Hi, @Tradehull_Imran , Sir,

What is the Code for Range Candle Break Out, for example from 10.10 am to 10.40 am high/low break out. ![]()

Hi, @Tradehull_Imran , Sir,

What is the Code for Range Candle Break Out, for example from 10.10 am to 10.40 am high/low break out. ![]()

Hi Imran - how many codebase zip files you have made available so far out of 10 sessions? not able to locate where they all are.

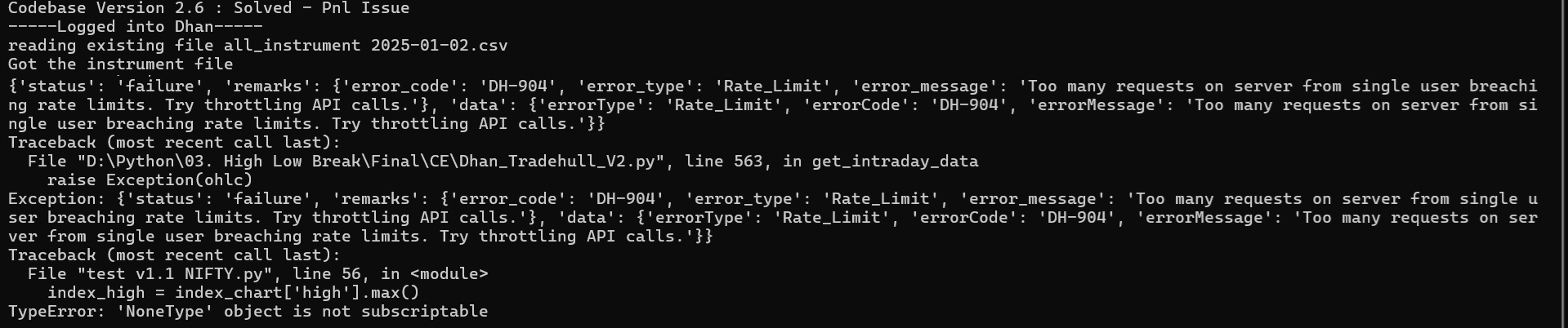

@Tradehull_Imran Sir, I encountered this error. How can I resolve it?

Thanks it is working now.

Latest updated Code Base :- https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718/1991?u=kishore007

@Kanha_Meher , It is Rate Limit Issue, Run the Algo Tomorrow..

For more information :- https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718/1557?u=kishore007

Hi, tradehall@imran,

chart_5 = tsl.get_historical_data(tradingsymbol = stock_name, exchange = ‘NSE’,timeframe=“5”) # Upgraded 5 minute chart according to Dhan_Tradehull_V2

cc_5 = chart_5.iloc[-1] # pandas

------ is [ -1] running candel or completed candel? pls. explain

@SUKANTA_MONDAL1 , [ -1] is running candle and [ -2] is completed candle..

traded_candle = ‘2025-1-2 10:10:00+05:30’

data_15 = tsl.get_historical_data(tradingsymbol=stock, exchange=‘NSE’, timeframe=“15”)

data_15 = data_15.set_index(data_15[‘timestamp’])

trade_candle = data_15.loc[traded_candle ] Use this code

@Tradehull_Imran Getting

tsl.ITM_Strike_Selection(NIFTY, 0, 3)

Getting Error at OTM strike Selection as Unable to find the ITM strike for the NIFTY

Exception in Getting OHLC data as 'NoneType' object has no attribute 'upper'

Its was working yesterday ![]()

Update: works for SENSEX

@Tradehull_Imran Is it possible to cache the instrument file locally after the initial download.

This BOT Is Picking New File From Dhan

Got the instrument file

Its taking around 20-30 seconds to process each time. Its kind a delaying the script development

Hi @Kishore007

Use this code for range breakout

chart = tsl.get_historical_data(tradingsymbol = 'NIFTY',exchange = 'INDEX',timeframe="5")

chart = chart.set_index(chart['timestamp'])

# get todays date in this format 2025-01-01

today_date = datetime.datetime.now().strftime("%Y-%m-%d")

start_time = today_date + " 09:20:00"

end_time = today_date + " 09:40:00"

range_chart = chart[start_time:end_time]

range_chart_high = range_chart['high']

range_chart_low = range_chart['low']

bc1 = ltp > range_chart_high

sc2 = ltp < range_chart_low

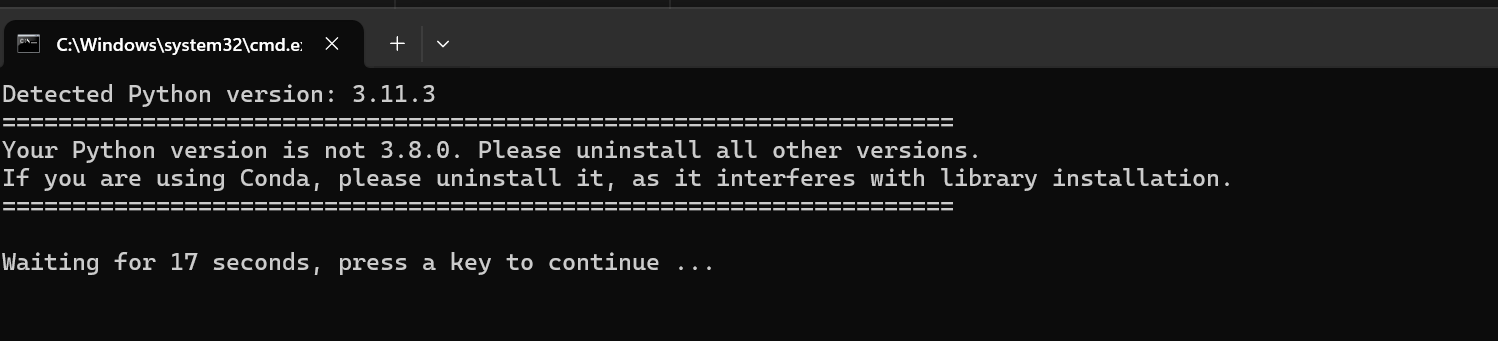

It seems that you are using python 3.11.3.

we need to use python 3.8.0 ..

so do uninstall python 3.11.3 and then retry the installation

we use older python versions, because they are supported by all the major libraries for algo trading.

Newer version may or may not support algo trading libraries, example : Ta-Lib

Instrument files gets a fresh download once per day,

so on the next run we just read it.. which may still take 20-30 seconds as the file is of 20 MB.

but yes, it feels too slow.. I will check on this.

@Tradehull_Imran

error

warnings.filterwarnings(“ignore”)

client_code = “”

token_id = “”

tsl = Tradehull(client_code,token_id)

available_balance = tsl.get_balance()

leveraged_margin = available_balance2

max_trades = 3

per_trade_margin = (leveraged_margin/max_trades)

max_loss = (available_balance1)/100*-1

traded = “no”

trade_info = {“options_name”:None, “qty”:None, “sl”:None, “CE_PE”:None}

while True:

live_pnl = tsl.get_live_pnl()

# current_time = datetime.datetime.now()

current_time = datetime.datetime.now().time() #time only

# print(current_time)

if current_time < datetime.time(9, 45, 00):

print (“Wait market to open”, current_time)

continue

if current_time> datetime.time(15, 15, 30) or(live_pnl <max_loss):

i_want_to_trade_no_more = tsl.kill_switch(‘ON’)

order_details = tsl.cancel_all_orders()

print (“Market is over or MAX LOSS, Bye for Now”, current_time)

break

print(“Algo is working”, current_time)

index_chart = tsl.get_historical_data(tradingsymbol='NIFTY JAN FUT', exchange='NFO', timeframe="5")

time.sleep(3)

index_ltp = tsl.get_ltp_data(names = ['NIFTY JAN FUT'])['NIFTY JAN FUT']

try:

index_chart = tsl.get_historical_data(tradingsymbol = 'NIFTY JAN FUT',exchange = 'NFO',timeframe="5")

except Exception as e:

print(e)

continue

# rsi ------------------------ apply indicators

index_chart['rsi'] = talib.RSI(index_chart['close'], timeperiod=14)

# vwap

index_chart.set_index(pd.DatetimeIndex(index_chart['timestamp']), inplace=True)

index_chart['vwap'] = pta.vwap(index_chart['high'] , index_chart['low'], index_chart['close'] , index_chart['volume'])

# Supertrend

indi = ta.supertrend(index_chart['high'], index_chart['low'], index_chart['close'], 10, 2)

index_chart = pd.concat([index_chart, indi], axis=1, join='inner')

# vwma

index_chart['pv'] = index_chart['close'] * index_chart['volume']

index_chart['vwma'] = index_chart['pv'].rolling(20).mean() / index_chart['volume'].rolling(20).mean()

# volume

volume = 50000

first_candle = index_chart.iloc[-3]

second_candle = index_chart.iloc[-2]

running_candle = index_chart.iloc[-1]

# ---------------------------- BUY ENTRY CONDITIONS ----------------------------

bc1 = first_candle['close'] > first_candle['vwap'] # First Candle close is above VWAP

bc2 = first_candle['close'] > first_candle['SUPERT_10_2.0'] # First Candle close is above Supertrend

bc3 = first_candle['close'] > first_candle['vwma'] # First Candle close is above VWMA

bc4 = first_candle['rsi'] < 80 # First candle RSI < 80

bc5 = second_candle['volume'] > 50000 # Second candle Volume should be greater than 50,000 for Nifty and above 125,000 for Bank Nifty

bc6 = traded == "no"

bc7 = index_ltp > first_candle['low']

print(f"BUY \t {current_time} \t {bc1} \t {bc2} \t {bc3} \t {bc4} \t {bc5} \t {bc7} \t first_candle {str(first_candle['timestamp'].time())}")

# ---------------------------- SELL ENTRY CONDITIONS ----------------------------

sc1 = first_candle['close'] < first_candle['vwap'] # First Candle close is below VWAP

sc2 = first_candle['close'] < first_candle['SUPERT_10_2.0'] # First Candle close is below Supertrend

sc3 = first_candle['close'] < first_candle['vwma'] # First Candle close is below VWMA

sc4 = first_candle['rsi'] > 20 # First candle RSI < 80

sc5 = second_candle['volume'] > 50000 # Second candle Volume should be greater than 50,000 for Nifty and above 125,000 for Bank Nifty

sc6 = traded == "no"

sc7 = index_ltp < first_candle['high']

print(f"SELL \t {current_time} \t {sc1} \t {sc2} \t {sc3} \t {sc4} \t {sc5} \t {sc7} \t first_candle {str(first_candle['timestamp'].time())} \n")

if bc1 and bc2 and bc3 and bc4 and bc5 and bc6 and bc7:

print("Buy Signal Formed")

CE_symbol_name, PE_symbol_name, strike = tsl.ATM_Strike_Selection(Underlying ='NIFTY',Expiry ='09-01-2024')

lot_size = tsl.get_lot_size(CE_symbol_name)*1

entry_orderid = tsl.order_placement(CE_symbol_name,'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info['options_name'] = CE_symbol_name

trade_info['qty'] = lot_size

trade_info['sl'] = first_candle['low']

trade_info['CE_PE'] = "CE"

if sc1 and sc2 and sc3 and sc4 and sc5 and sc6 and sc7:

print("Sell Signal Formed")

CE_symbol_name, PE_symbol_name, strike = tsl.ATM_Strike_Selection(Underlying ='NIFTY',Expiry ='09-01-2024')

lot_size = tsl.get_lot_size(PE_symbol_name)*1

entry_orderid = tsl.order_placement(PE_symbol_name,'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info['options_name'] = PE_symbol_name

trade_info['qty'] = lot_size

trade_info['sl'] = first_candle['high']

trade_info['CE_PE'] = "PE"

# ---------------------------- check for exit SL/TG

if traded == "yes":

long_position = trade_info['CE_PE'] == "CE"

short_position = trade_info['CE_PE'] == "PE"

if long_position:

sl_hit = index_ltp < trade_info['sl']

tg_hit = index_ltp < running_candle['SUPERT_10_2.0']

if sl_hit or tg_hit:

print("Order Exited", trade_info)

exit_orderid = tsl.order_placement(trade_info['options_name'],'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

# pdb.set_trace()

if short_position:

sl_hit = index_ltp > trade_info['sl']

tg_hit = index_ltp > running_candle['SUPERT_10_2.0']

if sl_hit or tg_hit:

print("Order Exited", trade_info)

exit_orderid = tsl.order_placement(trade_info['options_name'],'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

# pdb.set_trace()

Hi @Tradehull_Imran ,

I’m facing following issue,

I checked for all the dependencies and version of local python, all they are in good shape,

even though facing the following issue,

“Can we have all the updated new code in one place”,

I seen many of the times updates in the new files or version,

Due to which local code may not work sometimes,

So they are confusing to us.

TIA, ![]()

Hi @Arun_Rawat

Its a managed error in atm_strike_selection

use below code

import pdb

import time

import datetime

import traceback

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as pta

import pandas_ta as ta

import warnings

from Dhan_Tradehull_V2 import Tradehull

warnings.filterwarnings("ignore")

# ---------------- For Dhan Login ----------------

client_code = ""

token_id = ""

tsl = Tradehull(client_code, token_id)

available_balance = tsl.get_balance()

leveraged_margin = available_balance * 2

max_trades = 3

per_trade_margin = leveraged_margin / max_trades

max_loss = available_balance / 100 * -1

traded = "no"

trade_info = {"options_name": None, "qty": None, "sl": None, "CE_PE": None}

while True:

live_pnl = tsl.get_live_pnl()

current_time = datetime.datetime.now().time() # time only

if current_time < datetime.time(9, 45, 0):

print("Wait for the market to open", current_time)

continue

if current_time > datetime.time(15, 15, 30) or (live_pnl < max_loss):

tsl.kill_switch('ON')

tsl.cancel_all_orders()

print("Market is over or MAX LOSS reached, Bye for Now", current_time)

break

print("Algo is working", current_time)

try:

index_chart = tsl.get_historical_data(tradingsymbol='NIFTY JAN FUT', exchange='NFO', timeframe="5")

time.sleep(3)

index_ltp = tsl.get_ltp_data(names=['NIFTY JAN FUT'])['NIFTY JAN FUT']

except Exception as e:

print(e)

continue

# Apply Indicators

index_chart['rsi'] = talib.RSI(index_chart['close'], timeperiod=14)

index_chart.set_index(pd.DatetimeIndex(index_chart['timestamp']), inplace=True)

index_chart['vwap'] = pta.vwap(index_chart['high'], index_chart['low'], index_chart['close'], index_chart['volume'])

indi = ta.supertrend(index_chart['high'], index_chart['low'], index_chart['close'], 10, 2)

index_chart = pd.concat([index_chart, indi], axis=1, join='inner')

index_chart['pv'] = index_chart['close'] * index_chart['volume']

index_chart['vwma'] = index_chart['pv'].rolling(20).mean() / index_chart['volume'].rolling(20).mean()

first_candle = index_chart.iloc[-3]

second_candle = index_chart.iloc[-2]

running_candle = index_chart.iloc[-1]

# Buy Entry Conditions

bc1 = first_candle['close'] > first_candle['vwap']

bc2 = first_candle['close'] > first_candle['SUPERT_10_2.0']

bc3 = first_candle['close'] > first_candle['vwma']

bc4 = first_candle['rsi'] < 80

bc5 = second_candle['volume'] > 50000

bc6 = traded == "no"

bc7 = index_ltp > first_candle['low']

print(f"BUY \t {current_time} \t {bc1} \t {bc2} \t {bc3} \t {bc4} \t {bc5} \t {bc7} \t first_candle {str(first_candle['timestamp'].time())}")

# Sell Entry Conditions

sc1 = first_candle['close'] < first_candle['vwap']

sc2 = first_candle['close'] < first_candle['SUPERT_10_2.0']

sc3 = first_candle['close'] < first_candle['vwma']

sc4 = first_candle['rsi'] > 20

sc5 = second_candle['volume'] > 50000

sc6 = traded == "no"

sc7 = index_ltp < first_candle['high']

print(f"SELL \t {current_time} \t {sc1} \t {sc2} \t {sc3} \t {sc4} \t {sc5} \t {sc7} \t first_candle {str(first_candle['timestamp'].time())} \n")

if bc1 and bc2 and bc3 and bc4 and bc5 and bc6 and bc7:

print("Buy Signal Formed")

CE_symbol_name, PE_symbol_name, strike = tsl.ATM_Strike_Selection(Underlying='NIFTY', Expiry='09-01-2024')

if (CE_symbol_name is None) or (PE_symbol_name is None):

continue

lot_size = tsl.get_lot_size(CE_symbol_name) * 1

entry_orderid = tsl.order_placement(CE_symbol_name, 'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info.update({"options_name": CE_symbol_name, "qty": lot_size, "sl": first_candle['low'], "CE_PE": "CE"})

if sc1 and sc2 and sc3 and sc4 and sc5 and sc6 and sc7:

print("Sell Signal Formed")

CE_symbol_name, PE_symbol_name, strike = tsl.ATM_Strike_Selection(Underlying='NIFTY', Expiry='09-01-2024')

if (CE_symbol_name is None) or (PE_symbol_name is None):

continue

lot_size = tsl.get_lot_size(PE_symbol_name) * 1

entry_orderid = tsl.order_placement(PE_symbol_name, 'NFO', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info.update({"options_name": PE_symbol_name, "qty": lot_size, "sl": first_candle['high'], "CE_PE": "PE"})

# Check for exit SL/TG

if traded == "yes":

long_position = trade_info['CE_PE'] == "CE"

short_position = trade_info['CE_PE'] == "PE"

if long_position:

sl_hit = index_ltp < trade_info['sl']

tg_hit = index_ltp < running_candle['SUPERT_10_2.0']

if sl_hit or tg_hit:

print("Order Exited", trade_info)

tsl.order_placement(trade_info['options_name'], 'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

if short_position:

sl_hit = index_ltp > trade_info['sl']

tg_hit = index_ltp > running_candle['SUPERT_10_2.0']

if sl_hit or tg_hit:

print("Order Exited", trade_info)

tsl.order_placement(trade_info['options_name'], 'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

No module named talib, means the installation was not successful

do install libraries see : https://www.youtube.com/watch?v=YAyIoDJYorA&list=PLnuHyqUCoJsPA4l9KRLrNpWLIfZ9ucLxx&index=8

Also use the sequence : https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718/1065?u=tradehull_imran

code files : https://private-poc.madefortrade.in/t/learn-algo-trading-with-python-codes-youtube-series/32718?u=tradehull_imran

i am getting error in modify_order and cancel_order. Please help

Traceback (most recent call last):

File “/Users/vinodbhardwaj/Downloads/test/Trading/DhanTrading/Dhan_Tradehull_V2.py”, line 1431, in modify_order

p_orders = pd.DataFrame(self.xts1.get_order_book()[‘result’])

AttributeError: ‘Tradehull’ object has no attribute ‘xts1’