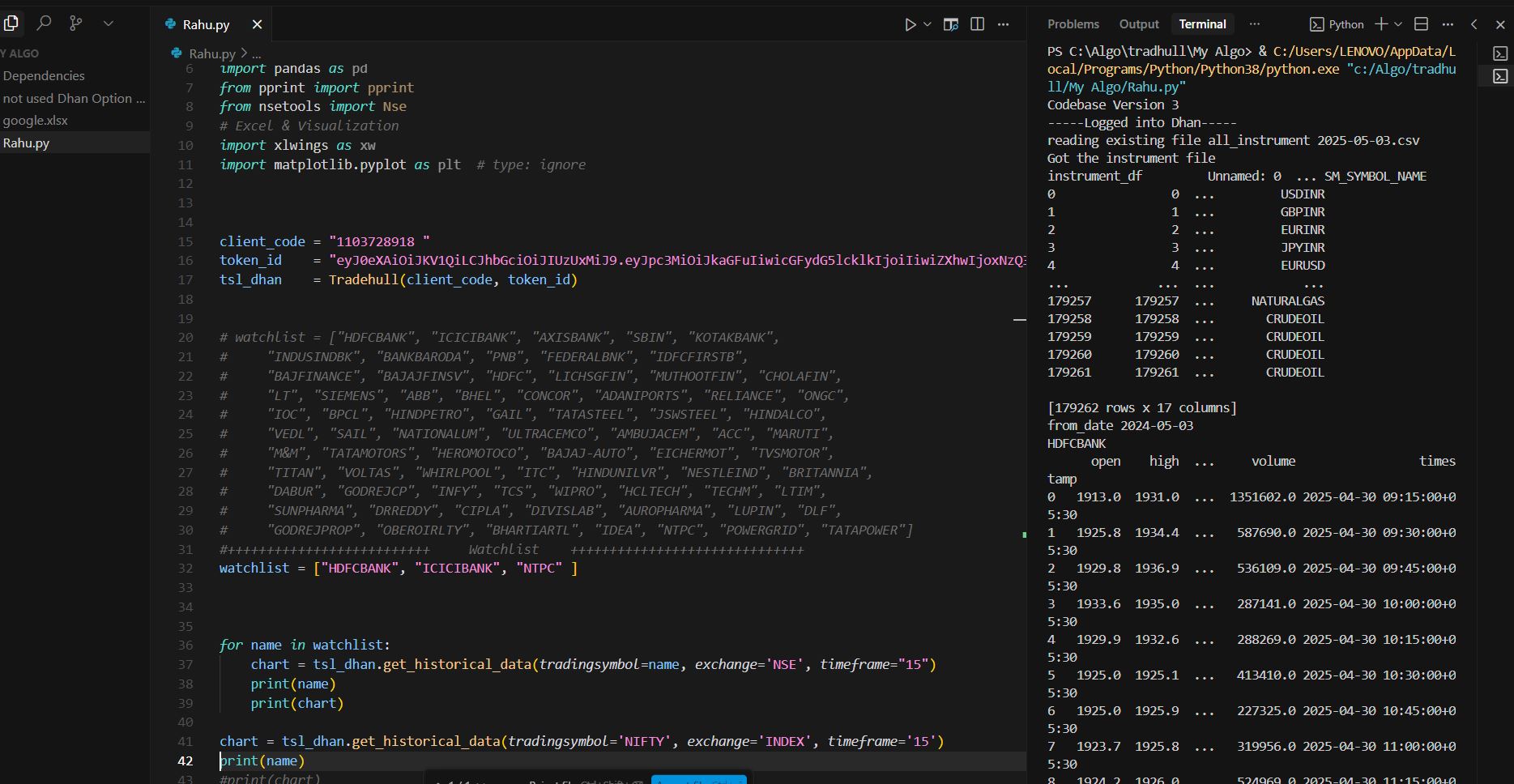

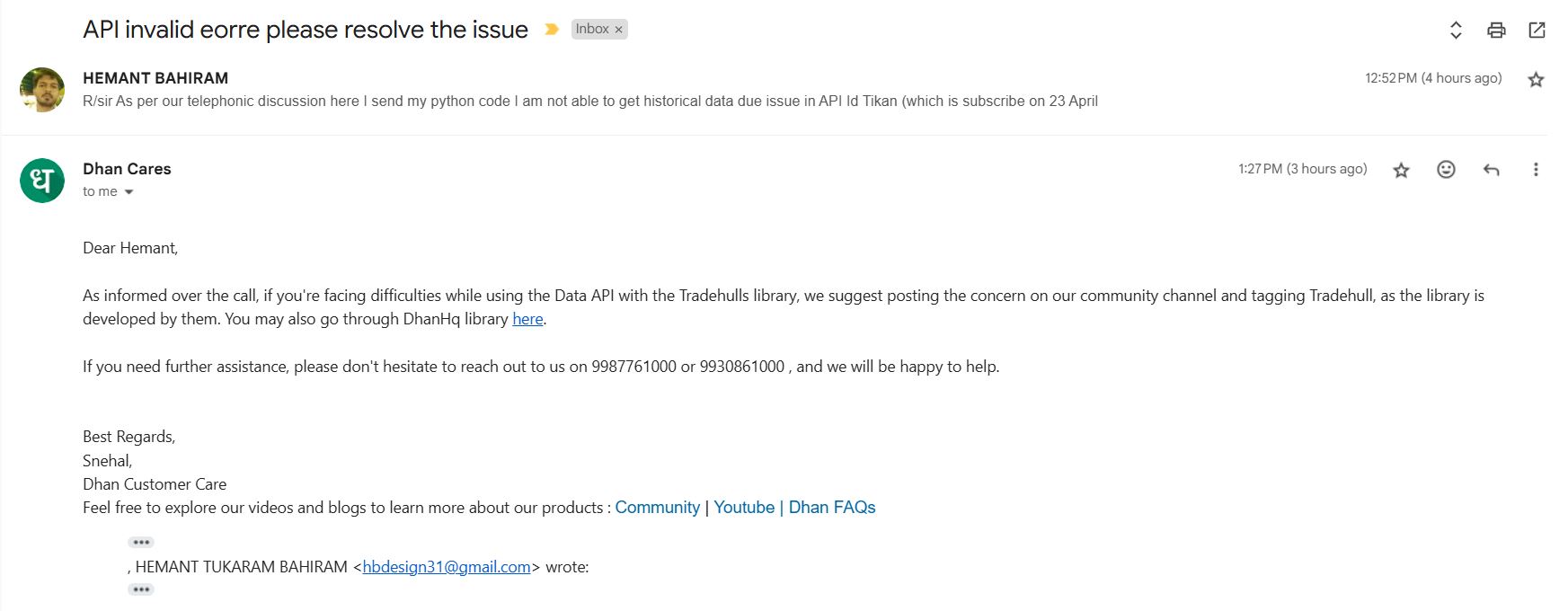

from Dhan_Tradehull import Tradehull

import datetime

import pdb

import os

client_code = "000000 "

token_id = "000000"

tsl = Tradehull(client_code, token_id)

index_name = 'SENSEX'

no_strikes_to_replay = 10

expiry_date = "29 APR"

start_time ='2025-04-29 09:15:00+05:30'

today_date = datetime.datetime.now().date()

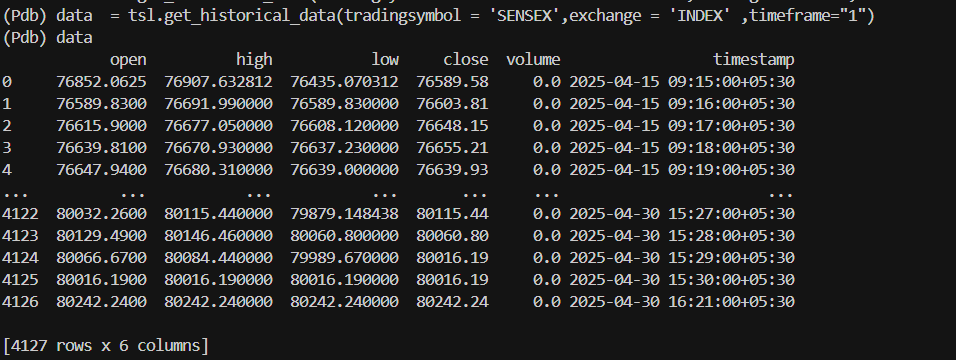

index_data = tsl.get_historical_data(tradingsymbol=index_name, exchange='INDEX', timeframe="1")

ATM_time_data = index_data[index_data['timestamp']==start_time]

if not ATM_time_data.empty:

ATM_close = ATM_time_data.iloc[-1]['close']

step = tsl.index_step_dict[index_name]

ATM_Strike = round(ATM_close/step)*step

all_strikes = [ATM_Strike+(step*i) for i in range(1,no_strikes_to_replay+1)] + [ATM_Strike-(step*i) for i in range(1,no_strikes_to_replay+1)] + [ATM_Strike]

call_and_put_Strikes = [f"{index_name} {expiry_date} {strike} CALL" for strike in all_strikes] + [f"{index_name} {expiry_date} {strike} PUT" for strike in all_strikes]

file_path = f'data/{index_name}/{today_date}/'

directory = os.path.dirname(file_path)

if not os.path.exists(directory):

os.makedirs(directory)

for strike in call_and_put_Strikes:

option_df = tsl.get_historical_data(tradingsymbol=strike, exchange='NFO', timeframe="1")

option_df.to_csv(f'data/{index_name}/{today_date}/{strike}.csv',index=False)

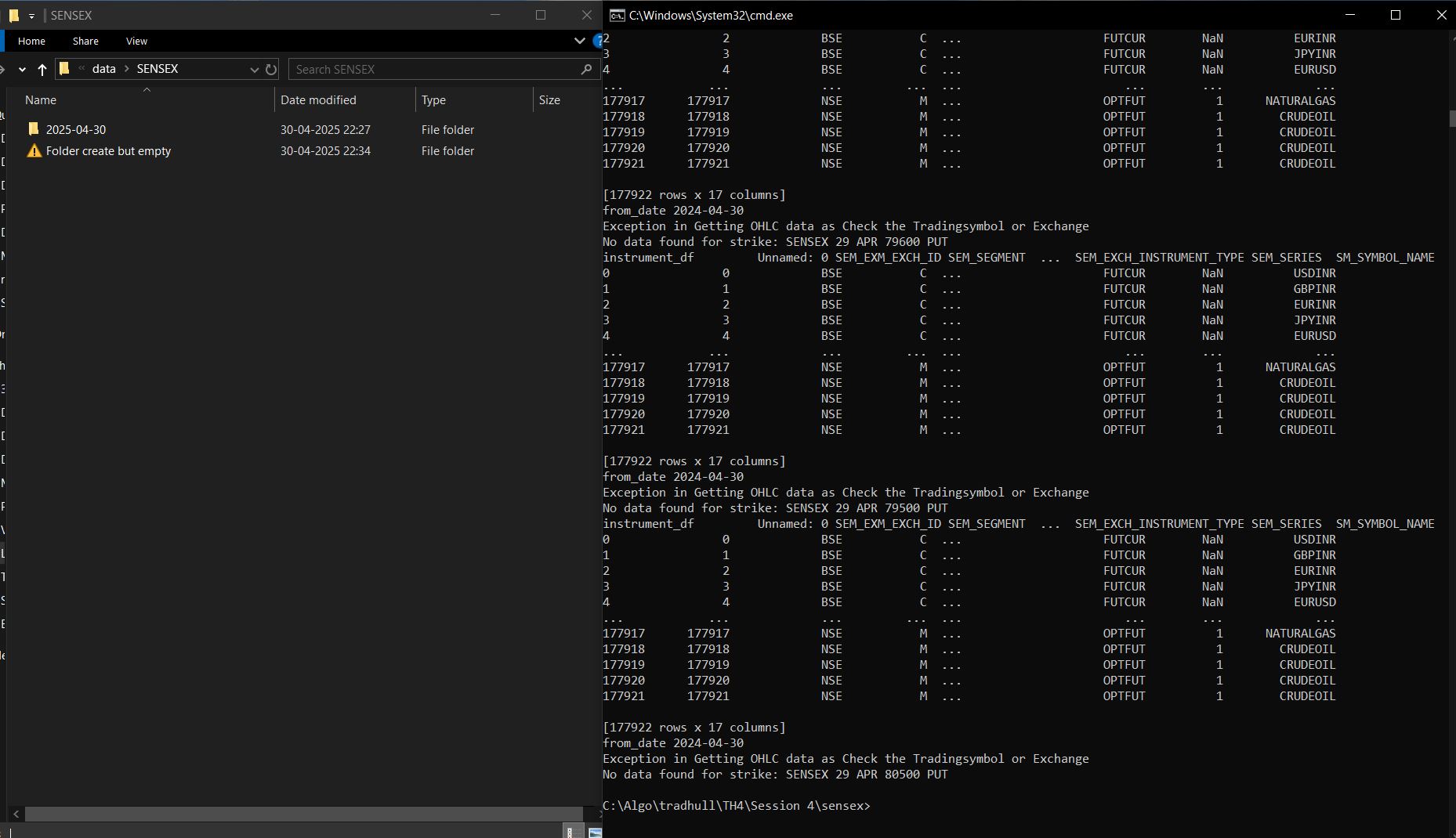

ERROR

.exe "c:/Dhan Option Chain/1. Download_Historical_data_SENSEX.pyCodebase Version 3

-----Logged into Dhan-----

reading existing file all_instrument 2025-04-29.csv

Got the instrument file

instrument_df Unnamed: 0 SEM_EXM_EXCH_ID … SEM_SERIES SM_SYMBOL_NAME

0 0 BSE … NaN USDIR

1 1 BSE … NaN GBPIR

2 2 BSE … NaN EURIR

3 3 BSE … NaN JPYIR

4 4 BSE … NaN EURUD

… … … … … ..

177151 177151 NSE … 1 NATURALGS

177152 177152 NSE … 1 CRUDEOL

177153 177153 NSE … 1 CRUDEOL

177154 177154 NSE … 1 CRUDEOL

.exe "c:/Dhan Option Chain/1. Download_Historical_data_SENSEX.pyCodebase Version 3

-----Logged into Dhan-----

reading existing file all_instrument 2025-04-29.csv

Got the instrument file

instrument_df Unnamed: 0 SEM_EXM_EXCH_ID … SEM_SERIES SM_SYMBOL_NAME

0 0 BSE … NaN USDIR

1 1 BSE … NaN GBPIR

2 2 BSE … NaN EURIR

3 3 BSE … NaN JPYIR

4 4 BSE … NaN EURUD

… … … … … ..

177151 177151 NSE … 1 NATURALGS

177152 177152 NSE … 1 CRUDEOL

177153 177153 NSE … 1 CRUDEOL

177154 177154 NSE … 1 CRUDEOL

.exe "c:/Dhan Option Chain/1. Download_Historical_data_SENSEX.pyCodebase Version 3

-----Logged into Dhan-----

reading existing file all_instrument 2025-04-29.csv

Got the instrument file

instrument_df Unnamed: 0 SEM_EXM_EXCH_ID … SEM_SERIES SM_SYMBOL_NAME

0 0 BSE … NaN USDIR

1 1 BSE … NaN GBPIR

2 2 BSE … NaN EURIR

3 3 BSE … NaN JPYIR

4 4 BSE … NaN EURUD

… … … … … ..

177151 177151 NSE … 1 NATURALGS

177152 177152 NSE … 1 CRUDEOL

177153 177153 NSE … 1 CRUDEOL

177154 177154 NSE … 1 CRUDEOL

.exe "c:/Dhan Option Chain/1. Download_Historical_data_SENSEX.pyCodebase Version 3

-----Logged into Dhan-----

reading existing file all_instrument 2025-04-29.csv

Got the instrument file

instrument_df Unnamed: 0 SEM_EXM_EXCH_ID … SEM_SERIES SM_SYMBOL_NAME

0 0 BSE … NaN USDIR

1 1 BSE … NaN GBPIR

2 2 BSE … NaN EURIR

3 3 BSE … NaN JPYIR

4 4 BSE … NaN EURUD

… … … … … ..

177151 177151 NSE … 1 NATURALGS

177152 177152 NSE … 1 CRUDEOL

177153 177153 NSE … 1 CRUDEOL

177154 177154 NSE … 1 CRUDEOL

reading existing file all_instrument 2025-04-29.csv

Got the instrument file

instrument_df Unnamed: 0 SEM_EXM_EXCH_ID … SEM_SERIES SM_SYMBOL_s x 17 columns]

NAME

0 0 BSE … NaN USDIR

1 1 BSE … NaN GBPIR

2 2 BSE … NaN EURIR

3 3 BSE … NaN JPYIR

4 4 BSE … NaN EURUD

… … … … … ..

177151 177151 NSE … 1 NATURALGS

177152 177152 NSE … 1 CRUDEOL

177153 177153 NSE … 1 CRUDEOL

177154 177154 NSE … 1 CRUDEOL

177155 177155 NSE … 1 CRUDEOL

177155 177155 NSE … 1 CRUDEOLrom_date 2024-04-29

[177156 rows x 17 columns]

from_date 2024-04-29

instrument_df Unnamed: 0 SEM_EXM_EXCH_ID … SEM_SERIES 1 BSE … NaN GBPISM_SYMBOL_NAME

0 0 BSE … NaN USDIR

1 1 BSE … NaN GBPIR 4 BSE … NaN EURU

2 2 BSE … NaN EURI

[177156 rows x 17 columns]

from_date 2024-04-29

instrument_df Unnamed: 0 SEM_EXM_EXCH_ID … SEM_SERIES SM_SYMBOL_NAME

0 0 BSE … NaN USDINR

1 1 BSE … NaN GBPINR

2 2 BSE … NaN EURINR

3 3 BSE … NaN JPYINR

4 4 BSE … NaN EURUSD

… … … … … …

177151 177151 NSE … 1 NATURALGAS

177152 177152 NSE … 1 CRUDEOIL

177153 177153 NSE … 1 CRUDEOIL

177154 177154 NSE … 1 CRUDEOIL

177155 177155 NSE … 1 CRUDEOIL

[177156 rows x 17 columns]

from_date 2024-04-29

Exception in Getting OHLC data as Check the Tradingsymbol or Exchange

Traceback (most recent call last):

File “c:/Dhan Option Chain/1. Download_Historical_data_SENSEX.py”, line 49, in

option_df.to_csv(f’data/{index_name}/{today_date}/{strike}.csv’,index=False)

AttributeError: ‘NoneType’ object has no attribute ‘to_csv’

PS C:\Users\LENOVO>

Folder create but empty

Same problem for other index also