- This error is related to dhanhq version

- This can be covered in commodity market

solution to both of the issues, will be covered in upcoming video release for Dhan_Tradehull_V2.py

solution to both of the issues, will be covered in upcoming video release for Dhan_Tradehull_V2.py

@Tradehull_Imran

Thanks for quick response ![]() when we will get next video?

when we will get next video?

Hi @Vijen_Singh

see session3 codebase

exit_all = tsl.cancel_all_orders()

tsl.get_option_chain(symbol, exchange)

do raise this feature request for this function on below link,

for all options chain related features I am tracking on this link :

https://private-poc.madefortrade.in/t/tick-by-tick-algo-for-option-chain-with-oi-buildup-and-covering/34867?u=tradehull_imran

use ce_name, pe_name, strike = tsl.ATM_Strike_Selection('NIFTY','expiry_date')

live_pnl = tsl.get_live_pnl()

exit_all = tsl.cancel_all_orders()

isse to jo order hai wo cancel honge na position bhi exit ho jayegi kya?

ce_name, pe_name, strike = tsl.ATM_Strike_Selection('NIFTY','expiry_date')mujhe ATM, OTM ya ITM ki strick price nhi chahiye mujhe premium based strick price chahiye qki mujhe pta hi nhi hai 95 greater than premium kisme aayega OTM me aayega ya ITM me ya ATM me

to me 1. use ce_name, pe_name, strike = tsl.ATM_Strike_Selection('NIFTY','expiry_date')

is function ka use kese kru?

Thanks for the response but message is not going to telegram… may be i am not doing the right thing…

Also i am not able to place target order as we well. please help

target_order = tsl.order_placement(stock_name,‘NSE’, qty, 0, target_price,‘LIMIT’, ‘BUY’, ‘MIS’)

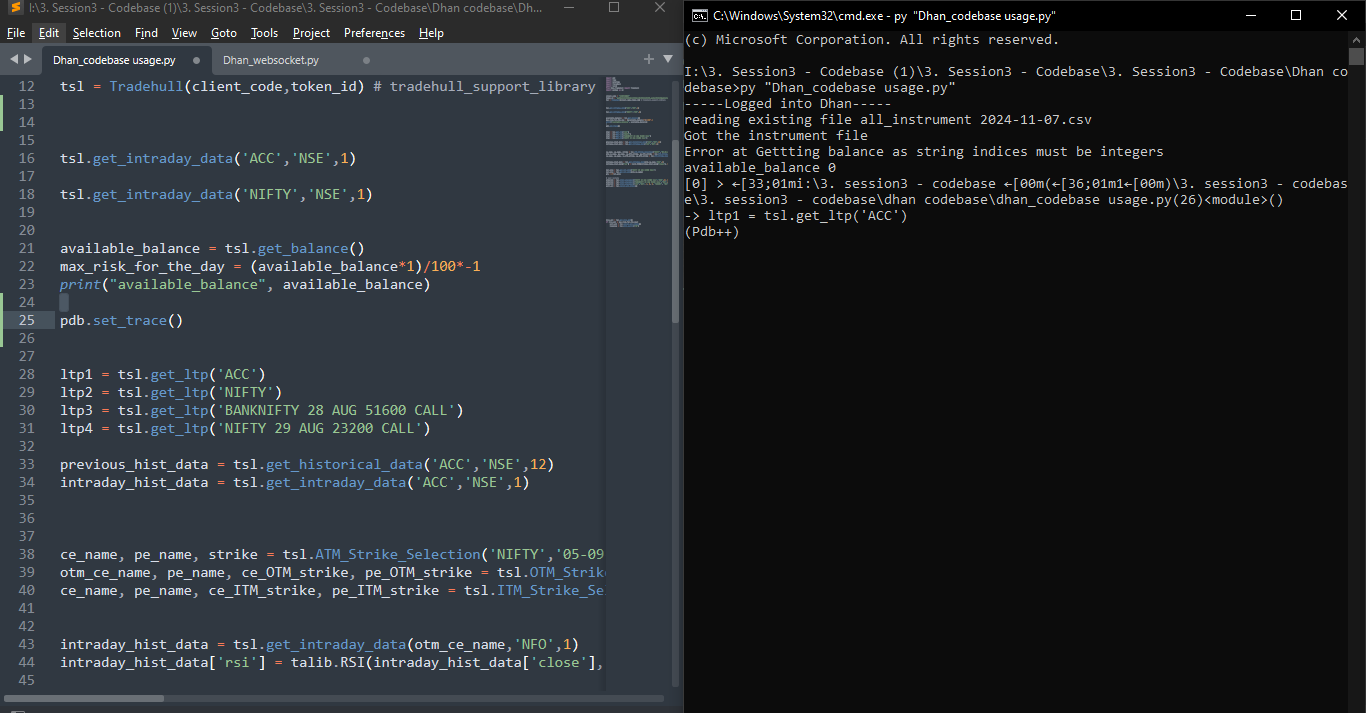

Hi Sir @Tradehull_Imran ! Thank you so much for the prompt response . Power shell method worked . I’m getting the LTPs now. No more SSL erros

However, on running the codebase file, I’m unable to fetch balance. I haven’t changed the code . I’ve just used pdb.set_trace (). I’m getting the error that : “Error at Gettting balance as string indices must be integers

available_balance 0”. Please help.

@Tradehull_Imran Sir, Thanks for the resolution of websocket errors. I’m able to fetch the LTPs now.

Hi everyone,

Below is the explanation video for Dhan_Tradehull_V2

This will solve majority of the issues you were facing in LTP and Historical data as well.

Codefiles : https://drive.google.com/file/d/1wCN8zpwHNKyW0xws9jhUMrkQVj5ehBRU

import pdb

from Dhan_Tradehull import Tradehull

import pandas as pd

import talib

import time

# Trading API client setup

client_code = ""

token_id = ""

tsl = Tradehull(client_code, token_id)

# Intraday strategy parameters

available_balance = tsl.get_balance()

leveraged_margin = available_balance * 5 # 5x leverage

max_trades = 1

per_trade_margin = leveraged_margin / max_trades # Amount for each trade

# Watchlist

watchlist = ['NBCC', 'RVNL', 'IFCI', 'HUDCO', 'MAZDOCK', 'INOXWIND', 'ZEEL', 'BSE', 'MMTC', 'ITI', 'BEML', 'SUZLON', 'HINDCOPPER', 'RELIANCE']

traded_watchlist = []

# Function to calculate 69 EMA and check for trend (uptrend/downtrend)

def check_trend_and_touch_ema(chart):

# Calculate 69 EMA for the chart

chart['69ema'] = talib.EMA(chart['close'], timeperiod=69)

# Get the last 4 EMA values for slope detection

ema_values = chart['69ema'].iloc[-4:].values # Last 4 EMA values

ema_slope_uptrend = all(ema_values[i] < ema_values[i+1] for i in range(3)) # Uptrend condition

ema_slope_downtrend = all(ema_values[i] > ema_values[i+1] for i in range(3)) # Downtrend condition

# Get the most recent candle (breakout candle)

bc = chart.iloc[-2] # Breakout candle

# Check if any part of the candle touches the 69 EMA (either body or wick)

touch_ema_uptrend = (bc['high'] >= bc['69ema'] >= bc['low']) or (bc['close'] >= bc['69ema'] >= bc['open'])

touch_ema_downtrend = (bc['high'] >= bc['69ema'] >= bc['low']) or (bc['close'] <= bc['69ema'] <= bc['open'])

return ema_slope_uptrend, ema_slope_downtrend, touch_ema_uptrend, touch_ema_downtrend, bc

# Main loop for the strategy

while True:

for stock_name in watchlist:

print(f"Processing {stock_name}…")

# Fetch intraday data for the stock (1-minute candles)

chart = tsl.get_intraday_data(stock_name, 'NSE', 15) # Fetch 1-minute candles

if chart is None or chart.empty:

print(f"No data retrieved for {stock_name}. Skipping...")

continue

# Check trend and EMA touch conditions

try:

ema_slope_uptrend, ema_slope_downtrend, touch_ema_uptrend, touch_ema_downtrend, bc = check_trend_and_touch_ema(chart)

print(f"{stock_name} - 69 EMA values: {chart['69ema'].iloc[-4:]}")

print(f"Uptrend: {ema_slope_uptrend}, Downtrend: {ema_slope_downtrend}")

print(f"Touch EMA Uptrend: {touch_ema_uptrend}, Touch EMA Downtrend: {touch_ema_downtrend}")

except Exception as e:

print(f"Error processing {stock_name}: {e}")

continue

# Ensure there is enough data for trend analysis

if len(chart) < 4:

print(f"Not enough data for {stock_name}. Skipping...")

continue

# Check for trade conditions

no_repeat_order = stock_name not in traded_watchlist

max_order_limit = len(traded_watchlist) < max_trades # Ensure we don't exceed max trades

# Calculate quantity to trade based on the available margin

qty = int(per_trade_margin / bc['close']) # Quantity based on the price of the stock

# Assuming you already have the correct logic in place for determining uptrend/downtrend

# and the other conditions for placing orders.

# Example when placing a sell order (if conditions for downtrend and touch EMA are met)

if ema_slope_downtrend and touch_ema_downtrend and no_repeat_order and max_order_limit:

print(f"Placing sell order for {stock_name} - Quantity: {qty}")

trigger_price = 0 # For a market order, trigger price might not be needed

tsl.order_placement(stock_name, 'NSE', qty, 1, 0, 'MARKET', 'BUY', 'MIS')

traded_watchlist.append(stock_name)

time.sleep(10) # Sleep to prevent hitting API rate limits

# Example when placing a buy order (if conditions for uptrend and touch EMA are met)

if ema_slope_uptrend and touch_ema_uptrend and no_repeat_order and max_order_limit:

print(f"Placing buy order for {stock_name} - Quantity: {qty}")

trigger_price = 0 # For a market order, trigger price might not be needed

tsl.order_placement(stock_name, 'NSE', qty, 1, 0, 'MARKET', 'SELL', 'MIS')

traded_watchlist.append(stock_name)

time.sleep(10) # Sleep to prevent hitting API rate limits

time.sleep(10) # Sleep between each watchlist check

When keep the tsl.get_intraday_data(stock_name, ‘NSE’, 1) to 1 minute the order gets place instantly but if I make it to 15 min then the order is not getting placed at all. Not sure what the issue is here.

This is a different strategy I was trying by seeing the upward/downward trend candle of 15 min timeframe touching the 69 EMA line to place orders.

Also I haven’t been able to figure out how to place stop loss and targets to my orders. I am doing it manually now. I would want it to be automated through the code. Could you please help with this.

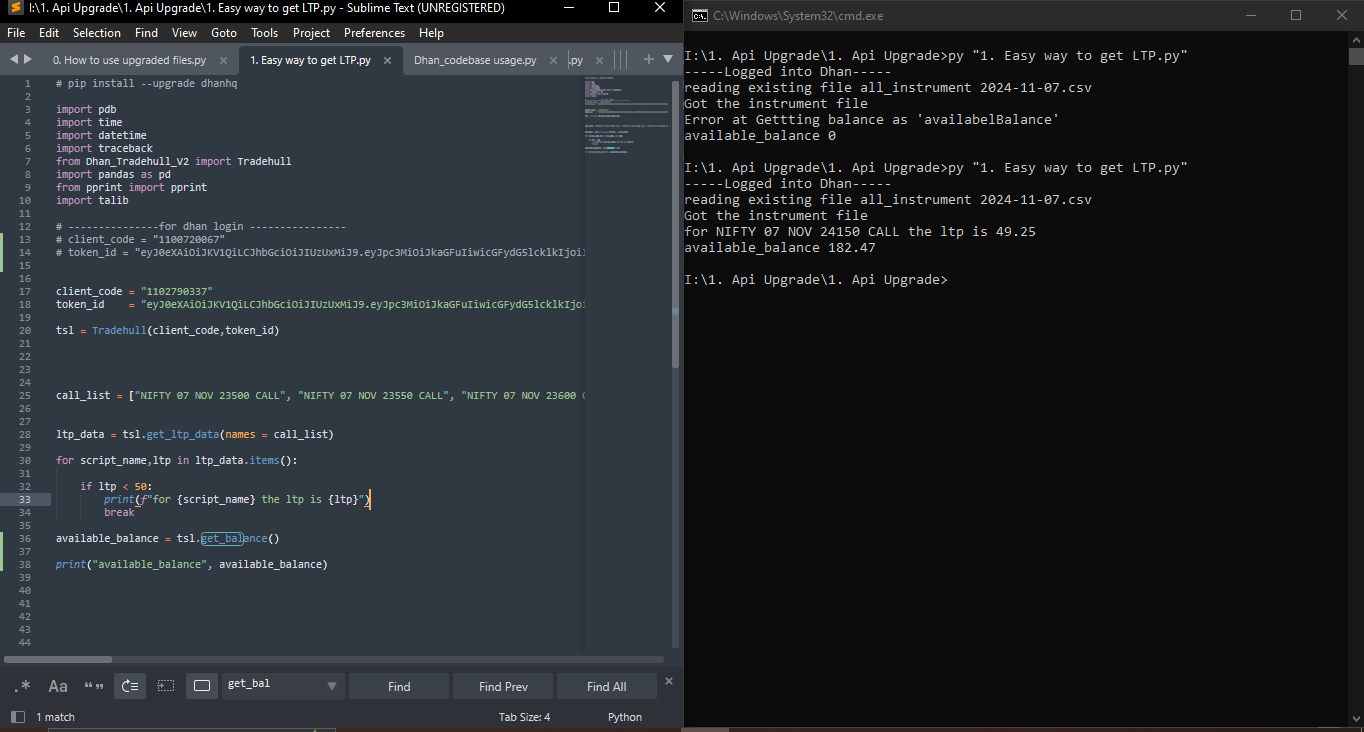

Hi Sir!

In the file " " , when I enter my dhan credentials , I get the attached error. However , if I’m running the file with already entered credentials, code is running fine. Please help resolve the issue.

File name “1. Easy way to get LTP.py”

Finally

Waow

Hye @Tradehull_Imran

Big Thankyou for such an informative video, now please guide us how to deploy it in server, because keeping laptop on all the time is not possible for strategy execution.

Very informative

Totally agree @Zee2Zahid ![]()

Already requested to @Tradehull_Imran sir from my side also

how to write supertrend indicator in talib format?

@Tradehull_Imran hi sir mene youtube pr session 8 dekha usse mene code copy

wait for market to start 09:29:58.468498

wait for market to start 09:29:59.547835

MOTHERSON

dhanhq.intraday_minute_data() takes 4 positional arguments but 7 were given

Traceback (most recent call last):

File “/Users/vijju/Desktop/Stock Algo/Dhan Algo/8. Session8- 2nd Live Algo/2nd live Algo/Dhan_Tradehull_V2.py”, line 257, in get_historical_data

ohlc = self.Dhan.intraday_minute_data(str(security_id),exchange_segment,instrument_type,self.start_date,self.end_date,int(interval))

TypeError: dhanhq.intraday_minute_data() takes 4 positional arguments but 7 were given

Traceback (most recent call last):

File “/Users/vijju/Desktop/Stock Algo/Dhan Algo/8. Session8- 2nd Live Algo/2nd live Algo/Multi timeframe Algo.py”, line 58, in

chart_1[‘rsi’] = talib.RSI(chart_1[‘close’], timeperiod=14) #pandas

TypeError: ‘NoneType’ object is not subscriptable

vijjus-MacBook-Air:8. Session8- 2nd Live Algo vijju$

ye error aa rhi hai

import pdb

from Dhan_Tradehull_V2 import Tradehull

import pandas as pd

import talib

import time

import datetime

client_code = “1101529493”

token_id = “eyJ0eXAiOiJKV1QiLCJhbGciOiJIUzUxMiJ9.eyJpc3MiOiJkaGFuIiwicGFydG5lcklkIjoiIiwiZXhwIjoxNzMxNzcxMDU4LCJ0b2tlbkNvbnN1bWVyVHlwZSI6IlNFTEYiLCJ3ZWJob29rVXJsIjoiIiwiZGhhbkNsaWVudElkIjoiMTEwMTUyOTQ5MyJ9.Oo3_dwF1lGkiSenKu-XdpsMZIav5og-BK2CxzuTPyaAZGyUMDJEb_lCaTOLXwydfeeXbwzeKRs3pHXhlosKGGQ”

tsl = Tradehull(client_code,token_id) # tradehull_support_library

available_balance = tsl.get_balance()

leveraged_margin = available_balance5

max_trades = 3

per_trade_margin = (leveraged_margin/max_trades)

max_loss = (available_balance1)/100*-1

watchlist = [‘MOTHERSON’, ‘OFSS’, ‘MANAPPURAM’, ‘BSOFT’, ‘CHAMBLFERT’, ‘DIXON’, ‘NATIONALUM’, ‘DLF’, ‘IDEA’, ‘ADANIPORTS’, ‘SAIL’, ‘HINDCOPPER’, ‘INDIGO’, ‘RECLTD’, ‘PNB’, ‘HINDALCO’, ‘RBLBANK’, ‘GNFC’, ‘ALKEM’, ‘CONCOR’, ‘PFC’, ‘GODREJPROP’, ‘MARUTI’, ‘ADANIENT’, ‘ONGC’, ‘CANBK’, ‘OBEROIRLTY’, ‘BANDHANBNK’, ‘SBIN’, ‘HINDPETRO’, ‘CANFINHOME’, ‘TATAMOTORS’, ‘LALPATHLAB’, ‘MCX’, ‘TATACHEM’, ‘BHARTIARTL’, ‘INDIAMART’, ‘LUPIN’, ‘INDUSTOWER’, ‘VEDL’, ‘SHRIRAMFIN’, ‘POLYCAB’, ‘WIPRO’, ‘UBL’, ‘SRF’, ‘BHARATFORG’, ‘GRASIM’, ‘IEX’, ‘BATAINDIA’, ‘AARTIIND’, ‘TATASTEEL’, ‘UPL’, ‘HDFCBANK’, ‘LTF’, ‘TVSMOTOR’, ‘GMRINFRA’, ‘IOC’, ‘ABCAPITAL’, ‘ACC’, ‘IDFCFIRSTB’, ‘ABFRL’, ‘ZYDUSLIFE’, ‘GLENMARK’, ‘TATAPOWER’, ‘PEL’, ‘IDFC’, ‘LAURUSLABS’, ‘BANKBARODA’, ‘KOTAKBANK’, ‘CUB’, ‘GAIL’, ‘DABUR’, ‘TECHM’, ‘CHOLAFIN’, ‘BEL’, ‘SYNGENE’, ‘FEDERALBNK’, ‘NAVINFLUOR’, ‘AXISBANK’, ‘LT’, ‘ICICIGI’, ‘EXIDEIND’, ‘TATACOMM’, ‘RELIANCE’, ‘ICICIPRULI’, ‘IPCALAB’, ‘AUBANK’, ‘INDIACEM’, ‘GRANULES’, ‘HDFCAMC’, ‘COFORGE’, ‘LICHSGFIN’, ‘BAJAJFINSV’, ‘INFY’, ‘BRITANNIA’, ‘M&MFIN’, ‘BAJFINANCE’, ‘PIIND’, ‘DEEPAKNTR’, ‘SHREECEM’, ‘INDUSINDBK’, ‘DRREDDY’, ‘TCS’, ‘BPCL’, ‘PETRONET’, ‘NAUKRI’, ‘JSWSTEEL’, ‘MUTHOOTFIN’, ‘CUMMINSIND’, ‘CROMPTON’, ‘M&M’, ‘GODREJCP’, ‘IGL’, ‘BAJAJ-AUTO’, ‘HEROMOTOCO’, ‘AMBUJACEM’, ‘BIOCON’, ‘ULTRACEMCO’, ‘VOLTAS’, ‘BALRAMCHIN’, ‘SUNPHARMA’, ‘ASIANPAINT’, ‘COALINDIA’, ‘SUNTV’, ‘EICHERMOT’, ‘ESCORTS’, ‘HAL’, ‘ASTRAL’, ‘NMDC’, ‘ICICIBANK’, ‘TORNTPHARM’, ‘JUBLFOOD’, ‘METROPOLIS’, ‘RAMCOCEM’, ‘INDHOTEL’, ‘HINDUNILVR’, ‘TRENT’, ‘TITAN’, ‘JKCEMENT’, ‘ASHOKLEY’, ‘SBICARD’, ‘BERGEPAINT’, ‘JINDALSTEL’, ‘MFSL’, ‘BHEL’, ‘NESTLEIND’, ‘HDFCLIFE’, ‘COROMANDEL’, ‘DIVISLAB’, ‘ITC’, ‘TATACONSUM’, ‘APOLLOTYRE’, ‘AUROPHARMA’, ‘HCLTECH’, ‘LTTS’, ‘BALKRISIND’, ‘DALBHARAT’, ‘APOLLOHOSP’, ‘ABBOTINDIA’, ‘ATUL’, ‘UNITDSPR’, ‘PVRINOX’, ‘SIEMENS’, ‘SBILIFE’, ‘IRCTC’, ‘GUJGASLTD’, ‘BOSCHLTD’, ‘NTPC’, ‘POWERGRID’, ‘MARICO’, ‘HAVELLS’, ‘MPHASIS’, ‘COLPAL’, ‘CIPLA’, ‘MGL’, ‘ABB’, ‘PIDILITIND’, ‘MRF’, ‘LTIM’, ‘PAGEIND’, ‘PERSISTENT’]

traded_wathclist =

while True:

live_pnl = tsl.get_live_pnl()

current_time = datetime.datetime.now().time()

if current_time < datetime.time(9, 30):

print("wait for market to start", current_time)

continue

if (current_time > datetime.time(15, 15)) or (live_pnl < max_loss):

I_want_to_trade_no_more = tsl.kill_switch('ON')

order_details = tsl.cancel_all_orders()

print("Market is over, Bye Bye see you tomorrow", current_time)

break

for stock_name in watchlist:

time.sleep(0.2)

print(stock_name)

# Conditions that are on 1 minute timeframe

# chart_1 = tsl.get_intraday_data(stock_name, 'NSE', 1) # 1 minute chart # this call has been updated to get_historical_data call,

chart_1 = tsl.get_historical_data(tradingsymbol = stock_name,exchange = 'NSE',timeframe="1")

chart_1['rsi'] = talib.RSI(chart_1['close'], timeperiod=14) #pandas

cc_1 = chart_1.iloc[-2] #pandas completed candle of 1 min timeframe

uptrend = cc_1['rsi'] > 50

# downtrend = cc_1['rsi'] < 49

# Conditions that are on 5 minute timeframe

# chart_5 = tsl.get_intraday_data(stock_name, 'NSE', 5) # 5 minute chart

chart_5 = tsl.get_historical_data(tradingsymbol = stock_name,exchange = 'NSE',timeframe="5") # this call has been updated to get_historical_data call,

chart_5['upperband'], chart_5['middleband'], chart_5['lowerband'] = talib.BBANDS(chart_5['close'], timeperiod=5, nbdevup=2, nbdevdn=2, matype=0)

cc_5 = chart_5.iloc[-1] # pandas

ub_breakout = cc_5['high'] > cc_5['upperband']

# lb_breakout = cc_5['low'] < cc_5['lowerband']

no_repeat_order = stock_name not in traded_wathclist

max_order_limit = len(traded_wathclist) <= max_trades

if uptrend and ub_breakout and no_repeat_order and max_order_limit:

print(stock_name, "is in uptrend, Buy this script")

sl_price = round((cc_1['close']*0.98),1)

qty = int(per_trade_margin/cc_1['close'])

buy_entry_orderid = tsl.order_placement(stock_name,'NSE', 1, 0, 0, 'MARKET', 'BUY', 'MIS')

sl_orderid = tsl.order_placement(stock_name,'NSE', 1, 0, sl_price, 'STOPMARKET', 'SELL', 'MIS')

traded_wathclist.append(stock_name)

# if downtrend and lb_breakout and no_repeat_order and max_order_limit:

# print(stock_name, "is in downtrend, Sell this script")

# sl_price = round((cc_1['close']*1.02),1)

# qty = int(per_trade_margin/cc_1['close'])

# buy_entry_orderid = tsl.order_placement(stock_name,'NSE', 1, 0, 0, 'MARKET', 'SELL', 'MIS')

# sl_orderid = tsl.order_placement(stock_name,'NSE', 1, 0, sl_price, 'STOPMARKET', 'BUY', 'MIS')

# traded_wathclist.append(stock_name)

ye code hai please help me

Hi @Tradehull_Imran,

Thanks for the updated API… I am able to extract historical data in 1 min and 5 min interval… can i get intraday historical data in 2 min tf ?

trying to get 2 min interval historical data and got the below error

data_day = tsl.get_historical_data(tradingsymbol = ‘ACC’,exchange = ‘NSE’,timeframe=“2”)

ValueError: DataFrame constructor not properly called!

Thanks in advance