Do share your code as well, I will check if some optimization in code is possible or not.

Also tagging @Hardik for rate limits.

Do share your code as well, I will check if some optimization in code is possible or not.

Also tagging @Hardik for rate limits.

@Tradehull_Imran Sir,

Is there any way or source from where we can get older OHLCV of 3 minute or 5 minute timeframe data like 6 month or 1 year for stocks of our choices. if any other community member can help in the same, please help. thanks in advance.

Regards,

Hi @Vinod_Kumar1

we will be covering this in upcoming OSB video.

The code seems to be working fine

Do use latest codebase file : https://drive.google.com/file/d/1h8J6VOLrHMAaF1NGP4_vJj2wtkNxfPDw/view

Do share the access to tradehull_mentorship@tradehull.com

@Tradehull_Imran Sir Thanks For Solving The Query

Done Sir.

Thank you for replying sir. It is working now in VISUAL STUDIO CODE, I think there was something wrong with sublime text.

Dear Sir @Tradehull_Imran,

I am getting following two errors, please help i am using ltp_data = tsl.get_ltp_data(open_stocks) every 60 seconds only for the stocks for which i have position open these could be max 2 to 5 at a time, still i am getting being blocked warnings.

Exception at calling ltp as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: None, ‘error_type’: None, ‘error_message’: None}, ‘data’: {‘data’: {‘805’: ‘Too many requests. Further requests may result in the user being blocked.’}, ‘status’: ‘failed’}}

got exception in pnl as ‘Titan’

def monitor_open_positions():

"""

Monitor open positions and manage stop-loss or profit targets in live mode.

If limit orders don't trigger as expected, place market orders.

"""

global current_positions, mode, order_api_calls, consolidated_data, tsl, data_api_calls

if mode != "live":

print("monitor_open_positions is not running because the mode is not live.")

return

while True:

try:

current_time = datetime.datetime.now(pytz.timezone("Asia/Kolkata"))

# Get open stocks from current_positions

open_stocks = [

stock for stock, position in current_positions.items()

if position["type"] != "None"

]

# End-of-Day (EOD) position closure at 3:10 PM IST

if current_time.time() >= datetime.time(15, 10) and mode == "live":

if not open_stocks:

print("No open positions to Close at 3:10 PM IST.")

else:

print("Closing all positions at 3:10 PM IST.")

message = "Closing all positions at 3:10 PM in monitoring mode"

send_telegram_message(message, ongroup)

with rate_limit_lock:

order_api_calls += 1

tsl.cancel_all_orders() # Cancel all open orders

force_close_positions() # Force close open positions

break # Exit monitoring loop after EOD closure

if not open_stocks:

print("No open positions to monitor.")

time.sleep(120) # Monitor every 120 seconds if no open positions

continue

print(f"Monitoring open positions for stocks: {', '.join(open_stocks)}")

message=f"Monitoring open positions for stocks: {', '.join(open_stocks)}"

if mode == 'live':

send_telegram_message(message)

ltp_data = {}

with rate_limit_lock:

data_api_calls += 1

ltp_data = tsl.get_ltp_data(open_stocks) # Correct usage of get_ltp_data

# Retry mechanism for missing LTP

retry_count = 0

while retry_count < 3 and any(ltp is None for ltp in ltp_data.values()):

print(f"LTP missing for some stocks. Retrying... ({retry_count+1}/3)")

time.sleep(2)

with rate_limit_lock:

data_api_calls += 1

ltp_data = tsl.get_ltp_data(open_stocks)

retry_count += 1

# Handle missing LTP by fallback to last known price or skip

for stock_name in open_stocks:

ltp = ltp_data.get(stock_name)

if ltp is None:

print(f"LTP missing for {stock_name}. Using last known price.")

ltp = (

consolidated_data[consolidated_data["stockName"] == stock_name]

.sort_values(by="timestamp", ascending=False)

.iloc[0]["close"]

)

if ltp is None:

print(f"Warning: No LTP or fallback for {stock_name}. Skipping...")

continue

# Monitor Stop-Loss and Profit Target

position = current_positions[stock_name]

check_and_manage_orders(stock_name, ltp, position)

ManageOpenPositions(ltp_data)

time.sleep(60) # Monitor at intervals

except Exception as e:

print(f"Error in monitoring positions: {e}")

time.sleep(10) # Add small delay before retry

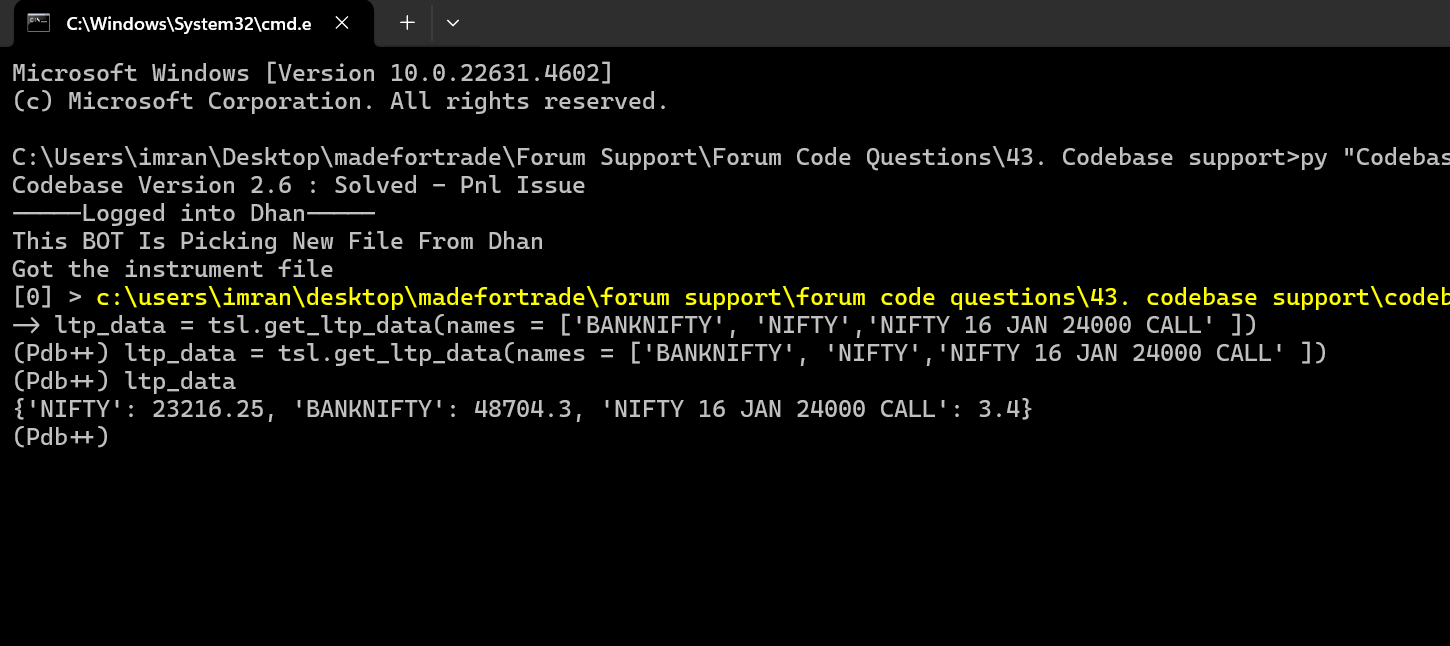

tsl = Tradehull(client_id,access_token)

ltp_data = tsl.get_ltp_data(names = ['BANKNIFTY', 'NIFTY','NIFTY 16 JAN 24000 CALL' ])

print(ltp_data)

getting error anyone please help me

Hi all,

I am happy to share that the 20-depth market data is now live on DhanHQ APIs.

You can start using 20 - Market Depth directly with the documentation here - 20 Market Depth - DhanHQ Ver 2.0 / API Document

Read more about the feature here: https://private-poc.madefortrade.in/t/introducing-20-depth-market-data-on-dhanhq-data-apis/40679

Awesome @RahulDeshpande Ji. Delivered as promised.

Thank you.

use this latest codebase file .. its has rate limit issues fixed in it : https://drive.google.com/file/d/1h8J6VOLrHMAaF1NGP4_vJj2wtkNxfPDw/view?usp=sharing

Also are you running multiple algo in parallel or 1 algo only.

Hi @kumarmohit

The code seems to be working fine. Delete all_instrument file inside Dependencies folder and try again.

let me know if it works

code seems to be working fine now

use below file

import pdb

import time

import datetime

import traceback

from Dhan_Tradehull_V2 import Tradehull

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as pta

import pandas_ta as ta

import warnings

import math

warnings.filterwarnings("ignore")

# ---------------for dhan login ----------------

client_code = ""

token_id = ""

tsl = Tradehull(client_code,token_id)

watchlist = [ "ADANIPORTS", "M&M", "SBILIFE", "MARUTI", "SHRIRAMFIN", "SUNPHARMA", "ADANIENT", "BEL", "BHARTIARTL", "BPCL", "BAJAJ-AUTO", "CIPLA", "TRENT", "TATAMOTORS", "COALINDIA", "ONGC", "DRREDDY", "KOTAKBANK", "HEROMOTOCO", "HDFCLIFE", "ULTRACEMCO", "HINDALCO", "SBIN", "BRITANNIA", "POWERGRID", "APOLLOHOSP", "HCLTECH", "TATASTEEL", "EICHERMOT", "NTPC", "BAJFINANCE", "INFY", "ICICIBANK", "AXISBANK", "WIPRO", "LT", "TCS", "HINDUNILVR", "ITC", "HDFCBANK", "BAJAJFINSV", "INDUSINDBK", "RELIANCE", "TECHM", "NESTLEIND", "GRASIM", "JSWSTEEL", "TATACONSUM", "ASIANPAINT", "TITAN"]

# index_chart = tsl.get_historical_data(tradingsymbol= watchlist, exchange='NSE', timeframe='15') # use for equity

#index_chart = tsl.get_historical_data(tradingsymbol= 'NIFTY JAN FUT', exchange='NFO', timeframe='15') # Use for Option

def market_type(num):

if num > 1.47:

return "very_bullish"

if 0.75 < num < 1.46:

return "bullish"

if 0 < num < 0.74:

return "neutral"

if -0.7 < num < 0:

return "bearish"

if num <= -0.7:

return "very_bearish"

def sqn(df, period):

df['pnl_sqn'] = ((df['close'] - df['open']) / df['open'])*100

df['average_pnl'] = df['pnl_sqn'].rolling(period).mean()

df['average_std'] = df['pnl_sqn'].rolling(period).std()

name = 'sqn'

df[name] = (math.sqrt(period)*df['average_pnl'])/df['average_std']

df.drop(columns=['pnl_sqn', 'average_pnl', 'average_std'], inplace=True)

return df

# Implementation

# sqn_lib.sqn(df=df, period=21)

# df['market_type'] = df['sqn'].apply(sqn_lib.market_type)

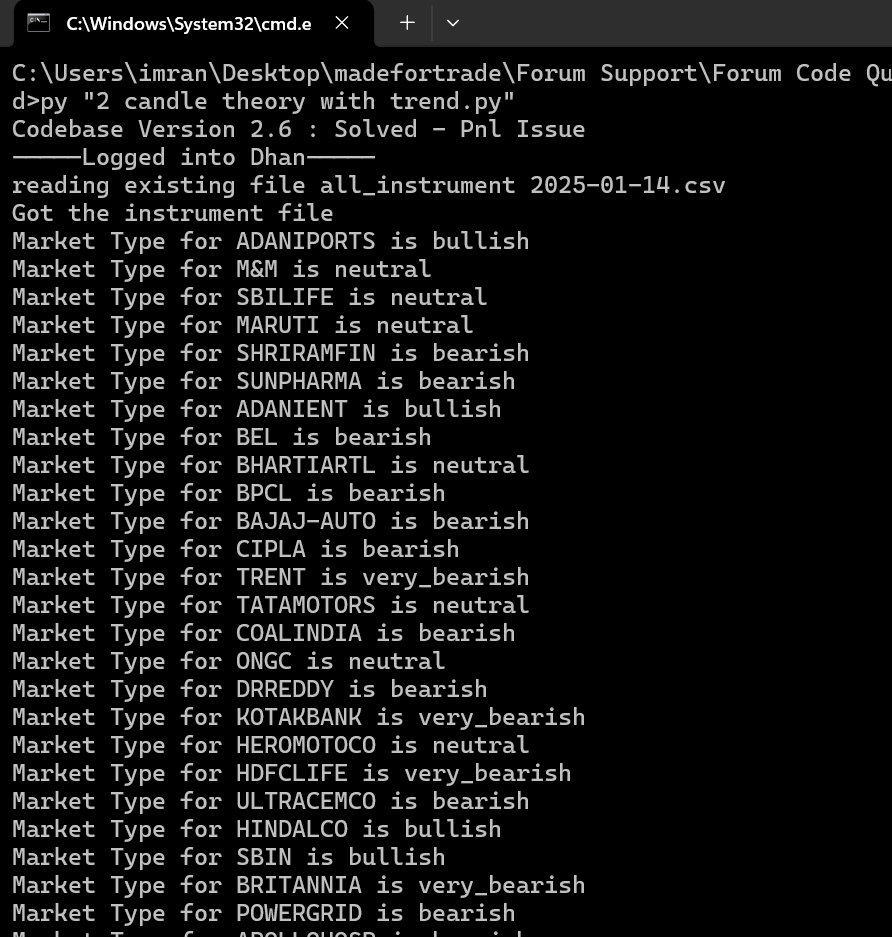

for name in watchlist:

index_chart = tsl.get_historical_data(tradingsymbol = name,exchange = 'NSE',timeframe="15")

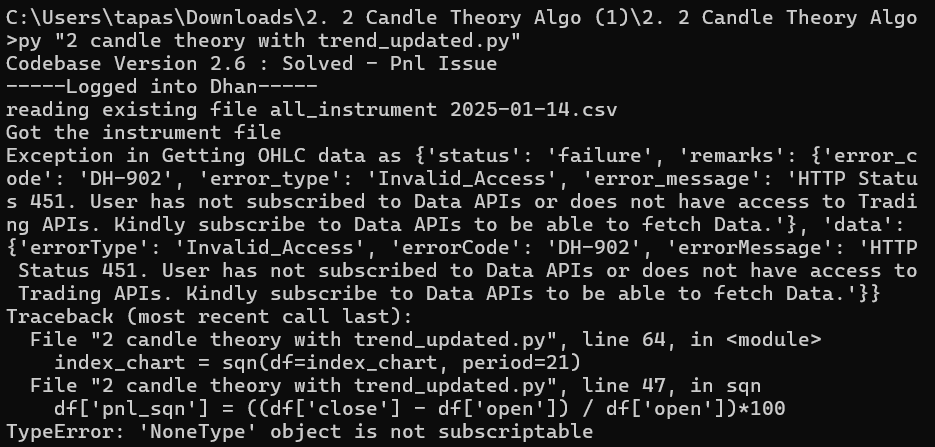

index_chart = sqn(df=index_chart, period=21)

index_chart['market_type'] = index_chart['sqn'].apply(market_type)

last_candle = index_chart.iloc[-1]

market_type_x = last_candle['market_type'] # we cant keep variabe name same as fuction name

print(f"Market Type for {name} is {market_type_x}")

#---------------------------------- apply indicators -------------------------------------------------------------

# rsi

index_chart['rsi'] = talib.RSI(index_chart['close'], timeperiod=14)

# vwap

index_chart.set_index(pd.DatetimeIndex(index_chart['timestamp']), inplace= True)

index_chart['vwap'] = pta.vwap(index_chart['high'] , index_chart['low'], index_chart['close'] , index_chart['volume'])

# Supertrend

indi = ta.supertrend(index_chart['high'], index_chart['low'], index_chart['close'], 10, 2)

index_chart = pd.concat([index_chart, indi], axis= 1, join='inner')

# vwma

index_chart['pv'] = index_chart['close'] * index_chart['volume']

index_chart['vwma'] = index_chart['pv'].rolling(34).mean() / index_chart['volume'].rolling(34).mean()

# # volume

# volume = 50,000

# # # first_candle = index_chart.iloc[-3]

# # # second_candle = index_chart.iloc[-2]

# # # running_candle = index_chart.iloc[-1]

Also use latest version of codebase : https://drive.google.com/file/d/1h8J6VOLrHMAaF1NGP4_vJj2wtkNxfPDw/view?usp=sharing

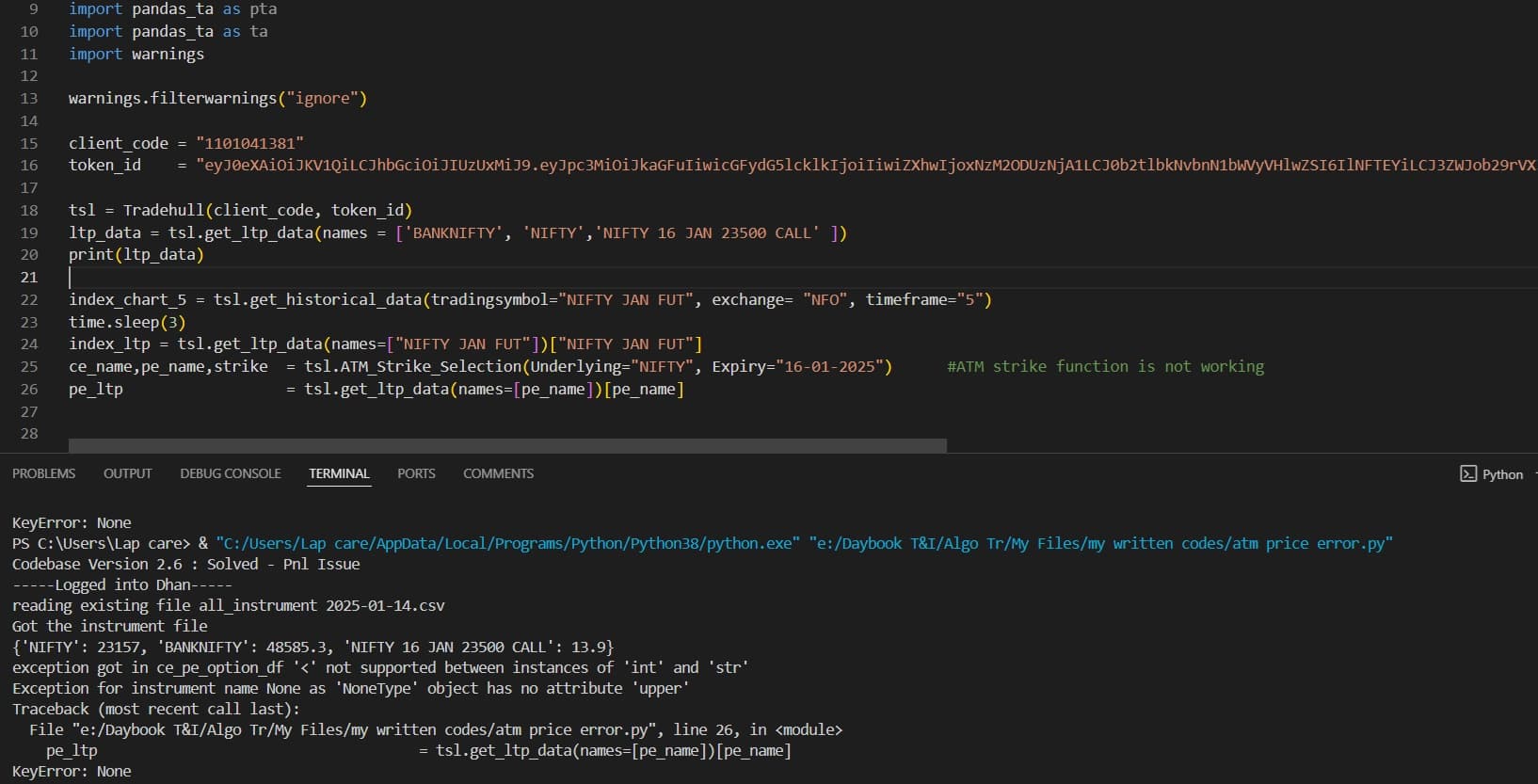

Still getting errors, Not sure if I am missing something

import pdb

import time

import datetime

import traceback

from Dhan_Tradehull_V2 import Tradehull

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as pta

import pandas_ta as ta

import warnings

warnings.filterwarnings("ignore")

client_code = "......"

token_id = "........"

tsl = Tradehull(client_code, token_id)

ltp_data = tsl.get_ltp_data(names = ['BANKNIFTY', 'NIFTY','NIFTY 16 JAN 23500 CALL' ])

print(ltp_data)

index_chart_5 = tsl.get_historical_data(tradingsymbol="NIFTY JAN FUT", exchange= "NFO", timeframe="5")

time.sleep(3)

index_ltp = tsl.get_ltp_data(names=["NIFTY JAN FUT"])["NIFTY JAN FUT"]

ce_name,pe_name,strike = tsl.ATM_Strike_Selection(Underlying="NIFTY", Expiry="16-01-2025") #ATM strike function is not working

pe_ltp = tsl.get_ltp_data(names=[pe_name])[pe_name]

Send a detailed explanation of the rulesets.

Hi @Qaisar

Send a detailed explanation of the rulesets.

Send a detailed explanation of the rulesets.