India’s Auto Sector just had its best year in 7 years. Here’s everything you need to know before touching these stocks. ![]()

FY2026 was historic for Indian automobiles. Every single major vehicle category : Passenger Vehicles, Commercial Vehicles, Three Wheelers, Two Wheelers, posted their all-time highest-ever annual sales simultaneously. Last time this happened in FY2018-19.

SIAM’s official data tells the story:

| Segment | FY26 Sales | Growth |

|---|---|---|

| Passenger Vehicles | 46.43 Lakh Units | +7.9% |

| Commercial Vehicles | 10.80 Lakh Units | +12.6% |

| Three Wheelers | 8.36 Lakh Units | +12.8% |

| Two Wheelers | 2.17 Crore Units | +10.7% |

And April 2026 (first month of FY27)? PVs grew +25.4%, 3Ws grew +32.8%. Momentum is not slowing.

What drove this? Three real reasons.

-

GST 2.0 : Rate rationalisation dropped the effective cost of vehicles. H1 FY26 was flat (-1.4% for PVs), but H2 exploded at +16.7%. One policy change, completely different half.

-

Multiple RBI rate cuts : Auto loans got cheaper. For CV buyers who finance 60-80% of the vehicle price, this is literally thousands of rupees off monthly EMI. Direct volume trigger.

-

Income tax relief in the Budget : Disposable income went up. First-time car buyers in the ₹8-15L segment pulled the trigger.

The Powertrain Story - This is where it gets interesting

India in FY26 is NOT a petrol-only market anymore. Look at the fuel split:

- Petrol- 52.6% (still #1, but losing share every year)

- CNG- 21.7% (the REAL story of FY26 — 10+ lakh units!)

- Diesel- 18.4% (declining overall, but alive in SUVs)

- EV- 4.6% (nearly doubled YoY)

- Hybrid- 2.7% (Toyota’s game entirely)

CNG has become mainstream, not alternative. Maruti alone sold 7.08 lakh CNG cars that’s ~70% of India’s entire CNG car market. When petrol costs ₹105/litre and CNG costs ₹75/kg and gives better mileage… the math is obvious.

EV crossed 2.2 lakh units with 80%+ growth. The surprise? MG Windsor became India’s #1 EV (46,720 units), beating Tata Nexon. Windsor’s battery-as-a-service model killed the upfront price barrier. Genuinely innovative.

Now the listed stocks

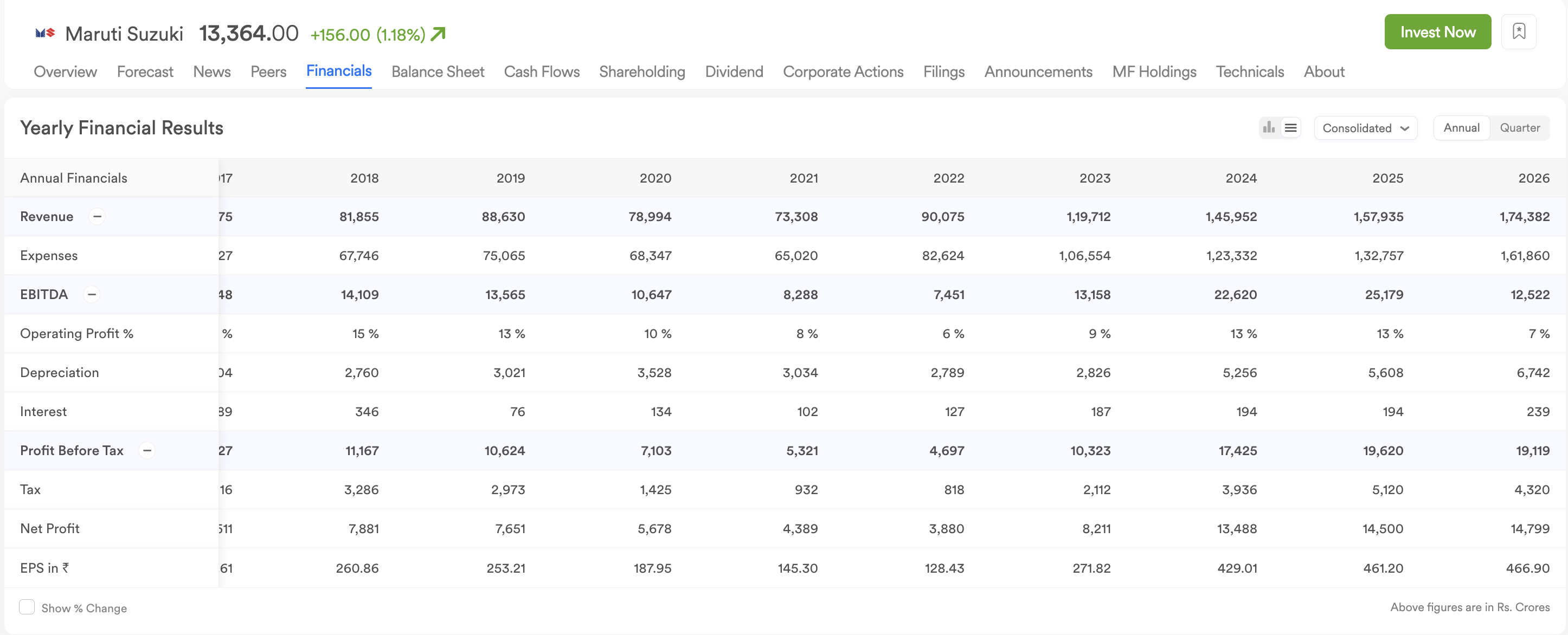

Maruti Suzuki

(Mkt Cap ₹4.2L Cr | Revenue Growth 10.41% | P/E 28x )

The OG. Dzire was India’s overall bestselling car in FY26. CNG moat is unbeatable right now. Serviced a record 2.84 crore vehicles in FY26. This stock is unbeatable in after-sales service, a big chunk in its revenue machine.

But eVitara sold only 3,652 units in its launch year. Tata sold 85,000 EVs in the same period. If EV adoption accelerates faster than expected, Maruti’s 40% market share story could face pressure. For now, CNG is buying them time.

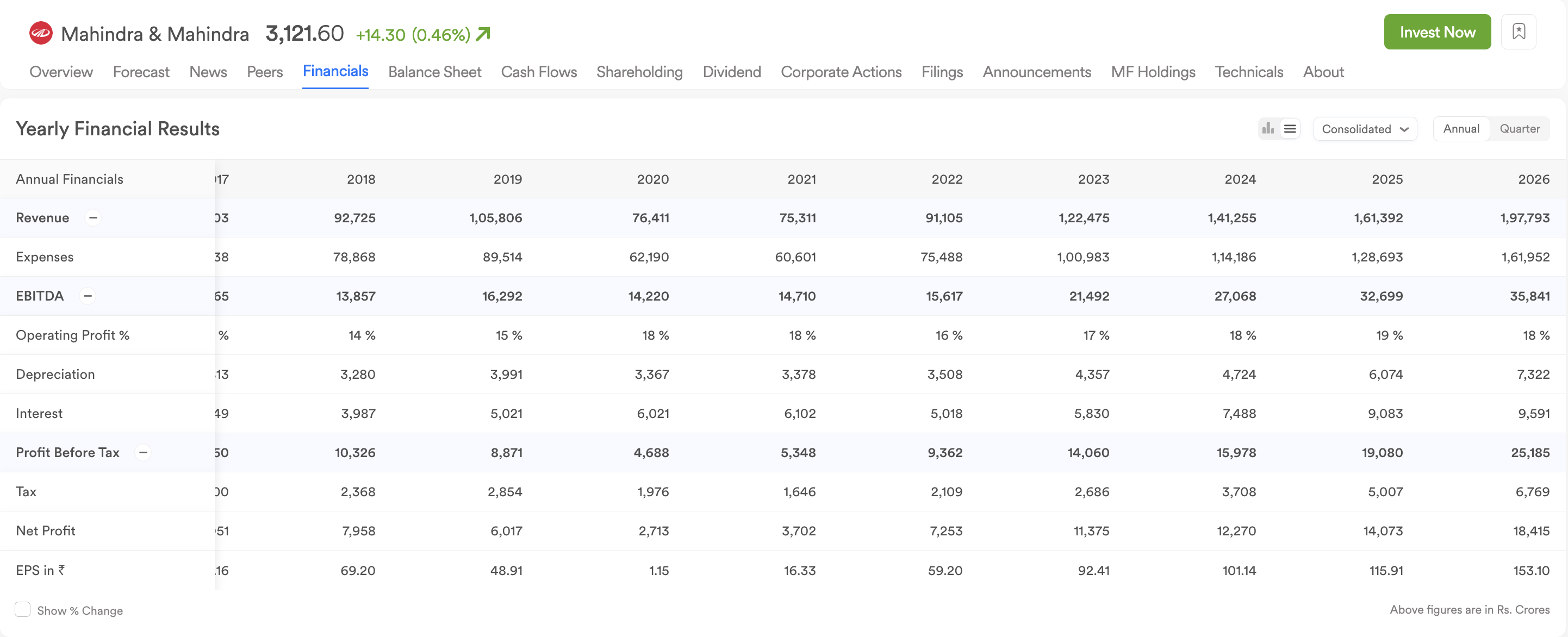

Mahindra & Mahindra

(Mkt Cap ₹3.9L Cr | Revenue Growth 22.5% | P/E 20.75x )

Arguably the best risk/reward in the whole space right now.

Why? Because they’re playing both sides. 74.6% of portfolio is diesel SUVs (cash cow). AND XEV 9e became India’s #3 EV with 27,336 units in its launch year.

You’re getting diesel SUV dominance & EV optionality in one stock, at a cheaper P/E than Maruti. Free cash flow is negative right now (-7,216 Cr) because of heavy EV investment, that’s the risk. But M&M has farm equipment, IT and financial services to fund it.

Thesis here is, if EVs win >> M&M’s new platforms pay off big. If EVs are slow >> diesel SUV cash flow protects.

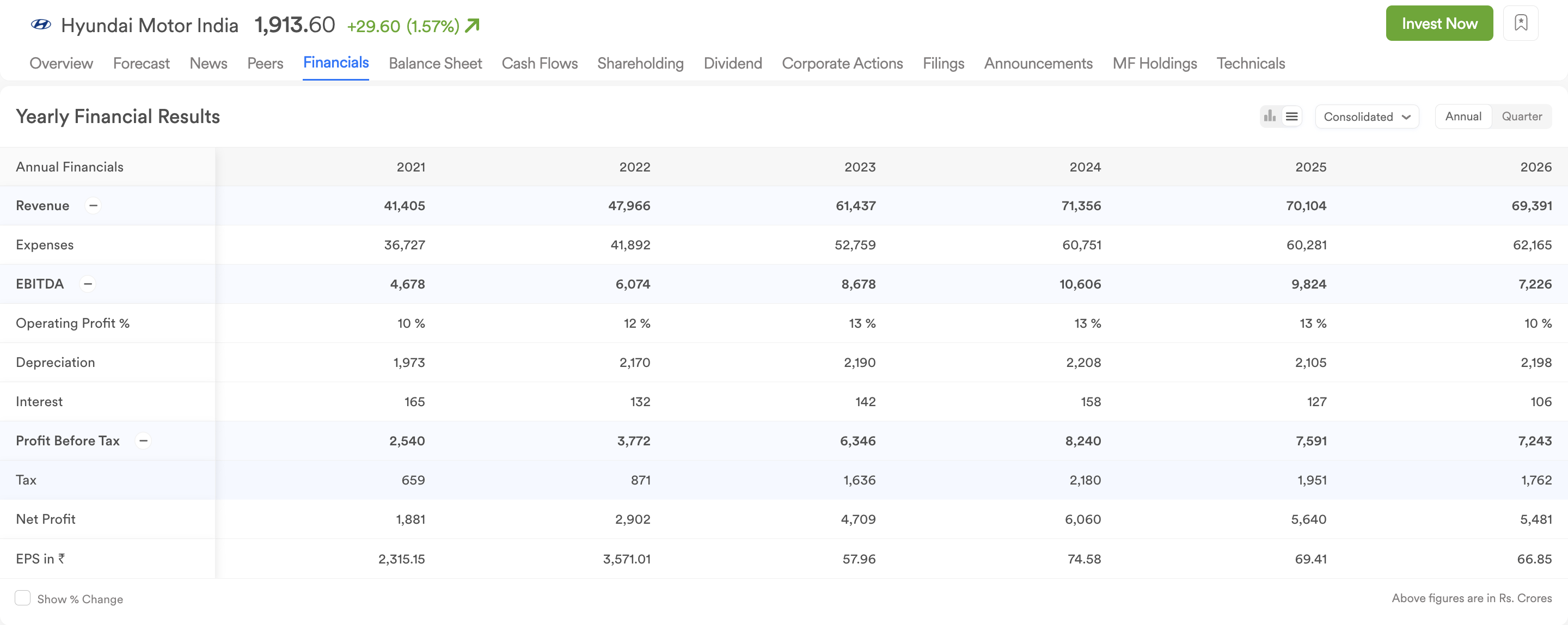

Hyundai Motor India

(Mkt Cap ₹1.55L Cr | Revenue Growth -1.02% | P/E 28x )

ROCE of 41% in a capital-intensive auto business is genuinely exceptional. Creta is India’s most-loved compact SUV, won’t change tomorrow.

The gap: Only 2.6% of Hyundai’s India sales are EVs. When MG is at 85.8% EV and Tata at 14%, Hyundai’s EV portfolio is thin. Also, as a majority-owned subsidiary of Korean parent, dividend policy isn’t entirely in domestic investors’ hands.

This stock is for who want quality + profitability + lower volatility. Less growth upside than M&M, but cleaner execution story.

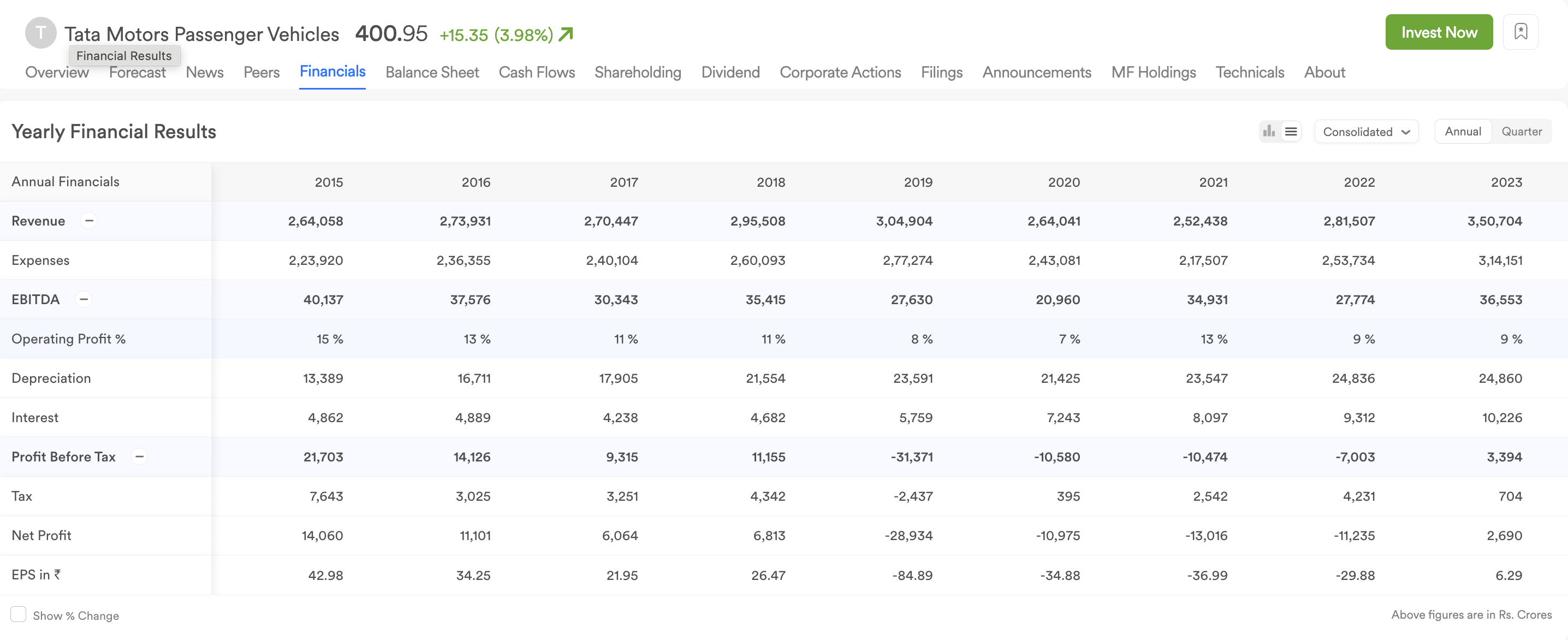

Tata Motors Passenger Vehicle

(Mkt Cap ₹1.47L Cr | Revenue Growth -25.2% | P/E 1.72X )

Complicated story. When you buy Tata Motors PV, you’re buying:

- India EV leadership (85,000 PV EVs, 38.8% EV market share)

- Tata Motors Passenger Vehicles (Nexon, Punch, Harrier, Safari and latest Sierra)

- Jaguar Land Rover (global luxury cars, sold in UK/Europe)

The low-looking P/E on screeners is misleading because JLR’s profits are outsized this year. Tata’s India EV moat is real — Tata Power charging network + widest EV portfolio + first-mover trust. But JLR is exposed to European recession risk and the UK EV mandate.

Value investors who understand the JLR overlay and are comfortable with global macro risk can explore this stock. Not a clean pure-play.

Key risks to watch in FY27

-

West Asia conflict - SIAM flagged this explicitly. Crude oil price spike = higher input costs + CNG cost increases + consumer sentiment hit. Watch Brent crude closely.

-

EV infrastructure gap - Charging stations in Tier 2/3 cities are still thin. Every industry roundtable in Feb-March 2026 cited this as the #1 barrier to next phase of EV growth.

-

Commodity prices - ET headline from May 20 was literally “Automakers’ Joy Ride Hits a Big Cost Hurdle.” Steel + aluminium input cost pressures are building.

Share your thoughts on these stocks in the thread below.

Full list of automobile stocks

Disclaimer: This is not investment advice. All data from SIAM, AutoPunditz, and ScanX. Do your own research before investing.