Fixed Deposits (FDs) have long been the go-to choice for risk-averse investors. But have you considered Treasury Bills (T-Bills)? These government-backed instruments combine safety, liquidity, and competitive returns, making them a strong alternative to FDs.

What Are T-Bills?

T-Bills are short-term debt instruments issued by the government to raise funds. They are considered one of the safest investments as they are backed by the government. T-Bills are issued for tenures of 91 days, 182 days, and 364 days, making them an excellent choice for investors seeking short-term options.

T-Bills are sovereign-backed instruments, making them virtually risk-free. FDs, while considered safe, are only insured up to ₹5 lakhs under the Deposit Insurance and Credit Guarantee Corporation (DICGC). For investments exceeding this limit, T-Bills are a safer alternative.

How are T-Bills Priced?

They are issued at a discount and redeemed at face value, meaning your returns depend on the difference between the purchase price and the redemption value.

How to Buy T-Bills?

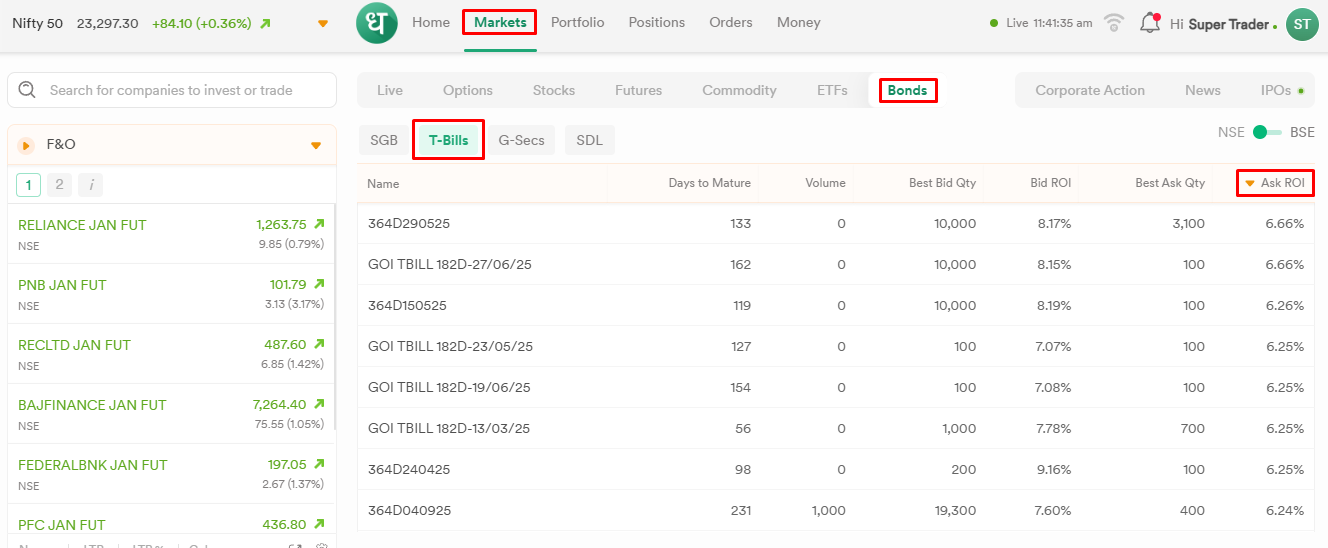

Primary Market: Bid directly via the RBI’s NCB marketplace (soon available on Dhan). Secondary Market: Explore better ROI opportunities on Dhan under Markets > Bonds > T-Bills.

Would also like to know similar comparison for swp mutual funds.

Say one time initial investment amount is 1 Cr, so a roi of 12% annually assumed and if I take payout of 0.5% every month, still I can grow with 6%?

This is just in my layman term calculation.

A detailed nuisance comparison with FD on this would be great, benchmark with FD is a great idea as most of us are well aware with FDs, hence understanding of comparison gives a better grasp of performance.

@thisisbanerjee I understand your concern that with fixed deposits (FDs), you can easily reach out to the local bank branch or relationship manager, whereas with T-Bills, the point of contact is the RBI, which may feel less accessible due to the lack of a peer connection. However, rest assured that T-Bills come with sovereign settlement, meaning they are automatically redeemed into the investor’s bank account—provided you don’t frequently change your bank details with the DP. For your information, proprietary books and FPIs also allocate substantial funds to T-Bills, as they carry an NCL haircut of just 2%, offering better collateral value for margin trading.

@RajeshK SWP works the same way as you said. The difference between yield and withdrawal becomes your net return. Generally SWP withdrawals are based on amount terms and not % as % would be huge (As AUM grows the % also grows). Also comparing FD with MF would not be a viable comparision as they are both ment for surving different purpose.

Can we buy and sell this easily using a trading app, similar to how we purchase stocks? Or do we need to reach out to a stock broker to find a buyer or seller?

Also, is the liquidity and spread of T-Bills reasonable for retail clients?

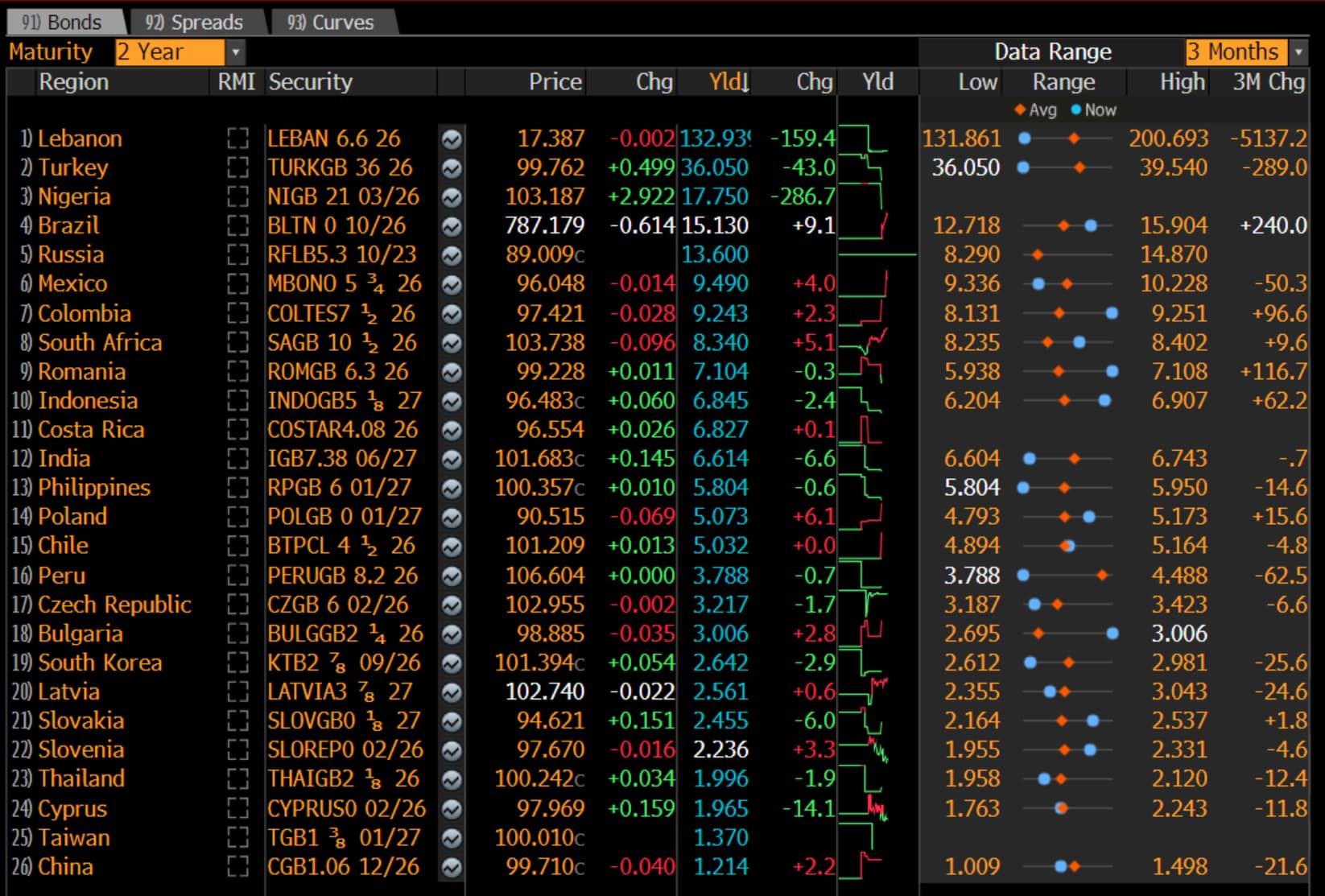

@thisisbanerjee Government mishaps are serious for sure. Infact that is the main reason why different governments have different rate of Interests. Just sharing an extract on interest rates of different countries.

Regarding SGBs, I wouldn’t place the blame on the government; it was indeed a good initiative. However, as mentioned, it was not suited to the Indian mindset. Since India is not a gold-producing country, the main objective was to reduce gold imports and boost foreign exchange reserves. Unfortunately, recent data shows that gold imports have been rising, leaving the government facing pressure on two fronts: the balance of payments and the tax revenue loss from SGBs.

@Brishide Yes you can buy and sell T-Bills using the App as well. However, more important in these securities is exploring them which is easily possible over the Web. You can explore based on the Ask ROI and Maturity and easily buy from the same screen.

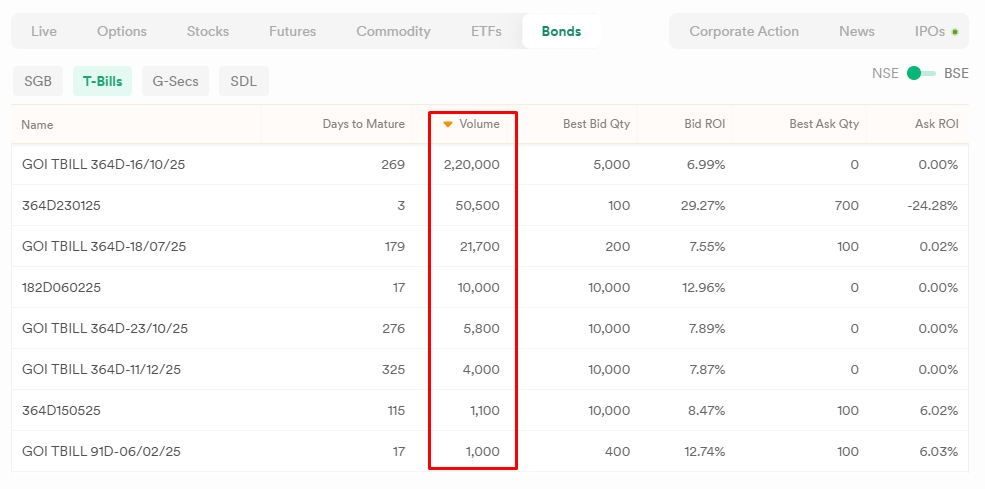

In terms of liquidity, T-Bills are not that liquid (incase you planning to sell in the secondary market). Better is to buy and get it redeemed from the RBI.

Bharat par hey viswas, Poora hey Viswas…It is not a 1 person country. It is a land of over 140 Cr people with a rich and diverse history. In this century we will reclaim our lost glory.

I am not a fan of leftist historians who painted a distorted picture of India Anyway it seems we are on different alleys of reality. So I don’t want to take this further on this thread of T-Bills

Luxembourg’s Per Capita GDP ( 1st on the list ): Approximately $132,370.

India’s Required GDP to match Luxembourg’s Per Capita GDP: Approximately $185.32 trillion to reach this per capita GDP with its population of about 1.4 billion.

World’s Total GDP: Estimated at approximately $100 trillion to $105 trillion.

For India’s GDP to reach the same level as Luxembourg’s income per capita, it would have to be greater than the total GDP of the entire planet.

For India to achieve the per capita GDP of the United States ( Positioned 3rd on the List ), India would need a total GDP of approximately $112.04 trillion, which is still greater than the total GDP of the entire planet.

This really shows how these calculations can hold us back and are not very useful. The statistics derived from them are often used in ways that can hurt the hopes and self-worth of our people.

@amish To engage larger audience into the debt market, RBI has launched eKuber, direct platform for buying government debt securities but that did not gauge much traction. So RBI decided to aggregate bids for these securities from the exchange(s) which has a larger connect with the retail audience. Here the bidding will be of NCB nature meaning that retail investors will be price acceptors (from NDS-OM).

Though I am not a Tax Expert, but T-Bills are to be treated as securities which mature in less than a year so they are to be taxable under STGC. @quicko and @cleartax Is this assertion correct?