Hi ,

i did take latest Session 8 file. but still getting error in placement of order.

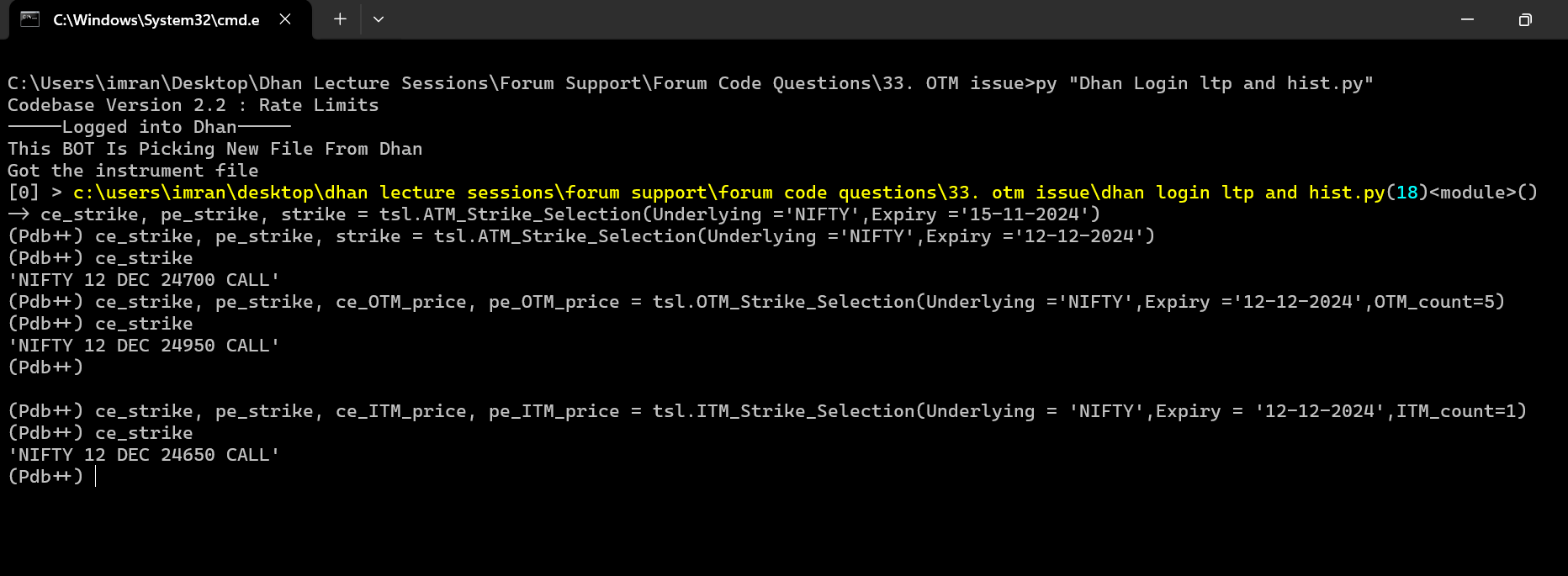

KeyError: ‘orderId’

Session 8 latest files but error in order placement

What is this Error:

step Value DF is not generated due to Error from NSE India site: invalid syntax (init .py, line 1187)

Hi @virender_singh

KeyError: ‘orderId’ This error is okey,

since now the market is closed, its not able to place order,

Hi @Zee2Zahid

step value is the difference between the options strikes.

sometimes it gives error in fetching all the steps value for fno scripts, so that the error

we will be removing dependency on NSE for step value in upcoming Dhan_Tradehull_V3.

1 Like

babji3

December 6, 2024, 5:45pm

1436

How to fix rate limit sir?

WebSocket connection error: [SSL: CERTIFICATE_VERIFY_FAILED] certificate verify failed: unable to get local issuer certificate (_ssl.c:1108)

please provide solution

Hi

C:\RAMESH\0Algo with Python Coding\6. Session6- 1st Live Algo\6. Session6- 1st Live Algo\1st live Algo>py “Dhan_codebase usage.py”#pandas

Hello @Tradehull_Imran Sir

Hi @SWARUP_NANDI

we get SSL issue while implementing WebSocket to get ltp,

see : https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718/952?u=tradehull_imran

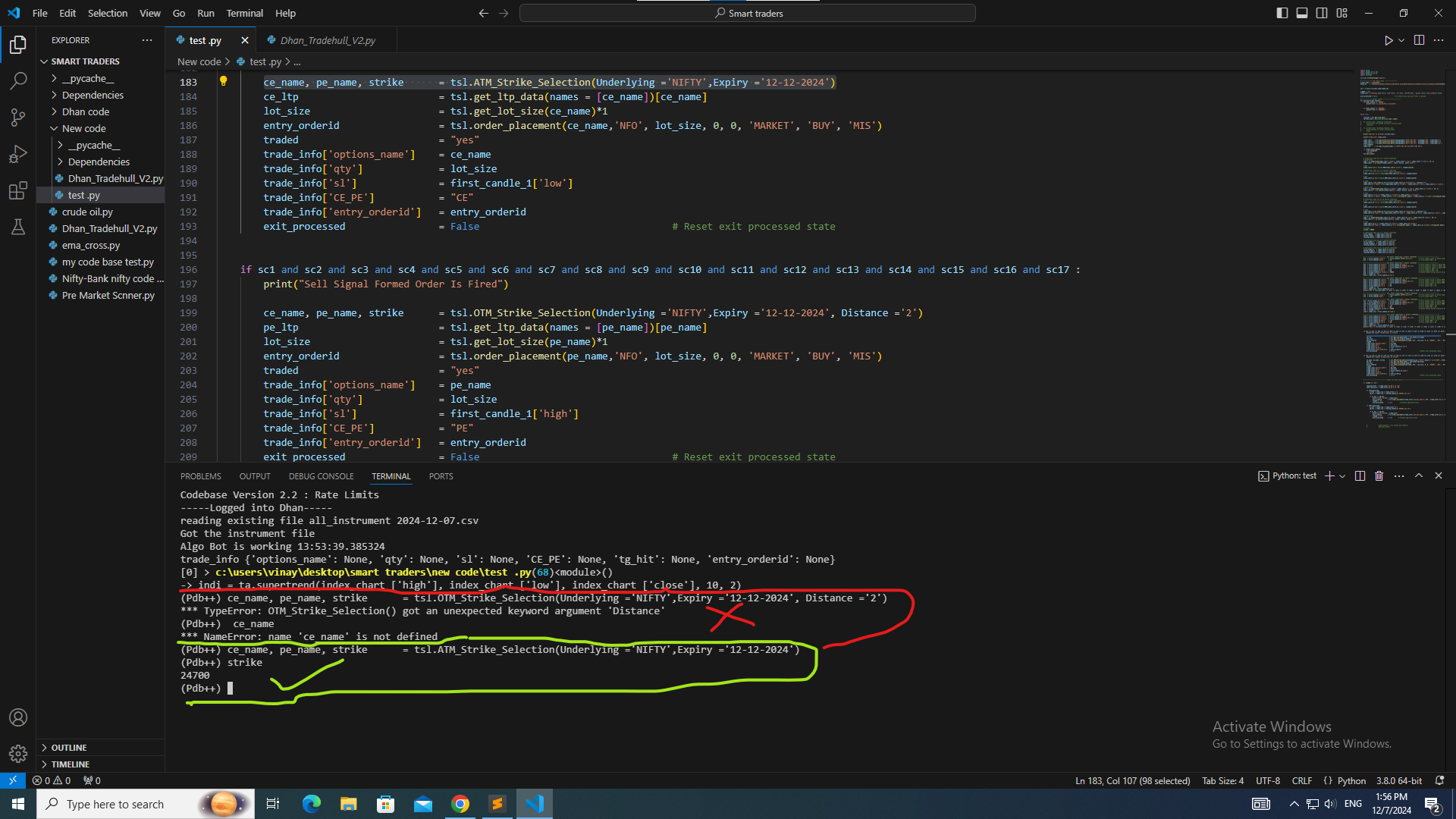

Hi @vinay_kumaar

use this code

ce_strike, pe_strike, strike = tsl.ATM_Strike_Selection(Underlying ='NIFTY',Expiry ='12-12-2024')

ce_strike, pe_strike, ce_OTM_price, pe_OTM_price = tsl.OTM_Strike_Selection(Underlying ='NIFTY',Expiry ='12-12-2024',OTM_count=5)

ce_strike, pe_strike, ce_ITM_price, pe_ITM_price = tsl.ITM_Strike_Selection(Underlying = 'NIFTY',Expiry = '12-12-2024',ITM_count=1)

Hi, @Tradehull_Imran , sir..

In next live session please cover this topic, sir..

How to manage multiple open position and tp/sl orders with trade_info dictionary

And in Dhan_Tradehull_V3 , please add function for get_position

1 Like

can we fetch intraday data from api of within specific time period on the data, i don’t to give unnecessory load on API and on my system, this is for purpose to get increment data only beween time period in minutes not in dates.

example :

Very good evening sir,

I would like to understand the purpose of using ‘f’ in the following code line sir?

print(f"for {script_name} the ltp is {ltp}")

VBR Prasad

@Tradehull_Imran Sir, Have u checked it

Hi @Vinod_Kumar1

If we call only specific data in historical api, that will be still counted as 1 API call.

Also , if the strategy includes indicator then trimmed data will not give correct indicator values.

let me know a specific use can, so we can explore more on this.