First of all, decent comparison. Thanks for thinking this way.

But I feel sorry that you considered 6.55% ROI in bank FD, whereas you can easily earn 7.99% in regular banks like Indusind, etc . (I am not even bringing SF banks which give 9% ROI)

the 7.99 vs 6.55 automatically clears the gap of stcg 20% and 30% tax slab

fd will turn out to be better.

additionally, when you cancel FD, you still get some interest guaranteed but in Tbills, it may happen sometimes that even though 50% duration has crossed, I havent got any return due to market pricing. (it has happened with me so I know)

TRUST ME - FDs are better.

Tbill is a scam nothing else. only buy it if you’re able to get it at 9 to 10% IRR due to market pricing disparity. (only if you’re lucky)

The key point missed in this analysis is that all FDs aren’t equal.

There is an additional risk associated with the banks that are unable to raise sufficient funds at a lower rate of interest that they would have to pay out, hence their willingness to pay a few additional percentage points of interest more to raise sufficient funds.

Adjust for the principal at risk

and a sovereign guarantee far outweighs a guarantee on an FD that any individual bank within the same country can offer. RBI can literally “print money”# to fulfill a sovereign guarantee. Of course that leads to inflation and a weaker-rupee, But, in such a scenario, that’s a problem for the rest of the folks who do not hold a bond with sovereign guarantee.

# Note: IIUC, in this digital age, there is no printing involved, simply adjusting the balance amount owed by the govt. is incremented, and the necessary interest payments are made to fulfill the payments on the bonds with sovereign guarantee. eg. T-Bills, GSECs, SDLs.

Maximum conservative? definitely not.

What is “conservative” here?

Did you perhaps mean traditional without exposure to modern markets?

For example. there isn’t sufficient diversification to protect against any factors that affect all banks.

For example, and even more “conservative” approach would be -

to invest a part in other countries (to protect against inflation)

to hold cash or SB (to the extent one needs instant liquidity)

to invest in FDs of non-banks (to limit one’s exposure to banks).

to invest in a “T-Bill ladder” (to ensure regular predictable income)

to invest in overnight funds or even hybrid mutual-funds (to limit exposure to debt. with limited exposure to equity)

…

Also, what specific risks does this approach protect against?

When comparing investment opportunities, my favorite goto these days is -

Here’s an elevator pitch of T-Bills for one’s grandma

i.e. in terms that someone from a previous generation,

who is aware of banking products like FDs,

would understand -

" An Indian T-Bill is like an FD issued by THE BANK that controls the rupee (RBI), that pays its “interest” upon maturity. "

T-Bill is a bond :

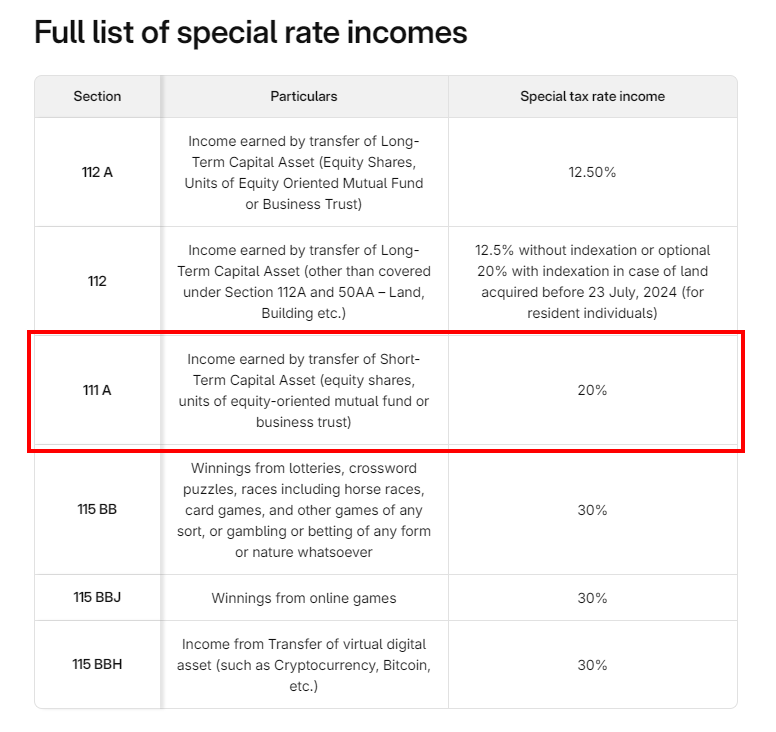

with zero coupon rate. (no interest, all income paid out as capital gains, STCG.).

and the income taxed at slab-rate (all types of STCG is not taxed identically).

that matures in 91/182/364 days when purchased by primary (RBI auction).

can mature sooner if purchased on NSE/BSE

someone else purchased it initially from primary and is selling it before maturity.

Compared to a traditional bank FD, the largest risk is liquidity before maturity.

While one can always sell a T-BIll before maturity on BSE/NSE,

one often ends-up losing a lot more than what typical banks charge on premature withdrawal of FDs held at the bank.

For more details,

checkout Government Securities – Varsity by Zerodha Varsity by Zerodha

and use the Markets > Bonds >T-Bills section in Dhan

to find out T-Bills trading at a discount,

and scalp them to get anywhere between 7% - 20% annualized returns on most days,

on T-bills maturing anywhere between 3 - 300 days.

PS: How do i know these numbers?

Over the last 5 years, if you have sold any T-Bill / SDL / GSEC at a deep discount on either BSE/NSE, chances are that i was the counter-party who purchased it.

Thank you for taking the time to help us understand this topic. With your many years of experience working with this instrument, it’s clear you have gained a lot of knowledge about it.

After new finance bill 2025, stcg is not included for rebate so it became far less attractive than FDs for people earning upto 12L. bcz selling tbills and earning interest would attract 20% stcg which otherwise would have been fully exempt