Hello @Tradehull_Imran

Sir If if people_intrested > required_people_intrested:

print(“BUILD LIVE ALGO”)

Thanks

Hello @Tradehull_Imran

Sir If if people_intrested > required_people_intrested:

print(“BUILD LIVE ALGO”)

Thanks

Hi @Tradehull_Imran

The “required_people_interested” has to be >16. If yes, then you will…

“red_circle GO LIVE SESSION ON YOUTUBE”

"red_circle BUILD ALGO LIVE "

“red_circle LIVE QUESTIONS AND ANSWER IMPLEMENTATION”

However, I would suggest one small change…

If interest_level_of_current_participants >100%:

print(“@Tradehull_Imran may make an exception to the above rule and still do a live session on youtube/build algo live/live q&a”)

![]()

![]()

Hi @Tradehull_Imran, Thank you for your help. I’ll check again today.

Thanks

Thank you for your kind words @Tradehull_Imran. Coming from an Algo trading expert like you, Its a big motivation for a novice like me. ![]()

![]()

@Tradehull_Imran Sir really need your help, what i am doing wrong here …i am able to place order in equity but not for options …why?

Hi @Kishore007

Dhan_Tradehull_V2 has no function for get_position

now if you want to check if you have bought/sold the position in this case we need to implement trade_info dictionary

see : https://youtu.be/wlQWSLzp_UI?si=LC7lZmWat_K-3JdI&t=2685

I am adding pseudocode for it, do make the changes accordingly.

import pdb

import time

import datetime

import traceback

from Dhan_Tradehull_V2 import Tradehull

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as pta

import pandas_ta as ta

import warnings

warnings.filterwarnings("ignore")

#-----------------------------------------------------------------------------------

client_code = "11"

token_id = "11"

tsl = Tradehull(client_code,token_id)

#----------------------------------------------------------------------------------

available_balance = tsl.get_balance()

leveraged_margin = available_balance*5

max_trades = 20

per_trade_margin = (leveraged_margin/max_trades)

max_loss = available_balance * -0.09 # max loss of 9%

#-----------------------------------------------------------------------------------------

watchlist = ['GOLDPETAL DEC FUT']

traded_wathclist = []

#-----------------------------------------------------------------------------------------------------

trade_info = {"stock_name":None, "qty":None, "entry_orderid":None, "direction":None}

while True:

live_pnl = tsl.get_live_pnl()

current_time = datetime.datetime.now().time()

if current_time < datetime.time(9, 18):

print("Wait for market to start", current_time)

time.sleep(1)

continue

if (current_time > datetime.time(23, 15)) or (live_pnl < max_loss):

# I_want_to_trade_no_more = tsl.kill_switch('ON')

order_details = tsl.cancel_all_orders()

print("Market is over, Bye see you tomorrow", current_time)

break

for stock_name in watchlist:

time.sleep(2)

print(f"Scanning {stock_name}")

# Conditions that are on 1 minute timeframe -------------------------------------------

chart_1 = tsl.get_historical_data(tradingsymbol=stock_name, exchange='MCX', timeframe="1")

pervious_candle = chart_1.iloc[-2]

no_repeat_order = stock_name not in traded_wathclist

# rsi ------------------------ apply indicators--------------------------------------

# Buy when rsi crosses above 55 and sell when rsi crosses below 45

# Ensure chart_1 has sufficient rows

if len(chart_1) <= 15:

print(f"Not enough data for {stock_name}. Skipping.")

continue

# Calculate RSI and drop NaN values

chart_1['rsi'] = talib.RSI(chart_1['close'], timeperiod=14)

chart_1['prev_rsi'] = chart_1['rsi'].shift(1)

chart_1.dropna(subset=['rsi', 'prev_rsi'], inplace=True)

# Add crossover columns

chart_1['uptrend_cross'] = (chart_1['prev_rsi'] <= 55) & (chart_1['rsi'] > 55)

chart_1['downtrend_cross'] = (chart_1['prev_rsi'] >= 45) & (chart_1['rsi'] < 45)

# Ensure the columns exist in the completed candle

cc_1 = chart_1.iloc[-2] # Second-to-last row

if 'uptrend_cross' not in cc_1 or 'downtrend_cross' not in cc_1:

print(f"Missing crossover columns for {stock_name}. Skipping.")

continue

# Access crossover values

uptrend_1 = cc_1['uptrend_cross']

downtrend_1 = cc_1['downtrend_cross']

print(f"Uptrend: {uptrend_1}, Downtrend: {downtrend_1}")

# Supertrend for Exit from open position -------------------------- apply indicators-----------------------------------

indi = ta.supertrend(chart_1['high'], chart_1['low'], chart_1['close'], 10, 1)

chart_1 = pd.concat([chart_1, indi], axis=1, join='inner')

cc_1 = chart_1.iloc[-2] #pandas completed candle of 1 min timeframe

exit_sell = cc_1['close'] > cc_1['SUPERT_10_1.0']

exit_buy = cc_1['close'] < cc_1['SUPERT_10_1.0']

# BUY conditions ------------------------------------------------------------------------------

breakout_b1 = ((pervious_candle['close'] - pervious_candle['open']) / pervious_candle['open']) * 100 # percentage change

breakout_b2 = pervious_candle['volume'] > 0.2 * chart_1['volume'].mean()

if uptrend_1 and breakout_b2 and (0.01 <= breakout_b1 <= 0.4) and no_repeat_order:

print(stock_name, "is in uptrend, Buy this script")

lot_size = tsl.get_lot_size(stock_name)

# Place buy order-------------------------------------------------------------------------

entry_orderid = tsl.order_placement(stock_name, 'MCX', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded_wathclist.append(stock_name)

trade_info['stock_name'] = stock_name

trade_info['qty'] = lot_size

trade_info['entry_orderid'] = entry_orderid

trade_info['direction'] = "BUY"

# SELL conditions -----------------------------------------------------------------------------

breakout_s1 = ((pervious_candle['close'] - pervious_candle['open']) / pervious_candle['open']) * 100 # percentage change

breakout_s2 = pervious_candle['volume'] > 0.2 * chart_1['volume'].mean()

if downtrend_1 and breakout_s2 and (-0.4 <= breakout_s1 <= -0.01) and no_repeat_order:

print(stock_name, "is in downtrend, Sell this script")

lot_size = tsl.get_lot_size(stock_name)

# Place sell order-------------------------------------------------------------------------

entry_orderid = tsl.order_placement(stock_name, 'MCX', lot_size, 0, 0, 'MARKET', 'SELL', 'MIS')

traded_wathclist.append(stock_name)

# Exit conditions based on Supertrend indicator----------------------------------------------------

for stock_name in traded_wathclist:

time.sleep(2)

print(f"Checking exit conditions for {stock_name}")

# Fetch updated 1-minute chart

chart_1 = tsl.get_historical_data(tradingsymbol=stock_name, exchange='MCX', timeframe="1")

# Apply Supertrend indicator again

indi = ta.supertrend(chart_1['high'], chart_1['low'], chart_1['close'], 10, 1)

chart_1 = pd.concat([chart_1, indi], axis=1, join='inner')

cc_1 = chart_1.iloc[-2] # Get the completed candle

# Exit conditions

exit_sell = cc_1['close'] > cc_1['SUPERT_10_1.0']

exit_buy = cc_1['close'] < cc_1['SUPERT_10_1.0']

# Check for existing positions to square off

position = trade_info['direction']

if position == 'BUY' and exit_buy:

print(f"Exiting BUY position for {stock_name}")

exit_orderid = tsl.order_placement(stock_name, 'MCX', position['lot_size'], 0, 0, 'MARKET', 'SELL', 'MIS')

traded_wathclist.remove(stock_name)

elif position == 'SELL' and exit_sell:

print(f"Exiting SELL position for {stock_name}")

exit_orderid = tsl.order_placement(stock_name, 'MCX', position['lot_size'], 0, 0, 'MARKET', 'BUY', 'MIS')

traded_wathclist.remove(stock_name)

But trade_info will only work for a single script,

as of now I have not taught how to manage multiple positions with all the details.

I will take this topic in next live lecture This week.

There were many upgraded along the way , do check below sequence for practice

use below code for order placement into options

tsl.order_placement(ce_name,'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

for video tutorial see : https://youtu.be/wlQWSLzp_UI?si=ZF5z38v2pnl_S2Xj&t=2472

Thankyou sir,

Awaiting for live session, sir..

BANKNIFTY DEC FUT Buy CALL

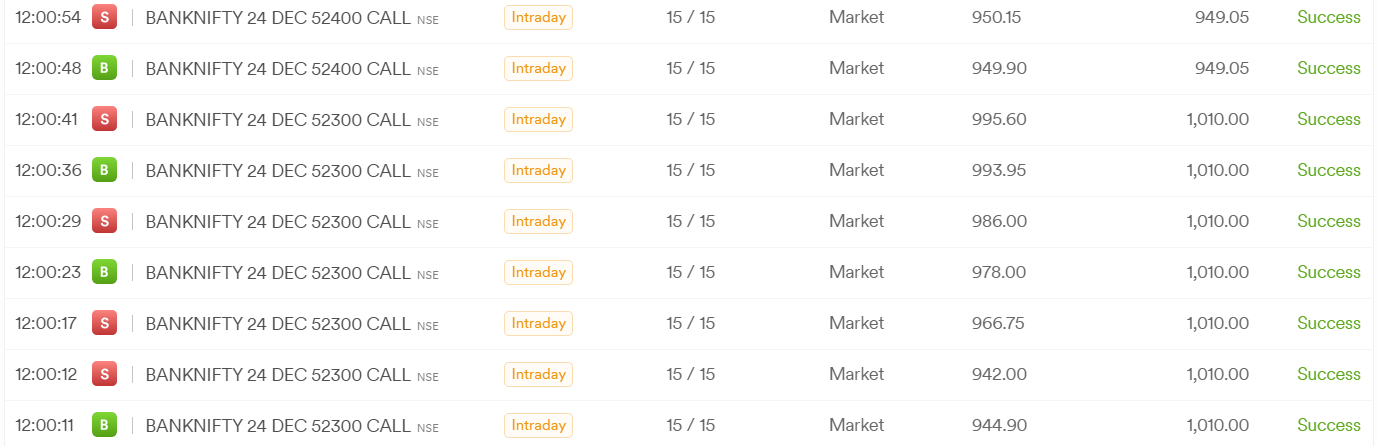

Order Exited {‘options_name’: ‘BANKNIFTY 24 DEC 52300 CALL’, ‘qty’: 15, ‘sl’: 944.9, ‘CE_PE’: ‘CE’, ‘entry_price’: 944.9, ‘Trailed’: ‘yes_I_have_trailed’, ‘entry_orderid’: ‘42241127396413’}

BUY NIFTY DEC FUT 12:00:11.177718 False True False cc_1 2024-11-27 12:00:00+05:30

SELL NIFTY DEC FUT 12:00:11.177718 False True False cc_1 2024-11-27 12:00:00+05:30

Order Exited {‘options_name’: ‘BANKNIFTY 24 DEC 52300 CALL’, ‘qty’: 15, ‘sl’: 944.9, ‘CE_PE’: ‘CE’, ‘entry_price’: 944.9, ‘Trailed’: ‘yes_I_have_trailed’, ‘entry_orderid’: ‘42241127396413’}

BUY BANKNIFTY DEC FUT 12:00:11.177718 True True True cc_1 2024-11-27 12:00:00+05:30

SELL BANKNIFTY DEC FUT 12:00:11.177718 False True False cc_1 2024-11-27 12:00:00+05:30

BANKNIFTY DEC FUT Buy CALL

BUY NIFTY DEC FUT 12:00:23.511704 False True False cc_1 2024-11-27 12:00:00+05:30

SELL NIFTY DEC FUT 12:00:23.511704 False True False cc_1 2024-11-27 12:00:00+05:30

Order Exited {‘options_name’: ‘BANKNIFTY 24 DEC 52300 CALL’, ‘qty’: 15, ‘sl’: 52422.25, ‘CE_PE’: ‘CE’, ‘entry_price’: 978.0, ‘Trailed’: ‘yes_I_have_trailed’, ‘entry_orderid’: ‘22241127378613’}

BUY BANKNIFTY DEC FUT 12:00:23.511704 True True True cc_1 2024-11-27 12:00:00+05:30

SELL BANKNIFTY DEC FUT 12:00:23.511704 False True False cc_1 2024-11-27 12:00:00+05:30

BANKNIFTY DEC FUT Buy CALL

BUY NIFTY DEC FUT 12:00:35.661303 False True False cc_1 2024-11-27 12:00:00+05:30

SELL NIFTY DEC FUT 12:00:35.661303 False True False cc_1 2024-11-27 12:00:00+05:30

Order Exited {‘options_name’: ‘BANKNIFTY 24 DEC 52300 CALL’, ‘qty’: 15, ‘sl’: 52422.25, ‘CE_PE’: ‘CE’, ‘entry_price’: 993.95, ‘Trailed’: ‘yes_I_have_trailed’, ‘entry_orderid’: ‘22241127380013’}

BUY BANKNIFTY DEC FUT 12:00:35.661303 True True True cc_1 2024-11-27 12:00:00+05:30

SELL BANKNIFTY DEC FUT 12:00:35.661303 False True False cc_1 2024-11-27 12:00:00+05:30

BANKNIFTY DEC FUT Buy CALL

BUY NIFTY DEC FUT 12:00:48.302710 False True False cc_1 2024-11-27 12:00:00+05:30

SELL NIFTY DEC FUT 12:00:48.302710 False True False cc_1 2024-11-27 12:00:00+05:30

Order Exited {‘options_name’: ‘BANKNIFTY 24 DEC 52400 CALL’, ‘qty’: 15, ‘sl’: 52422.25, ‘CE_PE’: ‘CE’, ‘entry_price’: 949.9, ‘Trailed’: ‘yes_I_have_trailed’, ‘entry_orderid’: ‘42241127399413’}

https://drive.google.com/file/d/1SOZWxIGv5niXVr2fwxGL_5YmbPQRAY77/view?usp=sharing

hi,

get_historical_data method is not working from Dhan_tradehull.py, i have passed the following parameters from my temp.py

import talib

import pdb

from Dhan_Tradehull import Tradehull

import pandas as pd

tsl = Tradehull(client_code,token_id) # tradehull_support_library

previous_hist_data = tsl.get_historical_data(‘HDFCBANK’,‘NSE’,12)

print(previous_hist_data)

OHLC Response: {‘status’: ‘failure’, ‘remarks’: “expiry_code value must be [‘0’,‘1’,‘2’,‘3’]”, ‘data’: ‘’}

Invalid OHLC data or missing.

Please help. how can it we resolved

Exception at calling ltp as {‘status’: ‘failure’, ‘remarks’: {‘error_code’: None, ‘error_type’: None, ‘error_message’: None}, ‘data’: {‘data’: {‘805’: ‘Too many requests. Further requests may result in the user being blocked.’}, ‘status’: ‘failed’}}

Traceback (most recent call last):

File “/Users/parveenchugh/latest/strategy1.py”, line 44, in

current_price = ltp_data[‘NIFTY 28 NOV 24300 PUT’]

~~~~~~~~^^^^^^^^^^^^^^^^^^^^^^^^^^

KeyError: ‘NIFTY 28 NOV 24300 PUT’

Do find updated code, I have made changes in buy side

Added up4 for entry

up4 = trade_info['traded'] is None

For trailing the code says

price_has_moved_20_pct = index_ltp_value > (trade_info['entry_price'] * 1.2)

Notice your entry is in options , so entry price is around Rs 993.95 and index ltp is around 52350 # Note I have taken example rates

so price_has_moved_20_pct condition equates to = (52350 > (993.95*1.2)) which will always be True

when the condition becomes True, below code sets stoploss to entry price (993.95)

if price_has_moved_20_pct and position_has_not_been_trailed:

trade_info['sl'] = trade_info['entry_price']

and the SL hit condition becomes True, because code is comparing index_ltp to options ltp, which is always True

sl_hit = index_ltp_value < trade_info['sl']

tg_hit = index_ltp_value < cc5_2['SUPERT_10_3.0']

Which leads to immdeiate SL exit

Important:

As of now work only with single script and trade_info,

as of now I have not taught how to manage multiple positions with all the details.

I will take this topic in next live lecture This week.

Also till then do work with a test account

Also we can review this code in live lecture also,

CODE

import pdb

import traceback

import time

import datetime

from Dhan_Tradehull_V2 import Tradehull

import pandas as pd

from pprint import pprint

import pandas_ta as ta

import talib

import warnings

warnings.filterwarnings("ignore")

# ---------------for Dhan login ----------------

client_code = ""

token_id = ""

tsl = Tradehull(client_code, token_id)

available_balance = tsl.get_balance()

print("Available Balance:", available_balance)

# Define the symbols to trade

symbols = ['NIFTY DEC FUT']

traded = "no"

trade_info = {"options_name": None, "qty": None, "sl": None, "CE_PE": None, "entry_price": None, "Trailed": None, "entry_orderid": None, "traded":None}

while True:

current_time = datetime.datetime.now().time()

if current_time < datetime.time(9, 20):

print("Wait for market to start", current_time)

continue

if current_time > datetime.time(23, 25):

print("Market is over, Bye Bye see you tomorrow", current_time)

break

for index_name in symbols:

index_chart = tsl.get_historical_data(tradingsymbol=index_name, exchange='NFO', timeframe="15")

time.sleep(3)

index_chart_5 = tsl.get_historical_data(tradingsymbol=index_name, exchange='NFO', timeframe="5")

index_ltp = tsl.get_ltp_data(names=[index_name])

if index_chart.empty or index_chart_5.empty:

time.sleep(60)

continue

index_chart['rsi'] = talib.RSI(index_chart['close'], timeperiod=14)

supertrend = ta.supertrend(index_chart_5['high'], index_chart_5['low'], index_chart_5['close'], 10, 3)

index_chart_5 = pd.concat([index_chart_5, supertrend], axis=1, join='inner')

cc_1 = index_chart.iloc[-1]

cc_2 = index_chart.iloc[-2]

cc_3 = index_chart.iloc[-3]

cc5_2 = index_chart_5.iloc[-2]

# ---------------------------- BUY ENTRY CONDITIONS ----------------------------

up1 = cc_2['rsi'] > 60

up2 = cc_3['rsi'] < 60

up3 = cc_2['high'] < cc_1['close']

up4 = trade_info['traded'] is None

print(f"BUY {index_name}\t{current_time}\t{up1}\t{up2}\t{up3}\tcc_1 {str(cc_1['timestamp'])}")

# ---------------------------- SELL ENTRY CONDITIONS ----------------------------

dt1 = cc_2['rsi'] < 40

dt2 = cc_3['rsi'] > 40

dt3 = cc_2['low'] > cc_1['close']

dt4 = ???

print(f"SELL {index_name}\t{current_time}\t{dt1}\t{dt2}\t{dt3}\tcc_1 {str(cc_1['timestamp'])}\n")

expiry = '24-12-2024' if 'BANKNIFTY' in index_name else '26-12-2024'

if up1 and up2 and up3 and up4:

print(index_name, "Buy CALL")

ce_name, pe_name, strike = tsl.ATM_Strike_Selection(Underlying=index_name.split()[0], Expiry=expiry)

lot_size = tsl.get_lot_size(ce_name) * 1

entry_orderid = tsl.order_placement(ce_name, 'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info.update({"options_name": ce_name, "qty": lot_size, "sl": cc_2['low'], "CE_PE": "CE", "entry_orderid": entry_orderid, "traded":"yes_I_have_entered_position"})

time.sleep(1)

trade_info['entry_price'] = tsl.get_executed_price(orderid=trade_info['entry_orderid'])

if dt1 and dt2 and dt3:

print(index_name, "Buy PUT")

ce_name, pe_name, strike = tsl.ATM_Strike_Selection(Underlying=index_name.split()[0], Expiry=expiry)

lot_size = tsl.get_lot_size(pe_name) * 1

entry_orderid = tsl.order_placement(pe_name, 'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info.update({"options_name": pe_name, "qty": lot_size, "sl": cc_2['high'], "CE_PE": "PE", "entry_orderid": entry_orderid})

time.sleep(1)

trade_info['entry_price'] = tsl.get_executed_price(orderid=trade_info['entry_orderid'])

if traded == "yes":

long_position = trade_info['CE_PE'] == "CE"

short_position = trade_info['CE_PE'] == "PE"

# Check if LTP is a dictionary or an integer and extract the correct value

index_ltp_value = index_ltp.get(index_name) if isinstance(index_ltp, dict) else index_ltp

if index_ltp_value is None:

print(f"Failed to get LTP for {index_name}")

continue

# Ensure comparison is with the correct type

price_has_moved_20_pct = index_ltp_value > (trade_info['entry_price'] * 1.2)

position_has_not_been_trailed = trade_info['Trailed'] is None

if price_has_moved_20_pct and position_has_not_been_trailed:

trade_info['sl'] = trade_info['entry_price']

trade_info['Trailed'] = "yes_I_have_trailed"

sl_hit = index_ltp_value < trade_info['sl']

tg_hit = index_ltp_value < cc5_2['SUPERT_10_3.0']

if sl_hit or tg_hit:

print("Order Exited", trade_info)

exit_orderid = tsl.order_placement(trade_info['options_name'], 'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

# if you want re-entry to happen, unblock below code

# trade_info = {"options_name": None, "qty": None, "sl": None, "CE_PE": None, "entry_price": None, "Trailed": None, "entry_orderid": None, "traded":None}

check this link : https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718/1065?u=tradehull_imran

The code was calling data too fast

See this link : https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718/860?u=tradehull_imran

Hi

@Tradehull_Imran

I am glad and appreciate for your back-to-back support

Thank You Very much

Thanks sir, now change time.sleep(5) for slow data

class DhanHQMock:

pass

def get_live_data(url):

return 120

api = DhanHQMock()

required_people_intrested = (100 // 6)

url = “https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718”

people_intrested = get_live_data(url)

if people_intrested > required_people_intrested:

print(“![]() BUILD ALGO LIVE SESSION ON YOUTUBE”)

BUILD ALGO LIVE SESSION ON YOUTUBE”)

print(“![]() LIVE QUESTIONS AND ANSWER IMPLEMENTATION”)

LIVE QUESTIONS AND ANSWER IMPLEMENTATION”)

else:

print(“Wait ![]() ”) i mean to say supper interested to continue learning with @Tradehull_Imran

”) i mean to say supper interested to continue learning with @Tradehull_Imran

There’s only one video that remains in this series! ![]()

Are you all excited for it ?

Sir, I’m excited for the remaining video and looking forward to the next one more series.This will keep our community members engaged and help them gain more expertise while fostering a user-friendly experience through continuous interaction. Request keep the same teacher for next series.