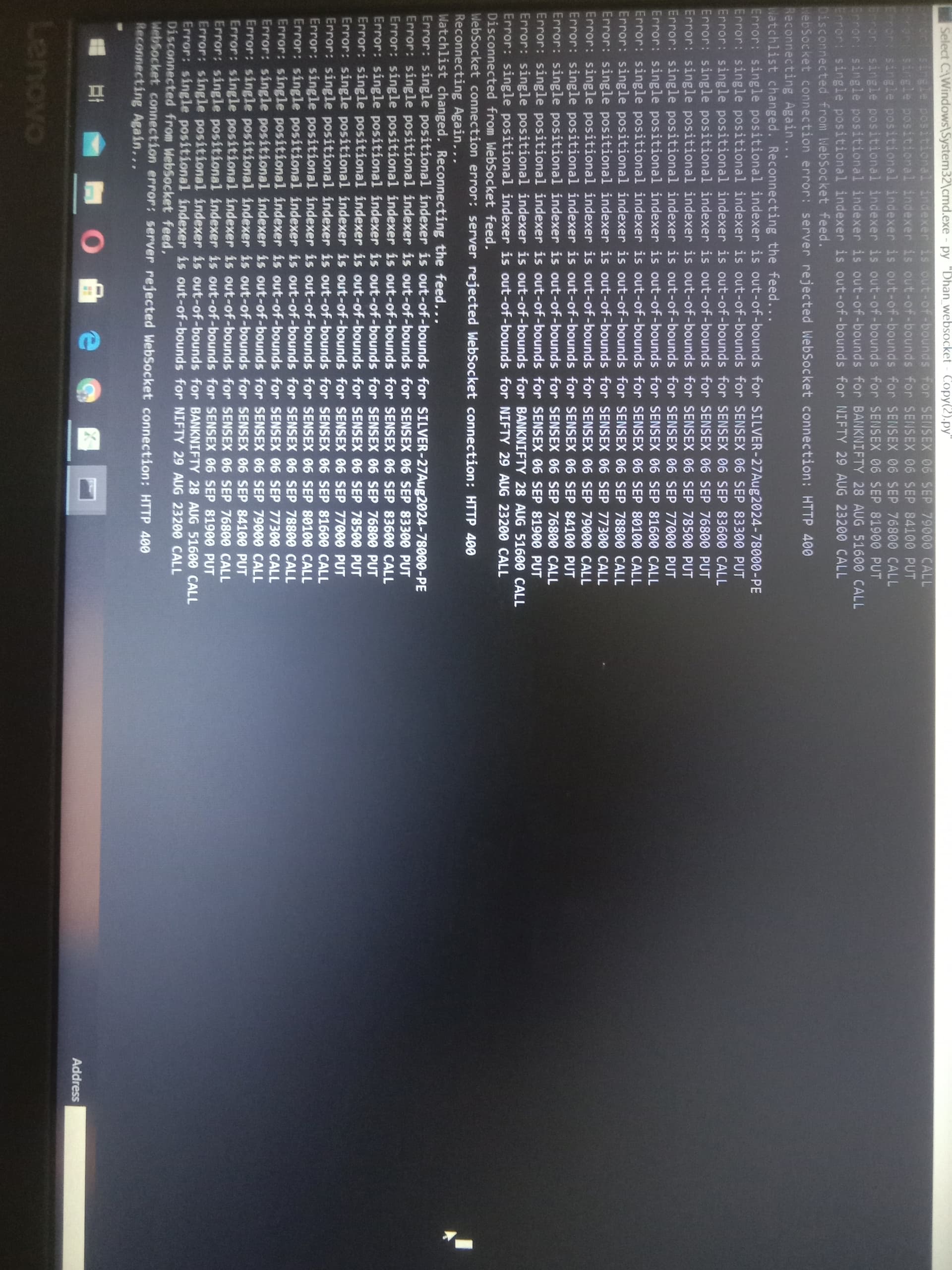

sir i am getting the error in the screenshot submitted with the following code. kindly check @Tradehull_Imran

import datetime

import warnings

from dhanhq import marketfeed

import xlwings as xw

import pandas as pd

import time

import os

warnings.filterwarnings(“ignore”)

def get_instrument_file():

global instrument_df

current_date = time.strftime(“%Y-%m-%d”)

expected_file = 'all_instrument ’ + str(current_date) + ‘.csv’

for item in os.listdir(“Dependencies”):

path = os.path.join(item)

if (item.startswith('all_instrument')) and (current_date not in item.split(" ")[1]):

if os.path.isfile("Dependencies\\" + path):

os.remove("Dependencies\\" + path)

if expected_file in os.listdir("Dependencies"):

try:

print(f"Reading existing file {expected_file}")

instrument_df = pd.read_csv("Dependencies\\" + expected_file, low_memory=False)

except Exception as e:

print("This BOT Is Instrument file is not generated completely, Picking New File from Dhan Again")

instrument_df = pd.read_csv("https://images.dhan.co/api-data/api-scrip-master.csv", low_memory=False)

instrument_df.to_csv("Dependencies\\" + expected_file)

else:

# This will fetch instrument_df file from Dhan

print("This BOT Is Picking New File From Dhan")

instrument_df = pd.read_csv("https://images.dhan.co/api-data/api-scrip-master.csv", low_memory=False)

instrument_df.to_csv("Dependencies\\" + expected_file)

return instrument_df

Excel sheet setup

wb = xw.Book(“Websocket.xlsx”)

sheet = wb.sheets[‘LTP’]

client_id = “1105938434”

access_token = "ACCESS TOKEN HIDDEN

"

Fetch the instrument file

current_date = time.strftime(“%Y-%m-%d”)

expected_file = 'all_instrument ’ + str(current_date) + ‘.csv’

global instrument_df, old_instruments

old_instruments = list()

instrument_df = get_instrument_file()

def create_instruments(watchlist, stock_exchange):

rows = dict()

row = 1

instruments = list()

instrument_exchange = {‘NSE’: “NSE”, ‘BSE’: “BSE”, ‘NFO’: ‘NSE’, ‘BFO’: ‘BSE’, ‘MCX’: ‘MCX’, ‘CUR’: ‘NSE’, ‘BSE_IDX’: ‘BSE’, ‘NSE_IDX’: ‘NSE’}

exchange_id = {‘NSE’: marketfeed.NSE, ‘BSE’: marketfeed.BSE, ‘MCX’: marketfeed.MCX, ‘NFO’: marketfeed.NSE_FNO, ‘BFO’: marketfeed.BSE_FNO, ‘IDX’: marketfeed.IDX, ‘BSE_IDX’: marketfeed.IDX, ‘NSE_IDX’: marketfeed.IDX}

for tradingsymbol in watchlist:

try:

row += 1

exchange_ = stock_exchange[tradingsymbol]

exchange = instrument_exchange[exchange_]

security_id = instrument_df[

((instrument_df['SEM_TRADING_SYMBOL'] == tradingsymbol) | (instrument_df['SEM_CUSTOM_SYMBOL'] == tradingsymbol)) &

(instrument_df['SEM_EXM_EXCH_ID'] == instrument_exchange[exchange])

].iloc[-1]['SEM_SMST_SECURITY_ID']

exchange_segment = exchange_id[exchange_]

# Subscribe to Quote mode for now, can be changed to Ticker or Depth as needed

instruments.append((exchange_segment, str(security_id), marketfeed.Quote))

rows[security_id] = row

except Exception as e:

print(f"Error: {e} for {tradingsymbol}")

continue

return instruments, rows

def run_feed(client_id, access_token, instruments):

try:

# Initialize DhanFeed

data = marketfeed.DhanFeed(client_id, access_token, instruments)

previous_watchlist =

rows = {}

old_instruments = instruments

while True:

# Check for updated watchlist

last_row_col1 = sheet.range('A1').end('down').row

last_row_col2 = sheet.range('B1').end('down').row

row = max(last_row_col1, last_row_col2)

data_frame = sheet.range('A1').expand().options(pd.DataFrame, header=1, index=False).value

stock_exchange = sheet.range(f'A2:B{row}').options(dict).value

watchlist = data_frame['Script Name'].to_list()

# If watchlist has changed, update the feed

if watchlist != previous_watchlist:

print("Watchlist changed. Reconnecting the feed...")

# Create new instruments and row mappings before disconnecting

new_instruments, new_rows = create_instruments(watchlist, stock_exchange)

# Disconnect the current connection

data.disconnect()

print("Disconnected from WebSocket feed.")

# Update previous watchlist and rows before reconnecting

previous_watchlist = watchlist

rows = new_rows

old_instruments = new_instruments

# Reconnect with the updated instruments

data = marketfeed.DhanFeed(client_id, access_token, new_instruments)

data.run_forever()

# Start receiving data

response = data.get_data()

if response:

print(f"{datetime.datetime.now().time()}: LTP Received")

if 'LTP' in response.keys():

df = pd.DataFrame(response, index=[0])

security_id = response['security_id']

row = rows.get(int(security_id), None)

if row:

df = df[['LTP', 'avg_price', 'volume', 'total_sell_quantity', 'open', 'close', 'high', 'low']]

sheet.range(f'C{row}').value = df.values.tolist()

except Exception as e:

print(f"WebSocket connection error: {e}")

print("Reconnecting Again...")

# time.sleep(5) # Short delay before reconnecting

run_feed(client_id, access_token, instruments) # Retry the connection

def main_loop():

# Fetch initial instrument data and start the feed

last_row_col1 = sheet.range(‘A1’).end(‘down’).row

last_row_col2 = sheet.range(‘B1’).end(‘down’).row

row = max(last_row_col1, last_row_col2)

data_frame = sheet.range(‘A1’).expand().options(pd.DataFrame, header=1, index=False).value

stock_exchange = sheet.range(f’A2:B{row}').options(dict).value

watchlist = data_frame[‘Script Name’].to_list()

instruments, rows = create_instruments(watchlist, stock_exchange)

run_feed(client_id, access_token, instruments)

if name == “main”:

main_loop()