@Tradehull_Imran need your help my algo is not placing order getting an error.

sharing with you full code can you please help me on this my algo is not fetch ce data may i know the reason please help me.

traded = “no”

trade_info = {“options_name”:None, “qty”:None, “sl”:None, “CE_PE”:None}

while True:

time.sleep(2)

current_time = datetime.datetime.now()

index_chart = tsl.get_historical_data(tradingsymbol='CRUDEOIL FEB FUT', exchange='MCX', timeframe="5")

# rsi ------------------------ apply indicators

index_chart['rsi'] = talib.RSI(index_chart['close'], timeperiod=14)

# vwap

index_chart.set_index(pd.DatetimeIndex(index_chart['timestamp']), inplace=True)

index_chart['vwap'] = pta.vwap(index_chart['high'] , index_chart['low'], index_chart['close'] , index_chart['volume'])

# Supertrend

indi = ta.supertrend(index_chart['high'], index_chart['low'], index_chart['close'], 10, 2)

index_chart = pd.concat([index_chart, indi], axis=1, join='inner')

# vwma

index_chart['pv'] = index_chart['close'] * index_chart['volume']

index_chart['vwma'] = index_chart['pv'].rolling(20).mean() / index_chart['volume'].rolling(20).mean()

# volume

volume = 50,000

first_candle = index_chart.iloc[-3]

second_candle = index_chart.iloc[-2]

running_candle = index_chart.iloc[-1]

# ---------------------------- BUY ENTRY CONDITIONS ----------------------------

bc1 = first_candle['close'] > first_candle['vwap'] # First Candle close is above VWAP

bc2 = first_candle['close'] > first_candle['SUPERT_10_2.0'] # First Candle close is above Supertrend

bc3 = first_candle['close'] > first_candle['vwma'] # First Candle close is above VWMA

bc4 = first_candle['rsi'] < 80 # First candle RSI < 80

#bc5 = second_candle['volume'] > 50000 # Second candle Volume should be greater than 50,000 for Nifty and above 125,000 for Bank Nifty

print("BUY ", current_time, bc1, bc2, bc3, bc4,)

if bc1 and bc2 and bc3 and bc4:

print("BUY Signal Formed")

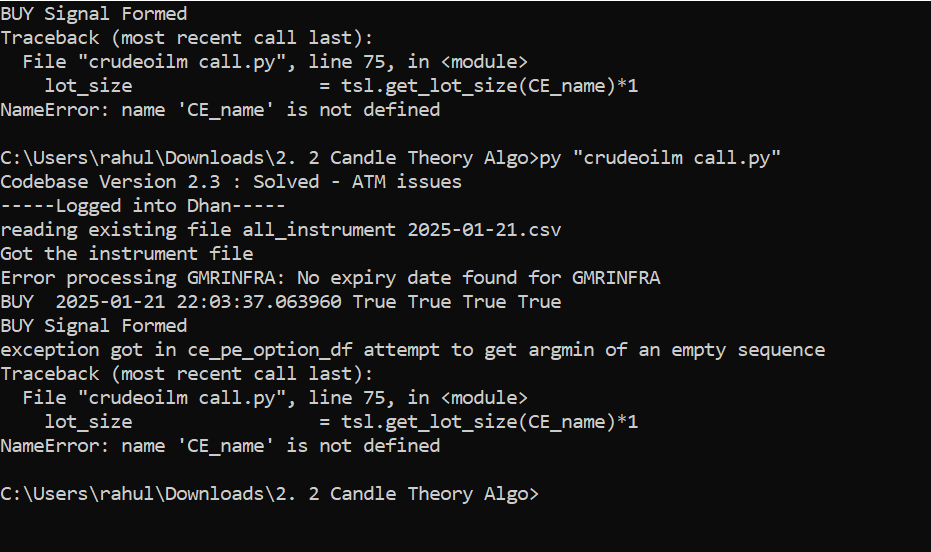

ce_name, pe_name, strike = tsl.ATM_Strike_Selection(Underlying ='CRUDEOIL',Expiry ='19-02-2025')

lot_size = tsl.get_lot_size(CE_name)*1

entry_orderid = tsl.order_placement(CE_name,'MCX', lot_size, 0, 0, 'MARKET', 'BUY', 'MIS')

traded = "yes"

trade_info['options_name'] = CE_name

trade_info['qty'] = lot_size

trade_info['sl'] = first_candle['low']

trade_info['CE_PE'] = "CE"

# ---------------------------- check for exit SL/TG

#if traded == "yes":

index_ltp = tsl.get_ltp_data(names = ['CRUDEOIL FEB FUT'])['CRUDEOIL FEB FUT']

long_position = trade_info['CE_PE'] == "CE"

short_position = trade_info['CE_PE'] == "PE"

if long_position:

sl_hit = index_ltp < trade_info['sl']

tg_hit = index_ltp < running_candle['SUPERT_10_2.0']

if sl_hit or tg_hit:

print("Order Exited", trade_info)

exit_orderid = tsl.order_placement(trade_info['options_name'],'NFO', trade_info['qty'], 0, 0, 'MARKET', 'SELL', 'MIS')

pdb.set_trace()

- List item