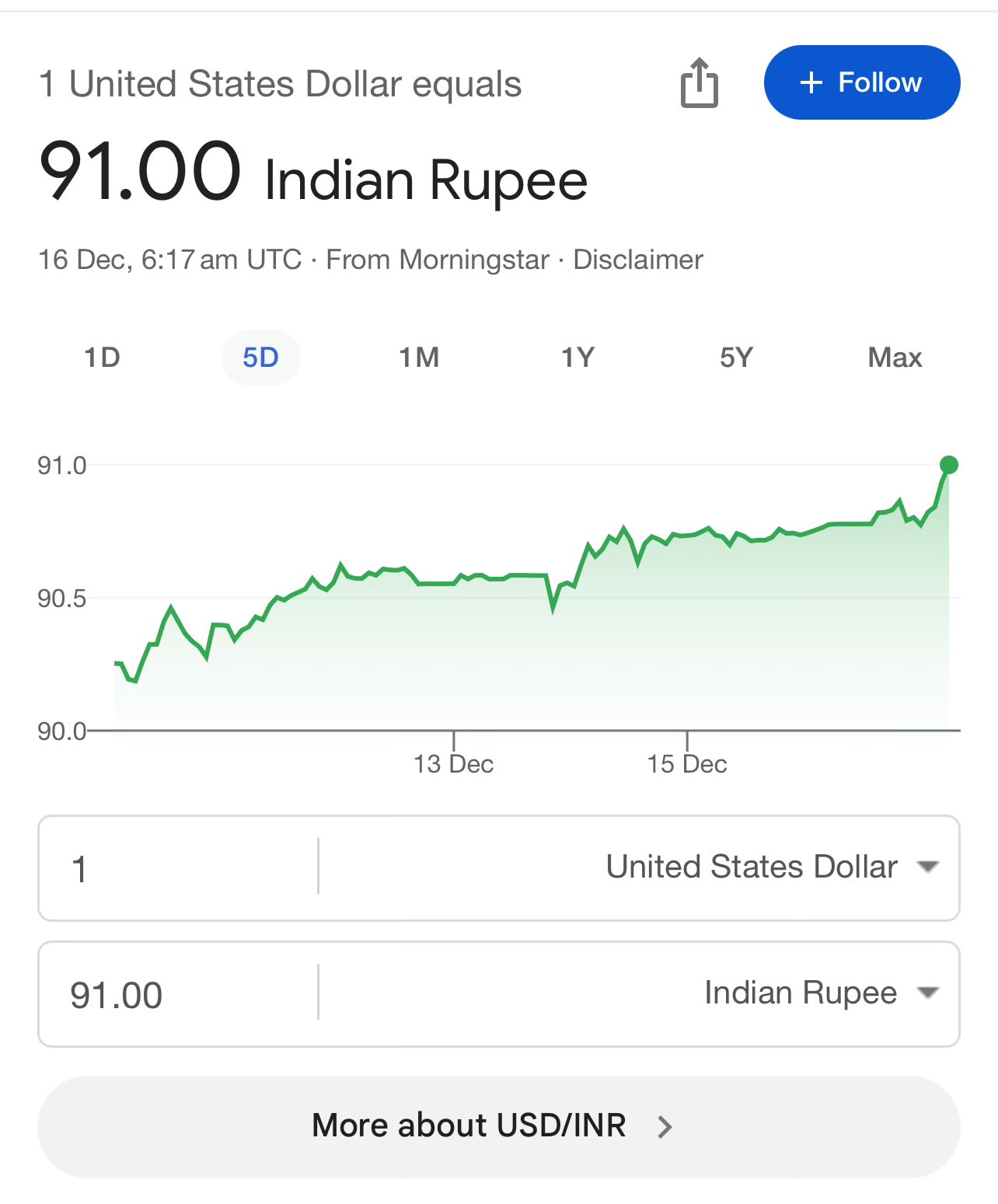

USDINR has crossed the 90 mark and hit new all-time highs. The rupee has been getting weaker for over a year now, moving from the 83–84 zone in 2024 to where it is today. This has happened because of a mix of global and local factors.

Globally, the US dollar has become stronger as US interest rates remain high and many investors are moving money back to the US. When the dollar strengthens, most emerging-market currencies fall, and the rupee is no exception.

On the domestic side, India’s import bill has jumped, foreign investors have been selling, and there are some growth concerns. All of this has added pressure on the rupee and pushed USDINR to new highs.

Different sectors react differently to a weak rupee.

Export-based sectors like IT, pharma, speciality chemicals and some manufacturers may benefit. They earn in dollars but report in rupees, so a weaker rupee can help their revenue and margins.

Import-heavy sectors feel the squeeze. Oil companies, airlines, paint makers and firms with dollar loans may face higher costs and lower profits. A weaker rupee can also push inflation higher because imported goods and commodities become more expensive.

But for normal retail traders like us, the impact is mostly indirect. We do not get affected in our day-to-day trading, but sector moves can change, and certain stocks may behave differently.

How are you looking at this move?

Am looking at RBI and asking why you did what you did to virtually halt retail currency trading  It has been a really massive long term bull run for USDINR

It has been a really massive long term bull run for USDINR

Does a country’s quality of life decline when its domestic currency starts losing value?

Yes, a declining domestic currency can lower the quality of life for ordinary citizens. When a currency weakens, the cost of imported goods—such as fuel, food items, medical equipment, electronics, and raw materials—goes up. This leads to higher overall prices (inflation), which reduces people’s purchasing power. Even if salaries stay the same, everyday essentials become more expensive, making it harder for families to maintain their usual standard of living.

Over time, savings lose value, foreign travel becomes costlier, and businesses face higher production expenses, which often get passed on to consumers. While certain sectors like exports may benefit, the average citizen experiences rising costs and financial stress, resulting in a gradual decline in quality of life.

3 Likes

Re-reading this thread now is interesting. When @Mohseen_Usmani put this up in December, USDINR had just crossed 90 and @Goal_Archiver flagged 91 a week later. Five months on, we are sitting near 95. The original framing in this post (stronger dollar, FII outflows, import bill) all still holds up, but there is one piece that was not really on the table back in December and has become central to the story since.

Jefferies put out a note last week titled “INR Pressure – The Downside of SIPs” arguing that the real culprit for rupee weakness is not CAD, it is the capital account. Their point is that FPIs sold $44 billion of Indian equities since April 2024, but because domestic SIP flows kept absorbing every share they dumped, the index never broke. The pressure went somewhere though, and that somewhere was the rupee. Every dollar an FPI takes out has to be converted back to USD, and the SIP wall does not absorb that FX leg.

April 2026 AMFI data shows ₹38,440 crore of net equity inflow in just one month, which is roughly a quarter of what FPIs sold across all of FY26. So the absorption is real, the equity market stays stable, but the rupee carries the cost.

Wrote a longer breakdown of this with the Korea and Japan parallels here in case it is useful: Jefferies just blamed our SIP for the rupee’s fall. Is that fair?

@dazzler263 your point about quality of life ties into this directly. If domestic flows are now structurally setting up a weaker rupee floor, the imported inflation effect you described is not a cyclical thing anymore, it is becoming part of the baseline.

Do go through the new article, would love to know your insights on it.

1 Like