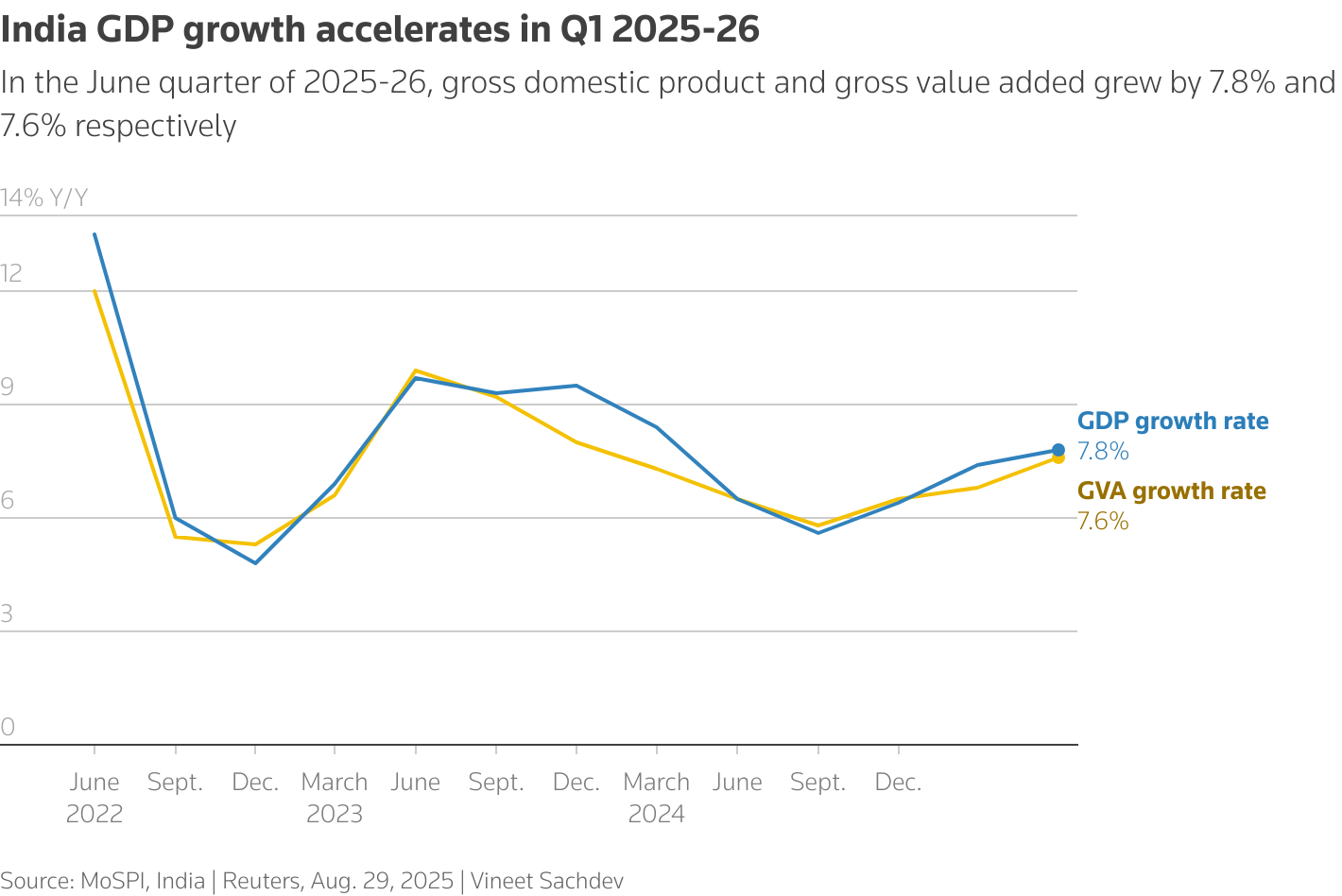

India’s economy outpaced expectations in the April–June quarter (Q1 FY26), with GDP expanding at 7.8% YoY — the fastest in five quarters. This resilience comes despite global headwinds and the looming threat of U.S. tariff hikes, which could pressure exports and corporate earnings in coming quarters.

![]() Key Economic Data (Q1 FY26: April–June)

Key Economic Data (Q1 FY26: April–June)

| Indicator | Q1 FY26 | Previous Quarter | Trend/Notes |

|---|---|---|---|

| GDP Growth (YoY) | 7.8% | 7.4% | Fastest in 5 quarters; above 6.7% forecast |

| Gross Value Added (GVA) | 7.6% | 6.8% | Stronger underlying activity |

| Private Consumption | 7.0% | 6.0% | Boost from rural demand, tractors, durables |

| Govt Spending | +7.4% | -1.8% | Fiscal push adds support |

| Capital Expenditure | +7.8% | — | Some private hesitancy amid global uncertainty |

| Manufacturing Output | +7.7% | 4.8% | Strong rebound |

| Construction | +7.6% | 10.8% | Slight moderation |

| Agriculture | +3.7% | 5.4% | Weaker on base effect |

| Nominal GDP | 8.8% | Avg ~11% (last 8 qtrs) | Cooling inflation pressure |

| Rupee vs USD | Record low: ₹88.30 | — | Pressure from tariff-driven outflows |

| Equity Markets | 2nd month of losses | — | Growth strong, but sentiment cautious |

![]() The U.S. Tariff Overhang

The U.S. Tariff Overhang

- U.S. doubled tariffs on Indian imports to as high as 50%, citing India’s Russian oil trade.

- Potential impact areas: textiles, leather goods, chemicals.

- Exporter groups estimate 55% of India’s $87B exports to U.S. could be affected.

- Competitors benefit: Vietnam, Bangladesh, and China may gain share.

- Economists warn 0.6–0.8% shaved off GDP growth if tariffs persist.

![]() Trader’s Perspective

Trader’s Perspective

-

Equity Markets: While real GDP is strong, slowing nominal GDP and tariff risks could weigh on corporate earnings → cautious sentiment ahead.

-

Rupee Watch: Fresh record low shows how quickly external shocks spill over. Exporters may gain in INR terms, but import-heavy sectors (oil, electronics) suffer.

-

Sector Moves:

- Positive: Domestic consumption plays (FMCG, tractors, durables), infra (govt spending support).

- Negative: Export-heavy sectors (textiles, chemicals, leather), rate-sensitive plays if RBI stays cautious.

-

Macro Setup: RBI steady at 5.50% repo rate; growth outlook still ~6.5% FY26, but risks tilted to the downside.

![]() Bottom line for traders: India remains the fastest-growing large economy, but U.S. tariffs are a genuine downside risk. Watch export-heavy stocks, rupee sensitivity, and consumption plays this festive season for cues.

Bottom line for traders: India remains the fastest-growing large economy, but U.S. tariffs are a genuine downside risk. Watch export-heavy stocks, rupee sensitivity, and consumption plays this festive season for cues.