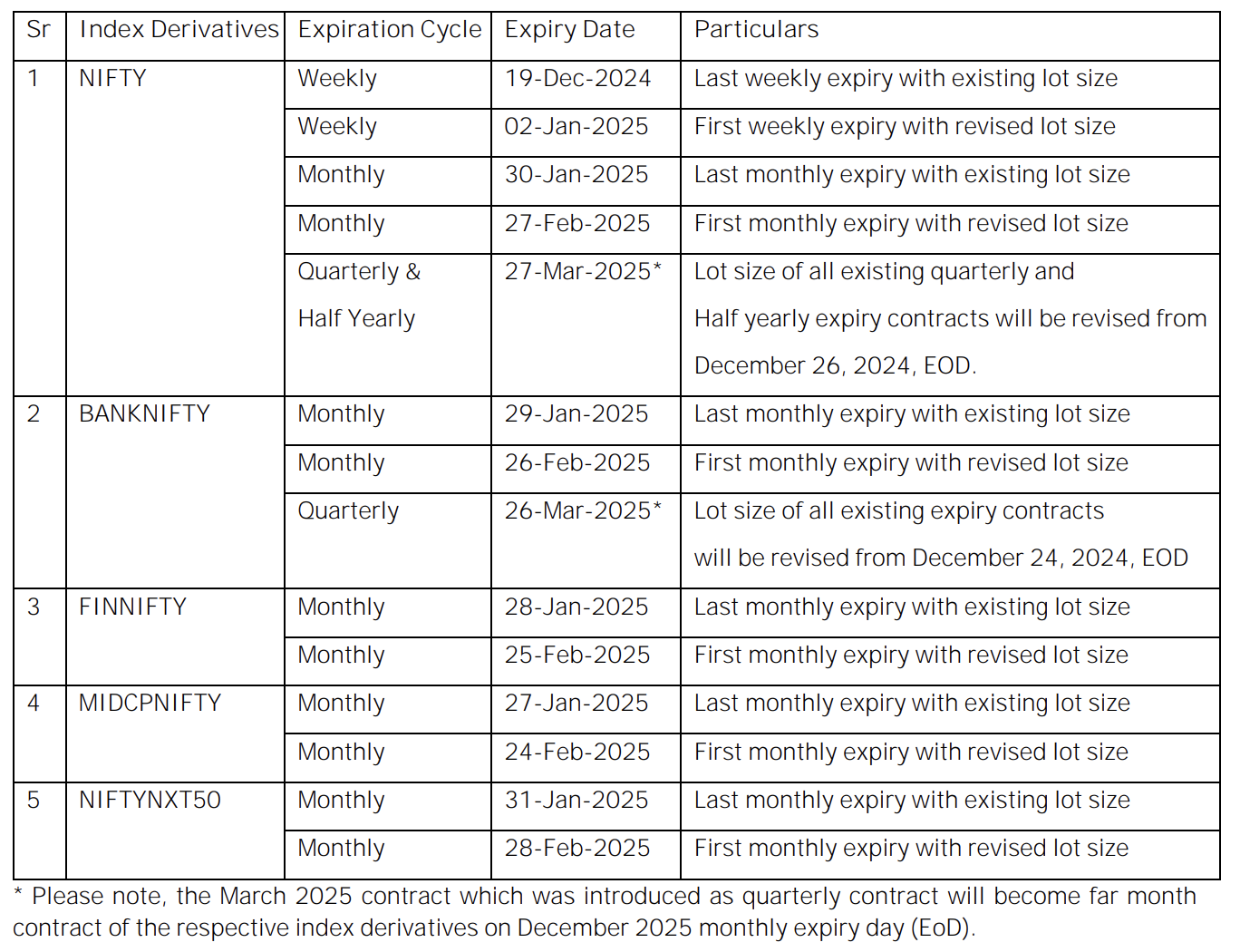

2. Revision of Index Derivatives Lot Sizes (Effective November 20, 2024)

SEBI has raised the minimum contract value for index derivatives to ₹15–20 lakhs. In turn NSE & BSE issued the circulars to change the lot sizes. It is important to note that the lot sizes for existing contracts will remain unchanged as of November 20, 2024. However, all new contracts introduced after this date will follow the revised lot sizes. The updated lot sizes for contracts introduced post-November 20, 2024, are as follows:

| Underlying Index | Existing Market Lot | Revised Market Lot |

|---|---|---|

| Nifty 50 | 25 | 75 |

| Nifty Bank | 15 | 30 |

| Nifty Financial Services | 25 | 65 |

| Nifty Midcap Select | 50 | 120 |

| Nifty Next 50 | 10 | 25 |

| Sensex | 10 | 20 |

| Bankex | 15 | 30 |

| Sensex 50 | 25 | 60 |

3. Increased ELM for Short Options on Expiry Day (Effective November 20, 2024)

To account for tail risks during volatile expiry day, SEBI has introduced an additional Extreme Loss Margin (ELM) of 2% for all short options positions expiring on the same day.

Extreme Loss Margin (ELM) is an additional margin levied by exchanges to cover potential tail risks. In simple words, ELM is a mechanism to calculate the risk associated with the contract in unforeseen conditions. This ensures a buffer for unanticipated losses that could arise in volatile market conditions, providing additional protection to the market and its participants.

On the day of options contract expiry, speculative activity tends to increase sharply, with traders taking high-risk positions to capitalise on short-term price fluctuations. This heightened speculative activity can lead to sudden, large price movements, creating significant risks for traders holding short positions. Did you hear injections?

To address these risks, SEBI has mandated an additional ELM of 2% to be levied on all short options positions that are due to expire on the same day. This will apply both to short positions that are open at the start of the trading day and to new short positions initiated during the day.

The relevant circulars are attached for your reference.

SEBI, NSE, BSE