Hey everyone,

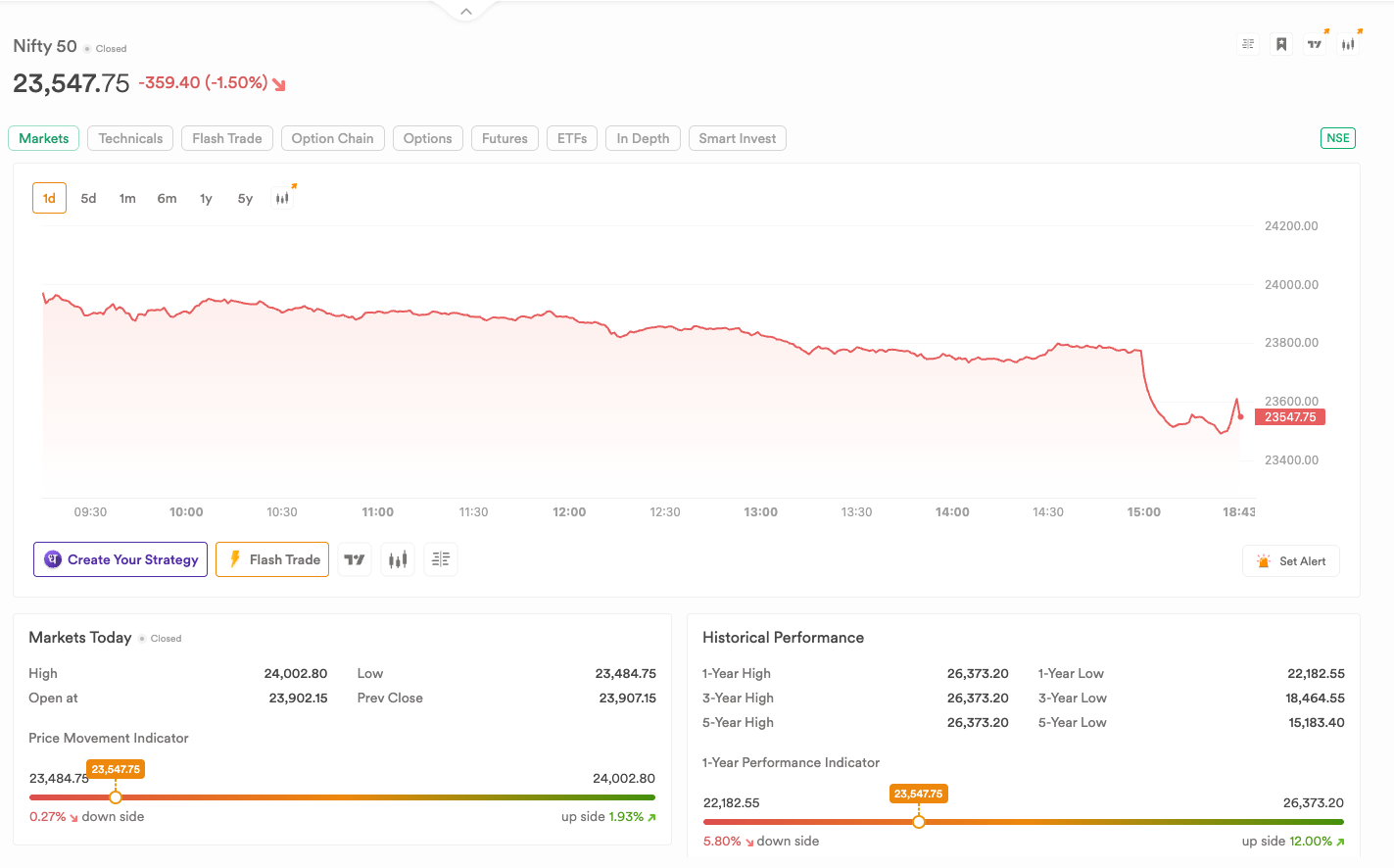

If you were watching your screen around 3 PM today, you saw something that looks terrifying on a chart and feels worse in a portfolio. Nifty opened firm near 23,902, even poked above 24,000 in the morning, and then spent the whole day quietly drifting lower. Nothing alarming. Then the close arrived and the floor gave way. Nifty finished at 23,547, down 359 points or 1.50%, after tagging a low of 23,484. Almost all the real damage came in one ugly red candle right near the end.

Here is the part worth slowing down for: most of that final drop had almost nothing to do with any company getting worse, any earnings miss, or any breaking headline. It was plumbing. Specifically, it was the MSCI rebalancing.

So what is the “MSCI rebalancing candle”?

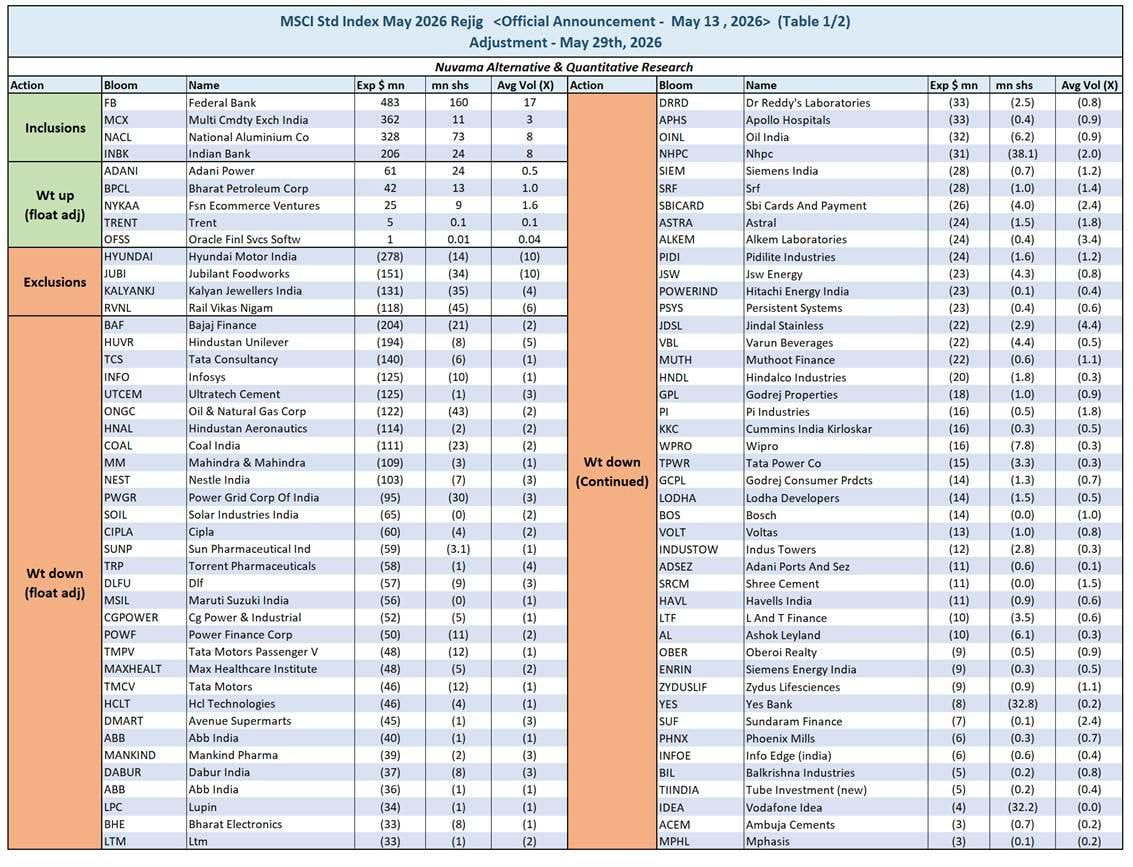

MSCI runs some of the most widely tracked global indices in the world. Funds sitting in the US, Europe, the Gulf, everywhere, benchmark themselves to MSCI India and MSCI Emerging Markets. A few times a year, MSCI reshuffles which Indian stocks sit inside those indices and how much weight each one carries. Today, May 29, was that adjustment day for the May 2026 cycle (the changes were actually announced back on May 13, so the market knew this was coming).

The headline part: who got in, who got dropped

The names everyone quotes are the inclusions and exclusions:

- Added: Federal Bank, Multi Commodity Exchange (MCX), National Aluminium (NALCO) and Indian Bank.

- Removed: Hyundai Motor India, Jubilant FoodWorks, Kalyan Jewellers and Rail Vikas Nigam (RVNL).

Per Nuvama’s estimates, Federal Bank alone was due roughly $483 million of passive buying (close to ₹4,000 crore), while Hyundai faced around $278 million of forced selling. Those are big single-stock flows, but here is the thing: eight stocks changing hands does not, by itself, drag the whole Nifty down 359 points.

Here’s the full list:

Why does the WHOLE index react, not just those eight names?

Two words: passive money.

A huge pool of global capital is “passive.” These are ETFs and index funds whose only job is to mirror the index exactly. They are not trying to beat the market, they are trying to be the market. So the moment MSCI changes the recipe, these funds have no discretion. They buy and sell to match, regardless of price, regardless of whether they like the stock.

Now look past the inclusions and exclusions at the long “weight down” column in those tables. This is the quiet engine of today’s fall. MSCI trimmed the index weight of a stack of heavyweights through float adjustments: TCS, Infosys, HUL, Bajaj Finance, ONGC, Ultratech, HAL, Coal India, Nestle, Power Grid and many more. When the weight of the biggest members gets cut, passive funds have to sell hundreds of millions of dollars of exactly those large, index-heavy stocks. That is mechanical selling concentrated in the names that move the index the most.

And there is a timing quirk that turns it into a candle. To keep their tracking error as small as possible, these funds want to execute as close as possible to the official closing price on rebalance day. So instead of spreading trades through the session, all of it stampedes into the last half hour at once. That wall of forced flow is the cliff on your chart. Massive volume, sharp move, then it is over.

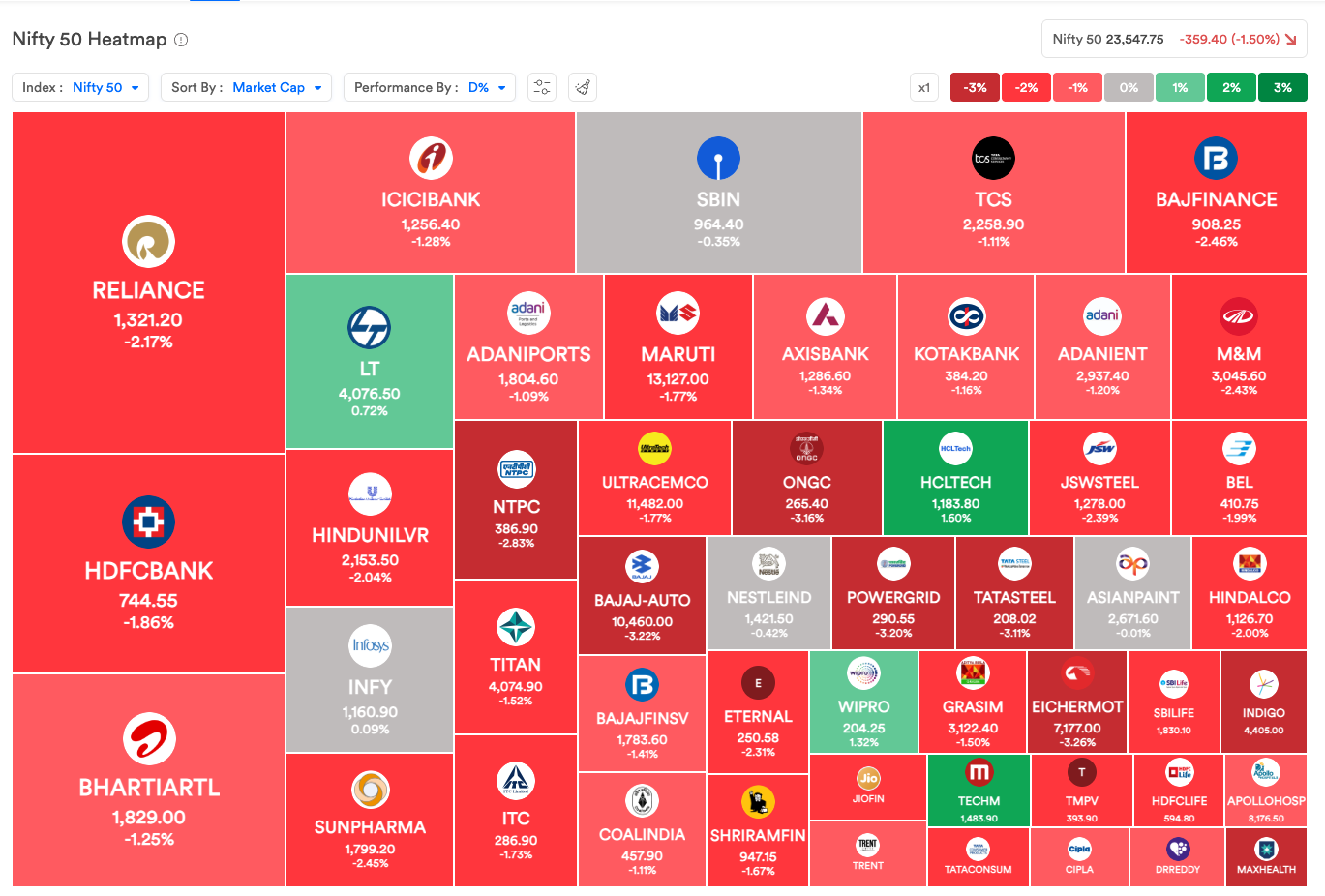

The heatmap tells the same story

Look at where the red is deepest today: ONGC down 3.16%, Power Grid down 3.20%, Tata Steel down 3.11%, Eicher down 3.26%, Bajaj Auto down 3.22%, NTPC down 2.83%, Bajaj Finance down 2.46%. Energy, metals, autos and PSUs took the brunt, and many of these are the very names sitting in the weight-down list. The only real green pocket was IT, with HCL Tech up 1.60%, Wipro up 1.32% and Infosys roughly flat.

One honest nuance worth flagging, because the tables show it: some giants like Reliance, HDFC Bank, Bharti and ICICI were actually on the receiving end of weight increases today, yet they still closed red. That tells you rebalancing flow is not a magic up or down switch for any single stock. It is one force landing on top of whatever mood the market is already in, and today the mood was sour enough to swamp even the buying.

Because today wasn’t only MSCI

Notice on the intraday chart that Nifty was already sloping down well before the close. Two things had left it jumpy through the day:

- The IMD trimmed its monsoon forecast for June to September, from 92% to 90% of the long period average. A softer monsoon revives worries about rural demand and food inflation, so sentiment turns cautious.

- FIIs have been leaning on the sell side, and rebalancing flows tend to amplify whatever direction the day is already drifting.

So you had an index already grinding lower, and then the mechanical MSCI selling dropped right on top of it in the closing window. That stacking is how a slow bleed turned into a near 300-point air pocket in minutes. Worth noting the rest of Asia did not share the gloom today, Korea’s Kospi was up over 3% and Japan’s Nikkei rose around 2.5%. This was a very domestic-flavoured fall, not a global risk-off.

What does this mean for us as traders?

A few honest takeaways, not hot takes:

- These candles look dramatic but are often the least informative moves of the month. The “why” is a calendar event, not a market view. Treating a rebalancing candle like fresh bearish news is exactly how people get shaken out at the worst possible price.

- If you trade intraday or options, rebalancing days have a known signature, and today is a textbook example: choppy, directionless drift for most of the session, then a liquidity flood near the close. The date is announced weeks in advance, so half the edge is just marking your calendar.

- For longer-term investors, forced selling occasionally drags good names down with the flow, which historically is where the calmer money tends to wait and step in.

One for the community: when a rebalancing candle hits like today, are you the type who steps aside and just watches it play out, or do you actively trade the closing volatility?