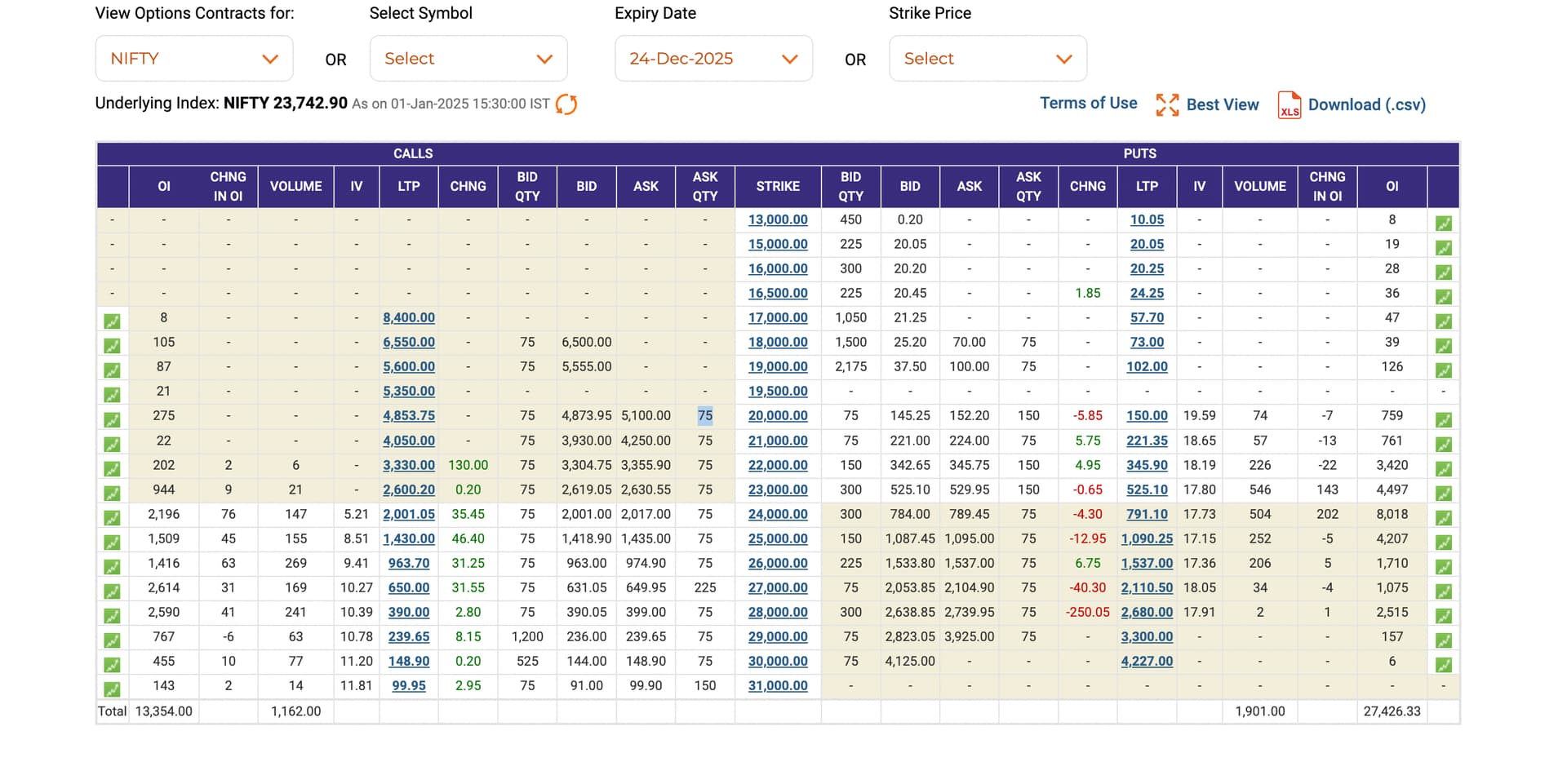

Why are the PUT options way cheaper than the call options for the long term expiry?

For Eg: 24000CE is trading at 2000 whereas 24000PE is trading at 791 at the moment. why is this disparity?

Why are the PUT options way cheaper than the call options for the long term expiry?

For Eg: 24000CE is trading at 2000 whereas 24000PE is trading at 791 at the moment. why is this disparity?

No, they are equal-ish, but you need to check the row corresponding to the Future price of expiry date, not the current spot price.

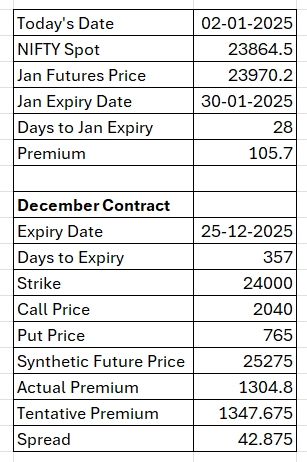

@srinivasr You are checking for December 2025 options which have almost 360 days for expiry. The correct matric to check would be Put Call Parity. PFA the tentative calculations

PS: This is one of the method to estimate the spread in NIFTY Contracts and establish an arbitrage between Actual Futures and Synthetic Futures.