Hi @Arun_Rawat

The sell orders is incorrect, this is sending sell orders after every 10 seconds.

Do send the code as well. we need to block repeated orders

Hi @Arun_Rawat

The sell orders is incorrect, this is sending sell orders after every 10 seconds.

Do send the code as well. we need to block repeated orders

Dhan Tradehull codebase link : Notion

Also we will be releasing new codebase document in upcoming weeks.

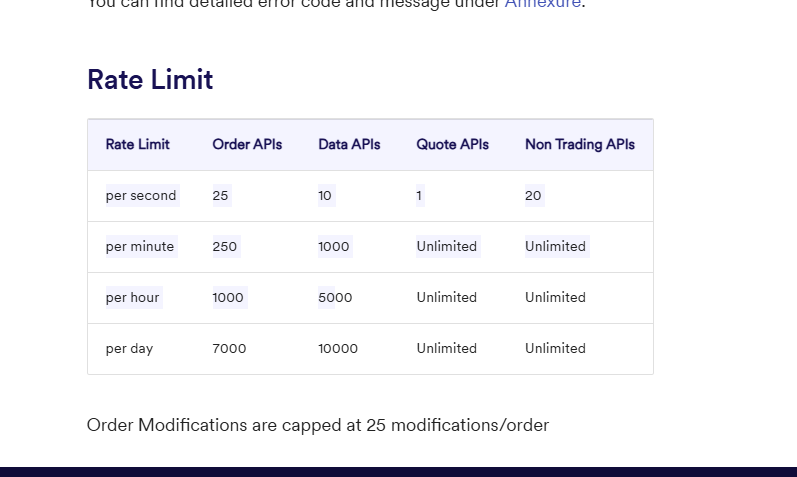

The rate limits are as follows

For tick data, (LTP/OHLC/QUOTE) … quote api is being used and yes we can request data for 1000 scripts in 1 api call when calling quote data (LTP/OHLC/QUOTE)

Dhan-Tradehull codebase LTP function supports the same

You have given a good suggestion we will extend this functionality for OHLC and Quote as well

data = tsl.get_ltp_data(names=['CRUDEOIL', 'NIFTY'])

.

.

Now for Historical chart data

The OHLC that was being referred to in dhanhq document.. is Open high low and close value for the current day only

{"open": 4521.45,"close": 4507.85,"high": 4530,"low": 4500}

for the chart level historical data for various timeframes [1/2/3/4/510/15/60]…

we need to call the Data Api.. which has only 7000 allowed calls per day,

which is nearly 1 api call after 3.3 seconds.

@Tradehull_Imran Sir,

Please find the code.

import pdb

import time

import datetime

import traceback

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as pta

import pandas_ta as ta

import warnings

from Dhan_Tradehull_V2 import Tradehull

warnings.filterwarnings(“ignore”)

client_code = “”

token_id = “”

tsl = Tradehull(client_code, token_id)

available_balance = tsl.get_balance()

leveraged_margin = available_balance * 2

max_trades = 3

per_trade_margin = leveraged_margin / max_trades

max_loss = available_balance / 100 * -1

traded = “no”

trade_info = {“options_name”: None, “qty”: None, “sl”: None, “CE_PE”: None}

while True:

live_pnl = tsl.get_live_pnl()

current_time = datetime.datetime.now().time() # time only

if current_time < datetime.time(9, 45, 0):

print("Wait for the market to open", current_time)

continue

if current_time > datetime.time(15, 15, 30) or (live_pnl < max_loss):

tsl.kill_switch('ON')

tsl.cancel_all_orders()

print("Market is over or MAX LOSS reached, Bye for Now", current_time)

break

print("Algo is working", current_time)

try:

index_chart = tsl.get_historical_data(tradingsymbol='NIFTY JAN FUT', exchange='NFO', timeframe="5")

time.sleep(3)

index_ltp = tsl.get_ltp_data(names=['NIFTY JAN FUT'])['NIFTY JAN FUT']

except Exception as e:

print(e)

continue

# Apply Indicators

index_chart['rsi'] = talib.RSI(index_chart['close'], timeperiod=14)

index_chart.set_index(pd.DatetimeIndex(index_chart['timestamp']), inplace=True)

index_chart['vwap'] = pta.vwap(index_chart['high'], index_chart['low'], index_chart['close'], index_chart['volume'])

indi = ta.supertrend(index_chart['high'], index_chart['low'], index_chart['close'], 10, 2)

index_chart = pd.concat([index_chart, indi], axis=1, join='inner')

index_chart['pv'] = index_chart['close'] * index_chart['volume']

index_chart['vwma'] = index_chart['pv'].rolling(20).mean() / index_chart['volume'].rolling(20).mean()

first_candle = index_chart.iloc[-3]

second_candle = index_chart.iloc[-2]

running_candle = index_chart.iloc[-1]

# Buy Entry Conditions

bc1 = first_candle['close'] > first_candle['vwap']

bc2 = first_candle['close'] > first_candle['SUPERT_10_2.0']

bc3 = first_candle['close'] > first_candle['vwma']

bc4 = first_candle['rsi'] > 60

bc5 = first_candle['rsi'] < 80

#(data['RSI'] > 60) & (data['RSI'] < 80)

bc6 = second_candle['volume'] > 50000

bc7 = traded == "no"

bc8 = index_ltp > first_candle['low']

print(f"BUY \t {current_time} \t {bc1} \t {bc2} \t {bc3} \t {bc4} \t {bc5} \t {bc7} \t {bc8} \t first_candle {str(first_candle['timestamp'].time())}")

# Sell Entry Conditions

sc1 = first_candle['close'] < first_candle['vwap']

sc2 = first_candle['close'] < first_candle['SUPERT_10_2.0']

sc3 = first_candle['close'] < first_candle['vwma']

sc4 = first_candle['rsi'] > 20

sc5 = first_candle['rsi'] < 40

sc6 = second_candle['volume'] > 50000

sc7 = traded == "no"

sc8 = index_ltp < first_candle['high']

print(f"SELL \t {current_time} \t {sc1} \t {sc2} \t {sc3} \t {sc4} \t {sc5} \t {sc7} \t {sc8} \t first_candle {str(first_candle['timestamp'].time())} \n")

if bc1 and bc2 and bc3 and bc4 and bc5 and bc6 and bc7 and bc8:

print("Buy Signal Formed")

CE_symbol_name, PE_symbol_name, strike_price = tsl.ATM_Strike_Selection(Underlying='NIFTY', Expiry=0)

# CE_symbol_name, PE_symbol_name, strike_price = tsl.ATM_Strike_Selection(Underlying='ACC', Expiry=0)

if (CE_symbol_name is None) or (PE_symbol_name is None):

continue

lot_size = tsl.get_lot_size(CE_symbol_name) * 1

entry_orderid = tsl.order_placement(CE_symbol_name, 'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info.update({"options_name": CE_symbol_name, "qty": lot_size, "sl": first_candle['low'], "CE_PE": "CE"})

if sc1 and sc2 and sc3 and sc4 and sc5 and sc6 and sc7 and sc8:

print("Sell Signal Formed")

CE_symbol_name, PE_symbol_name, strike = tsl.ATM_Strike_Selection(Underlying='NIFTY', Expiry=0)

if (CE_symbol_name is None) or (PE_symbol_name is None):

continue

lot_size = tsl.get_lot_size(PE_symbol_name) * 1

entry_orderid = tsl.order_placement(PE_symbol_name, 'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info.update({"options_name": PE_symbol_name, "qty": lot_size, "sl": first_candle['high'], "CE_PE": "PE"})

# Check for exit SL/TG

if traded == "yes":

long_position = trade_info['CE_PE'] == "CE"

short_position = trade_info['CE_PE'] == "PE"

if long_position:

sl_hit = index_ltp < trade_info['sl']

tg_hit = index_ltp < running_candle['SUPERT_10_2.0']

if sl_hit or tg_hit:

print("Order Exited", trade_info)

tsl.order_placement(trade_info['options_name'], 'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

if short_position:

sl_hit = index_ltp > trade_info['sl']

tg_hit = index_ltp > running_candle['SUPERT_10_2.0']

if sl_hit or tg_hit:

print("Order Exited", trade_info)

tsl.order_placement(trade_info['options_name'], 'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

Hi @Rajashekhar_Rangappa

Yes I have raised this issue to Dhan Team.

Hi @Rajashekhar_Rangappa @Arun_Rawat

There seems to be an issue in pnl function…

We are working on its fix, don’t use pnl function till then as it may give incorrect data.

Hi @CHETAN_99

Use this tested framework code,

import pdb

import time

import datetime

import traceback

from Dhan_Tradehull import Tradehull

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as ta

import xlwings as xw

import winsound

client_code = "1102790337"

token_id = "eyJ0eXAiOiJKV1QiLCJhbGciOiJIUzUxMiJ9.eyJpc3MiOiJkaGFuIiwicGFydG5lcklkIjoiIiwiZXhwIjoxNzM2ODYwMTMxLCJ0b2tlbkNvbnN1bWVyVHlwZSI6IlNFTEYiLCJ3ZWJob29rVXJsIjoiIiwiZGhhbkNsaWVudElkIjoiMTEwMjc5MDMzNyJ9.Leop6waGeVfmBOtczNEcjRWmC8pUGWQf54YPINGDi_PZjk1IvW-DDdaYXsgM_s8McOT44q4MjEQxGXU0lduK0A"

tsl = Tradehull(client_code,token_id)

# pre_market_watchlist = ['ASIANPAINT', 'BAJAJ-AUTO', 'BERGEPAINT', 'BEL', 'BOSCHLTD', 'BRITANNIA', 'COALINDIA', 'COLPAL', 'DABUR', 'DIVISLAB', 'EICHERMOT', 'GODREJCP', 'HCLTECH', 'HDFCBANK', 'HAVELLS', 'HEROMOTOCO', 'HAL', 'HINDUNILVR', 'ITC', 'IRCTC', 'INFY', 'LTIM', 'MARICO', 'MARUTI', 'NESTLEIND', 'PIDILITIND', 'TCS', 'TECHM', 'WIPRO']

# watchlist = []

# for name in pre_market_watchlist:

# print("Pre market scanning ", name)

# day_chart = tsl.get_historical_data(tradingsymbol = name,exchange = 'NSE',timeframe="DAY")

# day_chart['upperband'], day_chart['middleband'], day_chart['lowerband'] = talib.BBANDS(day_chart['close'], timeperiod=20, nbdevup=2, nbdevdn=2, matype=0)

# last_day_candle = day_chart.iloc[-1]

# upper_breakout = last_day_candle['high'] > last_day_candle['upperband']

# lower_breakout = last_day_candle['low'] < last_day_candle['lowerband']

# if upper_breakout or lower_breakout:

# watchlist.append(name)

# print(f"\t selected {name} for trading")

# pdb.set_trace()

# print(watchlist)

# # pdb.set_trace()

watchlist = ['BEL', 'BOSCHLTD', 'COLPAL', 'HCLTECH', 'HDFCBANK', 'HAVELLS', 'HAL', 'ITC', 'IRCTC', 'INFY', 'LTIM', 'MARICO', 'MARUTI', 'NESTLEIND', 'PIDILITIND', 'TCS', 'TECHM', 'WIPRO']

single_order = {'name':None, 'date':None , 'entry_time': None, 'entry_price': None, 'buy_sell': None, 'qty': None, 'sl': None, 'exit_time': None, 'exit_price': None, 'pnl': None, 'remark': None, 'traded':None}

orderbook = {}

wb = xw.Book('Live Trade Data.xlsx')

live_Trading = wb.sheets['Live_Trading']

completed_orders_sheet = wb.sheets['completed_orders']

reentry = "yes" #"yes/no"

completed_orders = []

bot_token = "8059847390:AAECSnQK-yOaGJ-clJchb1cx8CDhx2VQq-M"

receiver_chat_id = "1918451082"

live_Trading.range("A2:Z100").value = None

completed_orders_sheet.range("A2:Z100").value = None

for name in watchlist:

orderbook[name] = single_order.copy()

while True:

print("starting while Loop \n\n")

current_time = datetime.datetime.now().time()

if current_time < datetime.time(13, 55):

print(f"Wait for market to start", current_time)

time.sleep(1)

continue

if current_time > datetime.time(15, 15):

order_details = tsl.cancel_all_orders()

print(f"Market over Closing all trades !! Bye Bye See you Tomorrow", current_time)

pdb.set_trace()

break

all_ltp = tsl.get_ltp_data(names = watchlist)

for name in watchlist:

orderbook_df = pd.DataFrame(orderbook).T

live_Trading.range('A1').value = orderbook_df

completed_orders_df = pd.DataFrame(completed_orders)

completed_orders_sheet.range('A1').value = completed_orders_df

current_time = datetime.datetime.now()

print(f"Scanning {name} {current_time}")

try:

chart = tsl.get_historical_data(tradingsymbol = name,exchange = 'NSE',timeframe="5")

chart['rsi'] = talib.RSI(chart['close'], timeperiod=14)

cc = chart.iloc[-2]

# buy entry conditions

bc1 = cc['rsi'] > 45

bc2 = orderbook[name]['traded'] is None

except Exception as e:

print(e)

continue

if bc1 and bc2:

print("buy ", name, "\t")

margin_avialable = tsl.get_balance()

margin_required = cc['close']/4.5

if margin_avialable < margin_required:

print(f"Less margin, not taking order : margin_avialable is {margin_avialable} and margin_required is {margin_required} for {name}")

continue

orderbook[name]['name'] = name

orderbook[name]['date'] = str(current_time.date())

orderbook[name]['entry_time'] = str(current_time.time())[:8]

orderbook[name]['buy_sell'] = "BUY"

orderbook[name]['qty'] = 1

try:

entry_orderid = tsl.order_placement(tradingsymbol=name ,exchange='NSE', quantity=orderbook[name]['qty'], price=0, trigger_price=0, order_type='MARKET', transaction_type='BUY', trade_type='MIS')

orderbook[name]['entry_orderid'] = entry_orderid

orderbook[name]['entry_price'] = tsl.get_executed_price(orderid=orderbook[name]['entry_orderid'])

orderbook[name]['tg'] = round(orderbook[name]['entry_price']*1.002, 1) # 1.01

orderbook[name]['sl'] = round(orderbook[name]['entry_price']*0.998, 1) # 99

sl_orderid = tsl.order_placement(tradingsymbol=name ,exchange='NSE', quantity=orderbook[name]['qty'], price=0, trigger_price=orderbook[name]['sl'], order_type='STOPMARKET', transaction_type ='SELL', trade_type='MIS')

orderbook[name]['sl_orderid'] = sl_orderid

orderbook[name]['traded'] = "yes"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"Entry_done {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

except Exception as e:

print(e)

pdb.set_trace(header= "error in entry order")

if orderbook[name]['traded'] == "yes":

bought = orderbook[name]['buy_sell'] == "BUY"

if bought:

try:

ltp = all_ltp[name]

sl_hit = tsl.get_order_status(orderid=orderbook[name]['sl_orderid']) == "TRADED"

tg_hit = ltp > orderbook[name]['tg']

except Exception as e:

print(e)

pdb.set_trace(header = "error in sl order cheking")

if sl_hit:

try:

orderbook[name]['exit_time'] = str(current_time.time())[:8]

orderbook[name]['exit_price'] = tsl.get_executed_price(orderid=orderbook[name]['sl_orderid'])

orderbook[name]['pnl'] = round((orderbook[name]['exit_price'] - orderbook[name]['entry_price'])*orderbook[name]['qty'],1)

orderbook[name]['remark'] = "Bought_SL_hit"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"SL_HIT {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

if reentry == "yes":

completed_orders.append(orderbook[name])

orderbook[name] = None

except Exception as e:

print(e)

pdb.set_trace(header = "error in sl_hit")

if tg_hit:

try:

tsl.cancel_order(OrderID=orderbook[name]['sl_orderid'])

time.sleep(2)

square_off_buy_order = tsl.order_placement(tradingsymbol=orderbook[name]['name'] ,exchange='NSE', quantity=orderbook[name]['qty'], price=0, trigger_price=0, order_type='MARKET', transaction_type='SELL', trade_type='MIS')

orderbook[name]['exit_time'] = str(current_time.time())[:8]

orderbook[name]['exit_price'] = tsl.get_executed_price(orderid=square_off_buy_order)

orderbook[name]['pnl'] = (orderbook[name]['exit_price'] - orderbook[name]['entry_price'])*orderbook[name]['qty']

orderbook[name]['remark'] = "Bought_TG_hit"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"TG_HIT {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

if reentry == "yes":

completed_orders.append(orderbook[name])

orderbook[name] = None

winsound.Beep(1500, 10000)

except Exception as e:

print(e)

pdb.set_trace(header = "error in tg_hit")

Hi @Siddh_Shah

Solution link : https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718/983?u=tradehull_imran

Hello @Tradehull_Imran Sir

aaj subah se ye error aa rha hai ![]() (same code is yesterday runing fine but today i am facing this essue) please help

(same code is yesterday runing fine but today i am facing this essue) please help

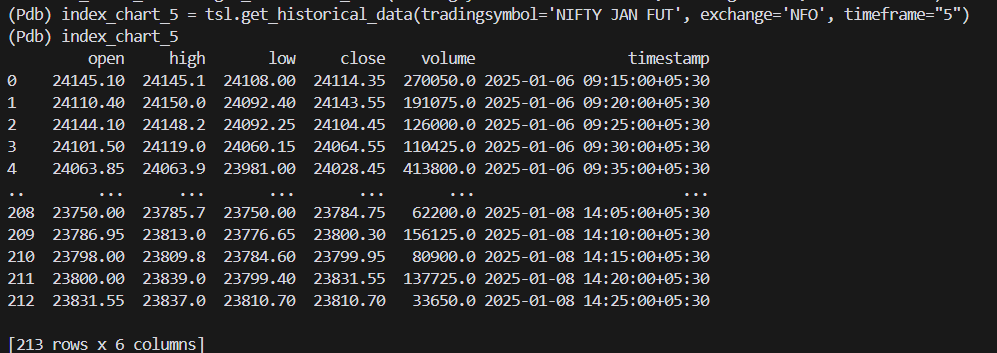

Exception in Getting OHLC data as Check the Tradingsymbol or Exchangepaste code here

index_chart_5 = tsl.get_historical_data(tradingsymbol='NIFTY JAN FUT', exchange='NFO', timeframe="5")

Sir, I am getting the Error by Running this code addressed to Mr.Chetan.

How to resolve it sir.

C:\Users\RP\Desktop\DHAN Algorhythemic Trading\Codes from MadeForTrade Forum>py “IA to Chetan MumWrkShop.py”

-----Logged into Dhan-----

This BOT Is Picking New File From Dhan

Got the instrument file

Traceback (most recent call last):

File “IA to Chetan MumWrkShop.py”, line 61, in

wb = xw.Book(‘Live Trade Data.xlsx’)

File “C:\Users\RP\AppData\Local\Programs\Python\Python38\lib\site-packages\xlwings\main.py”, line 929, in init

impl = app.books.open(

File “C:\Users\RP\AppData\Local\Programs\Python\Python38\lib\site-packages\xlwings\main.py”, line 5153, in open

raise FileNotFoundError(“No such file: ‘%s’” % fullname)

FileNotFoundError: No such file: ‘Live Trade Data.xlsx’

Hi @Tradehull_Imran , I have kept the sleep time as time.sleep(1), still I am getting below error

Scanning APOLLOHOSP…

Exception in Getting OHLC data as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: ‘DH-904’, ‘error_type’: ‘Rate_Limit’, ‘error_message’: ‘Too many requests on server from single user breaching rate limits. Try throttling API calls.’}, ‘data’: {‘errorType’: ‘Rate_Limit’, ‘errorCode’: ‘DH-904’, ‘errorMessage’: ‘Too many requests on server from single user breaching rate limits. Try throttling API calls.’}}

Insufficient data for APOLLOHOSP. Skipping…

Traceback (most recent call last):

File “Breakout Algo on Stock Options.py”, line 37, in

time.sleep(0.2)

KeyboardInterrupt

Can you please suggest what appropriate sleep time I should keep? I was running two algos at the same time with the same watchlist.

Hello Imran, can you help me to create a new code with strategy ?

thank you. Do let us know once the new document is ready.

I am not able to get Historical price for Future Contract (BANK Nifty JAN 25) via Tradehull API. Exception in Getting OHLC data as For Future or Commodity, DAY - Timeframe not supported by API, SO choose another timeframe Please help on fixing this error. [image]

Thank you Rahul Bhai for arranging upcoming event at bangalore ![]()

is trade hull version 2 is the order placement updated for bracket orders?

Hi @vinay_kumaar ,

It seems the code is working fine. Do try again and let us know if you face any issue

Hi @Vasili_Prasad ,

We need to create “Live Trade Data.xlsx” excel sheet as the error suggests:

FileNotFoundError: No such file: ‘Live Trade Data.xlsx’

Hello @Tradehull_Imran Sir

code Runing fine (P C file missing problem)

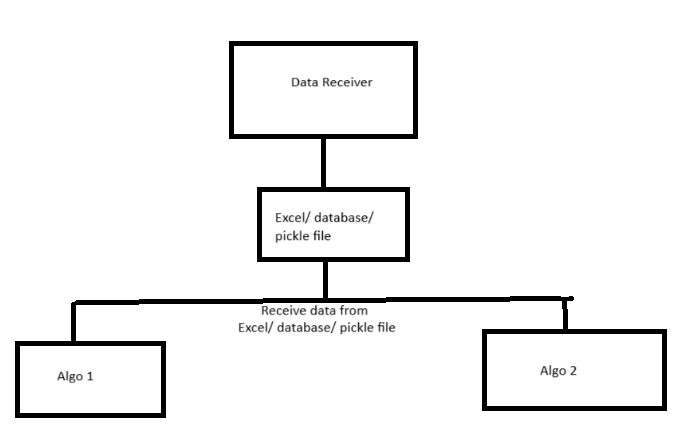

Hi @ddeogharkar ,

Below are the possible solutions:

We can use 2 Dhan account with different API’s.

Since the watchlist is same, make a data receiver file that will retrieve the data for both the algo’s. The data should be sent in excel/ database/ pickle file and both the algo’s will refer to the same excel/ database/ pickle file for fetching data .

Also you can double the sleep time in Dhan_Tradehull_V2.

![[image]](https://private-poc.madefortrade.in/uploads/default/original/3X/a/5/a585d60896911407e80c6d397829a9948add37fc.png){kind=link}