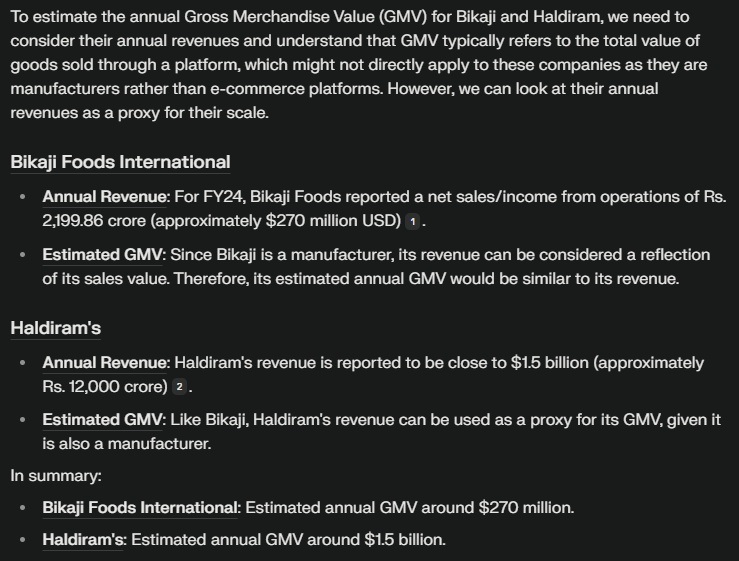

Singapore’s Temasek Holdings has finalized a landmark deal, securing a 10% stake in Haldiram’s for $1 billion, valuing the iconic Indian snacks and restaurant brand at an estimated $10 billion. This deal marks one of the most significant foreign investments in India’s consumer packaged goods (CPG) sector, highlighting the increasing attractiveness of India’s food and FMCG industry to global investors.

Haldiram’s, a household name in India, has built a formidable presence in both snacks and quick-service restaurants (QSR). With growing demand for traditional Indian packaged snacks and an expanding global footprint, the brand has become a prime target for private equity and sovereign wealth funds looking to tap into India’s consumer market.

Why Private Equity is Rushing into India

India has emerged as a hotspot for private equity (PE) and venture capital (VC) funding, driven by robust economic growth, a rising middle class, and increasing digital adoption. Temasek’s investment in Haldiram’s underscores several key trends:

- Consumer Growth Potential: India’s food and beverage market is expected to reach $1 trillion by 2030, fueled by changing consumption habits and urbanization.

- Global Investors’ Interest in Indian Brands: Private equity firms and sovereign wealth funds, including Temasek, Blackstone, and KKR, have been actively acquiring stakes in India’s FMCG and QSR brands, recognizing their long-term value.

- Exit Potential & IPO Pipeline: With India’s capital markets performing well, many PE-backed companies are considering IPOs or strategic exits, making investments even more lucrative.

- Government Reforms & Ease of Business: India’s liberalized FDI policies and regulatory improvements have made it easier for foreign investors to enter high-growth sectors like food, retail, and logistics.

How This Funding Will Shape Haldiram’s Future

Temasek’s investment provides Haldiram’s with a financial war chest to accelerate its expansion, innovation, and global ambitions. Here’s how the capital infusion is expected to play out:

- Expansion in Domestic & International Markets: Haldiram’s aims to increase its footprint in tier-2 and tier-3 cities in India while expanding exports, particularly in the US, Middle East, and Southeast Asia.

- Strengthening Manufacturing & Supply Chain: Funds will likely be deployed to scale up manufacturing capacity, modernize supply chains, and ensure product consistency across global markets.

- Potential IPO Consideration: With a valuation of $10 billion, Haldiram’s could be preparing for an IPO in the coming years, offering further liquidity to its investors.

- Innovation in Product Lines: The funding could support R&D efforts, allowing the brand to develop healthier, premium, and digital-first snack offerings to cater to evolving consumer preferences.

What This Means for Private Equity in India

The Haldiram’s-Temasek deal is part of a broader wave of private equity and sovereign wealth fund investments in India’s consumer-driven sectors. We are seeing similar moves in fintech, e-commerce, and manufacturing as PE firms deploy billions into high-growth, cash-generating businesses.

Looking ahead, India’s startup and mid-sized business ecosystem is poised for a record-breaking influx of PE investments, with sectors like QSR, D2C brands, renewable energy, and financial services being the key beneficiaries.

Conclusion

Temasek’s acquisition of a 10% stake in Haldiram’s for $1 billion is more than just an investment—it’s a validation of India’s consumer market potential and the growing role of private equity in shaping its future. As global investors continue to seek exposure to India’s high-growth sectors, we can expect further large-scale deals, strategic exits, and potential IPOs in the near future.

How do you see this funding playing out? Would more global funds follow Temasek’s path into India’s food and FMCG sector? Share your thoughts.